South Australia Housing Statistics: supply, approvals and rental vacancy rates

Greater Adelaide added 18,647 residents in 2024–25, while South Australia approved 14,516 dwellings over the same period. Building approvals remained elevated through to March 2026, but completions were more uneven, falling in the September quarter before rebounding to 3,726 in the December quarter of 2025. Adelaide's rental vacancy rate held at 0.7% in May 2026, placing it among the tightest capital city rental markets. Annual advertised rent growth eased to 4.9%, below the national average and behind Darwin, Hobart and Brisbane. Playford accounted for almost one in six dwelling approvals across South Australia, while water and sewerage capacity constraints affecting major northern release areas are now being addressed.

Dwellings approved, 2024–25

14,516

10,394 new houses · 4,017 other residential · 105 conversions

Completions, Dec Q 2025

3,726

Up from 3,111 in Sep Q 2025

Rental vacancy, May 2026

0.7%

1,081 properties available; among the tightest capital city markets

SA Housing Accord shortfall

18,000

66,000 of 84,000 target projected 2024–29; full delivery not expected until March 2031

Section 01 · Where Adelaide is growing

Where are new homes being approved in Adelaide?

Playford approved 2,302 dwellings in 2024–25, the highest total of any local government area in South Australia and equivalent to 15.9% of all dwelling approvals in the state. The LGA also added 4,357 residents over the same period, growing by 3.9%, the fastest rate of any South Australian council area. New approvals across Greater Adelaide remain concentrated in a small number of outer-fringe and middle-ring locations.

Salisbury, one of the state's larger established council areas with about 151,000 residents, approved 712 dwellings while adding 382 residents. Charles Sturt recorded a different approval mix, with 919 apartments and townhouses compared with 538 houses, making it the strongest inner-ring example of medium-density approval activity in this dataset.

Where are the most new homes being approved?

Playford approved 2,302 dwellings in 2024–25, the highest total of any LGA in South Australia. It was followed by Charles Sturt with 1,463 approvals, Port Adelaide Enfield with 1,027 and Onkaparinga with 890.

15.9%

of all SA approvals

Playford's share of state-wide dwelling approvals, 2024–25

Playford accounted for roughly one in every six dwellings approved across South Australia in 2024–25. Together, the Playford–Salisbury–Gawler corridor accounted for 3,202 approvals, or 22.1% of the state total.

New residents vs dwellings approved by LGA, 2024–25

Green bars show dwelling approvals; red bars show new residents added. Both are scaled to Playford = 100%, so where the red bar is longer, population growth is running ahead of new supply.

Bars scaled to Playford = 100%. Source: ABS Building Approvals (Cat. 8731.0), 2024–25 LGA cube; ABS Regional Population, 2024–25.

| LGA | New residents 2024–25 | Dwellings approved | New houses | Other residential |

|---|---|---|---|---|

| Playford | 4,357 | 2,302 | 2,113 | 180 |

| Port Adelaide Enfield | 1,650 | 1,027 | 772 | 250 |

| Charles Sturt | 1,400 | 1,463 | 538 | 919 |

| Onkaparinga | 1,588 | 890 | 648 | 235 |

| Mount Barker | 1,400 | 625 | 586 | 36 |

| Salisbury | 382 | 712 | 554 | 153 |

| Marion | 1,220 | 767 | 347 | 417 |

| Tea Tree Gully | 530 | 531 | 388 | 142 |

| SA total | 20,501 | 14,516 | 10,394 | 4,017 |

SA total new residents covers the whole state; Greater Adelaide growth was 18,647. New houses and other residential approvals do not sum to total approvals because conversion dwellings are recorded separately. Source: ABS Building Approvals (Cat. 8731.0), LGA data cube 87310DO016, April 2026 release; ABS Regional Population, 2024–25.

Note: LGA-level completion data is not publicly available from the ABS. Approvals are used as the closest available proxy for local housing delivery activity.

How are South Australian dwelling approvals tracking in 2025–26?

In the first ten months of 2025–26, from July 2025 to April 2026, South Australia approved 12,328 dwellings. This included 8,336 new houses and 3,878 other residential dwellings, with Greater Adelaide accounting for 10,068 approvals. Playford again recorded the highest total of any LGA, with 1,759 approvals, or 14.3% of the state total. It was followed by Charles Sturt with 1,168 approvals, Onkaparinga with 1,000 and Port Adelaide Enfield with 998. Port Adelaide Enfield moved into fourth place in the 2025–26 year-to-date figures, supported by a rise in medium-density approvals. The LGA recorded 511 other residential approvals in the first ten months of 2025–26, more than double its 2024–25 full-year pace.

| LGA | New houses | Other residential | Total dwellings |

|---|---|---|---|

| Playford | 1,530 | 226 | 1,759 |

| Charles Sturt | 503 | 661 | 1,168 |

| Onkaparinga | 602 | 390 | 1,000 |

| Port Adelaide Enfield | 482 | 511 | 998 |

| Salisbury | 570 | 266 | 841 |

| Marion | 256 | 469 | 730 |

| Mount Barker | 496 | 60 | 562 |

| Tea Tree Gully | 312 | 128 | 443 |

| SA total | 8,336 | 3,878 | 12,328 |

Figures cover the 2025–26 financial year to date, from July 2025 to April 2026. SA total includes all LGAs statewide. Source: ABS Building Approvals (Cat. 8731.0), LGA data cube 87310DO017, April 2026 release.

Section 02 · Approvals vs completions

South Australia building approvals and dwelling completions

South Australia approved 14,516 dwellings in 2024–25. Dwelling completions remained lower, with about 12,800 new residential dwellings completed over the four quarters to June 2025. In the December quarter of 2025, South Australian Treasury reported 3,726 dwelling completions, based on ABS Building Activity data.

On a total-approvals basis, this leaves a gap of about 1,700 dwellings. Excluding the 105 conversion dwellings included in the approvals total, the new-build gap is closer to 1,600 dwellings.

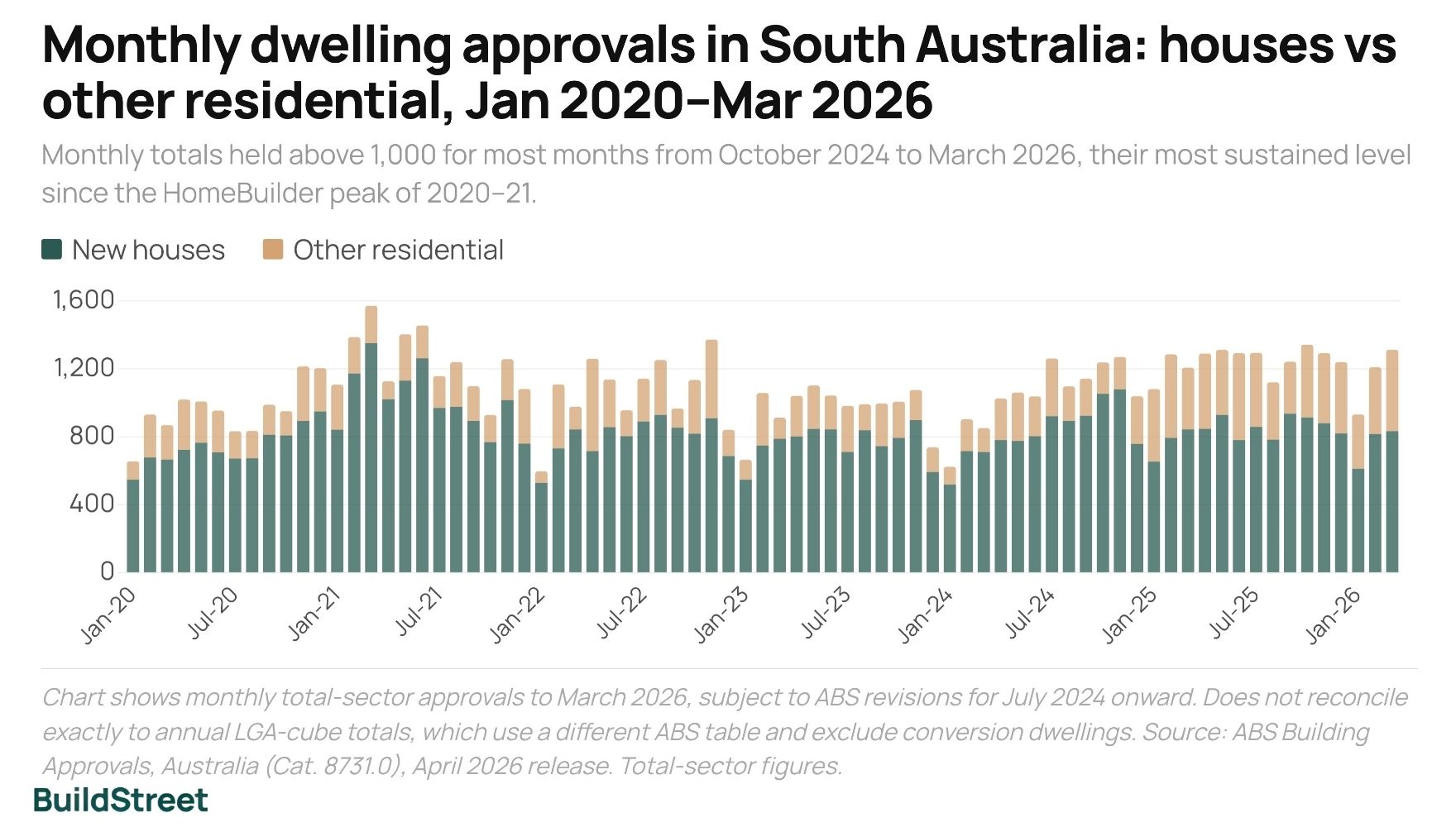

Monthly total approvals stayed above 1,000 in most months from October 2024 to March 2026, with January 2026 the main exception. House approvals exceeded 800 in 12 of those 18 months. An approval represents planning permission, while a completion represents a finished dwelling. The difference between approvals and completions shows how much approved supply has not yet converted into completed housing.

Monthly dwelling approvals in South Australia: houses vs other residential, Jan 2020–Mar 2026

Monthly totals held above 1,000 for most months from October 2024 to March 2026, their most sustained level since the HomeBuilder peak of 2020–21.

Chart shows monthly total-sector approvals to March 2026, subject to ABS revisions for July 2024 onward. Does not reconcile exactly to annual LGA-cube totals, which use a different ABS table and exclude conversion dwellings. Source: ABS Building Approvals, Australia (Cat. 8731.0), April 2026 release. Total-sector figures.

New dwellings approved, 2024–25

14,516

10,394 houses + 4,017 other residential

ABS Building Approvals (Cat. 8731.0)

New residential completed, 2024–25

12,800

Estimated sum of four quarters to Jun 2025

ABS Building Activity (Cat. 8752.0)

The 14,516 approvals figure includes 105 conversion dwellings. Houses plus other residential approvals total 14,411. Completions cover the four quarters to June 2025, new residential dwellings and total sectors. Source: ABS Building Approvals (Cat. 8731.0), LGA data cube 87310DO016, April 2026 release; ABS Building Activity (Cat. 8752.0).

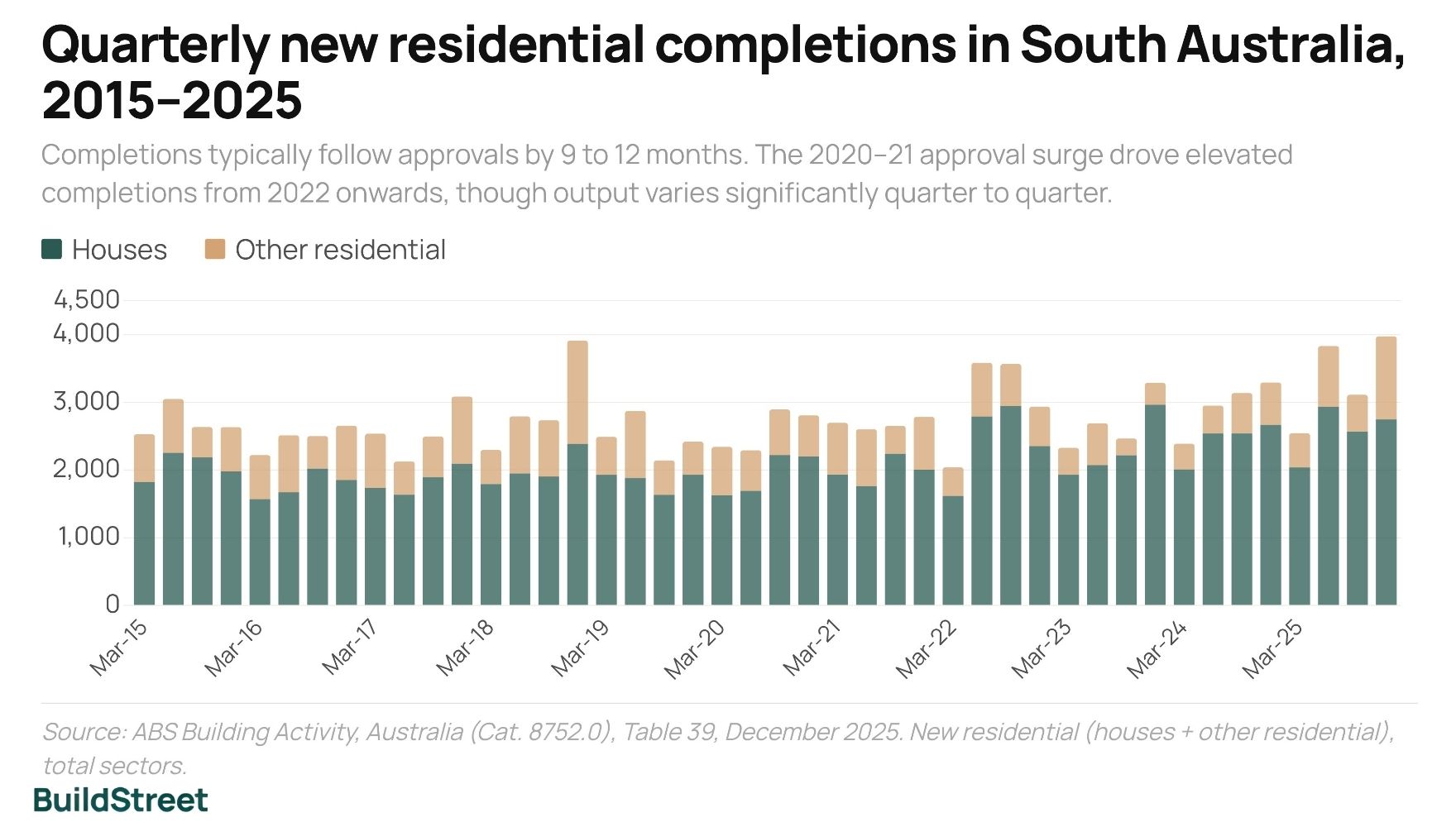

Quarterly new residential completions in South Australia, 2015–2025

Completions typically follow approvals by 9 to 12 months. The 2020–21 approval surge drove elevated completions from 2022 onwards, though output varies significantly quarter to quarter.

Source: ABS Building Activity, Australia (Cat. 8752.0), Table 39, December 2025. New residential (houses + other residential), total sectors.

Approvals have remained above completions

In 2024–25, South Australia approved 14,516 dwellings and completed around 12,800. This represents a gap of roughly 1,600 to 1,700 dwellings, depending on whether conversion dwellings are included. Quarterly completions were also uneven, falling to 3,111 in September 2025 before rising to 3,726 in December 2025.

Completions remained below approvals throughout 2024–25, with quarterly completions staying within a range of about 2,500 to 4,000 dwellings. While the gap was modest in individual quarters, it shows that approved dwellings were not being completed at the same pace as new approvals.

Section 03 · Growth corridors

How is infrastructure shaping Adelaide's growth corridors?

A $1.5 billion SA Water infrastructure package is intended to support tens of thousands of allotments across Adelaide's growth areas, including the northern corridor. The main constraint was not only planning policy, but physical servicing capacity. The Bolivar Wastewater Treatment Plant in the outer north had reached full capacity, while the Salisbury trunk main was also under pressure. Until both were upgraded, major releases could not proceed at the planned scale and Development Agreements for Infrastructure could not be issued. The Greater Adelaide Regional Plan identifies these corridors as key areas for future housing growth.

Key northern release areas, including Riverlea, Concordia and Two Wells, were therefore constrained by water and wastewater servicing capacity as well as the broader planning process. These areas could not proceed at their planned scale until the infrastructure constraints were addressed.

$1.5B

SA Water package

How was the northern corridor infrastructure package funded?

The package was funded through a $440 million direct budget allocation, increased developer contributions capped at $10,000 per lot, and a 3.5% above-inflation increase in residential water bills. The bill increase was reported as adding around $80 to $85 per household per year. The Premier was reported as saying that without the investment, growth fronts including Concordia and Two Wells had "no hope" of proceeding.

Northern corridor

Playford · Angle Vale · Concordia · Riverlea · Two Wells

Major

Growth corridor. Playford is projected to reach 166,334 residents by 2041, up 50,544 (43.6%) from its 2025 population of 115,790. Water and wastewater capacity, rather than planning policy, was the main constraint resolved by the SA Water package.

Southern corridor

Hackham · Aldinga · Sellicks Beach · Onkaparinga Heights

2,000+

Onkaparinga Heights (Hackham) is planned for 2,000+ allotments, backed by $30.5 million in state funding. The GARP notes that southern greenfield land will run out in the medium term at current demand rates.

Seaton (inner west)

Renewal SA, master-planned infill

1,315

$425.3 million state-funded. Includes 388 social and 197 affordable dwellings. A flagship government-backed project designed to show that inner-city infill can work at scale.

Southwark (inner north)

Renewal SA, master-planned infill

1,300

$104.7 million state-funded on former industrial land. Designed as a model for medium-density infill on government-owned urban sites, though the level of public investment in both projects suggests infill doesn’t yet stack up financially without government support.

Source: SA 2025–26 Budget Statement; Housing Roadmap 2024; PlanSA Local Area Population Projections; Greater Adelaide Regional Plan, current version.

Section 04 · Supply vs demand

Why is Adelaide's rental vacancy rate still so low?

Adelaide's rental vacancy rate held at 0.7% in May 2026, with 1,081 rental properties listed across metro Adelaide. This placed Adelaide among the tightest capital city rental markets, behind Darwin and Hobart and level with Perth. Combined advertised rents rose 4.9% over the year to June 2026, below the national average of 7.8% and behind Darwin at 14.0%, Hobart at 12.3% and Brisbane at 9.1%. SQM's three-week vacancy measure indicates a constrained rental market, with available rental stock well below the 2.5% to 3.0% range often used to indicate a more balanced market.

Adelaide rental vacancy rate, May 2026

0.7%

1,081 rental properties were available across metro Adelaide. SQM's three-week vacancy measure indicates a constrained rental market.

Balanced rental market: 2.5–3.0%

Selected rental vacancy rates by capital city vs the balanced market threshold, May 2026

The red line marks 2.5%, the lower bound of a balanced rental market. No major capital comes close. Adelaide's vacancy rate held at 0.7%, even as its annual rent growth of 4.9% to June 2026 ran below most other capitals.

Bars scaled to 4.0% axis maximum. Vacancy data, May 2026. Source: SQM Research, National Vacancy Rates and Weekly Rents, May 2026.

Fastest rent growth (Darwin)

+14.0%

Darwin recorded the highest annual rent growth of any capital city to June 2026. Adelaide's annual rent growth eased to 4.9%, placing it among the slower-growing capital city markets.

Completions, Dec Q 2025

3,726

Dwelling completions rose from 3,111 in the September quarter of 2025 to 3,726 in the December quarter.

SA Accord target met

78%

South Australia is projected to deliver 78% of its 84,000-dwelling Accord allocation, with full delivery not expected until March 2031.

South Australia is projected to fall 18,000 homes short of its Accord target

South Australia is projected to deliver 66,000 dwellings against its 84,000-home National Housing Accord allocation, leaving an estimated shortfall of 18,000 homes. At the current projected pace, full delivery is not expected until March 2031, which is 21 months after the June 2029 deadline.

The National Housing Accord targets 1.2 million new homes across Australia over the five years from mid-2024. South Australia's 84,000-home allocation reflects its roughly 7% share of the national population. Nationally, WA and the ACT are the only jurisdictions projected to meet their targets by June 2029. Australia as a whole is tracking at 82% of the Accord target, while NSW has the largest estimated shortfall, at 118,000 homes below its 376,000-dwelling allocation.

South Australia: National Housing Accord progress

SA's cumulative progress against its 84,000-home Accord allocation, due by June 2029. The vertical marker shows the straight-line target pace; latest inputs are approvals to March 2026 and completions to December 2025.

~37% (May 2026)

Approved

% of 84,000 Accord target

25,505 homes

est. Jul 2024 – Mar 2026

Built

completions to date

19,888 homes

est. Jul 2024 – Dec 2025

Expected Accord completion: March 2031, approximately 21 months late

At the current pace, SA is on track to reach its 84,000-home allocation around March 2031, roughly 21 months after the June 2029 deadline. That's an improvement on the previous five years, when SA built 54,000 homes, but still leaves a gap of 18,000 dwellings. Completions would need to pick up substantially to meet the deadline.

SA vs national Accord progress

South Australia

78%

66,000 of 84,000 target

Est. completion: Mar 2031

National average

82%

980,000 of 1.2M target

Est. completion: Sep 2030

On track (100%+)

2

WA and ACT only

All other states behind target

Pace markers are calculated pro-rata over the 60-month Accord period and differ by series because the data cut-offs differ: approvals run to March 2026 (21 months, 35.0%) and completions to December 2025 (18 months, 30.0%). The calendar-elapsed marker (~37%) reflects May 2026. Projected supply from NHSAC Table 4.1, early 2026 outlook. Sources: ABS; NHSAC, State of the Housing System 2026, Table 4.1.

| State/territory | Supply 2019–24 | Est. supply 2024–29 | Accord target | % of target met | Est. completion date |

|---|---|---|---|---|---|

| ACT | 24,000 | 22,000 | 21,000 | 103% | Jun-29 |

| WA | 75,000 | 129,000 | 129,000 | 100% | Jun-29 |

| VIC | 306,000 | 287,000 | 306,000 | 94% | Dec-29 |

| QLD | 166,000 | 204,000 | 246,000 | 83% | Sep-30 |

| SA | 54,000 | 66,000 | 84,000 | 78% | Mar-31 |

| NSW | 251,000 | 258,000 | 376,000 | 69% | Jun-31 |

| TAS | 16,000 | 13,000 | 26,000 | 51% | Dec-33 |

| NT | 3,000 | 4,000 | 11,000 | 34% | After 2034 |

| Australia | 896,000 | 980,000 | 1,200,000 | 82% | Sep-30 |

SA highlighted. WA and the ACT are the only jurisdictions projected to meet their Accord targets by June 2029. Source: NHSAC, Table 4.1, early 2026 outlook.

SA is not projected to meet its Accord target by June 2029

On current projections, South Australia will deliver about 66,000 homes against an 84,000-home target, leaving an estimated shortfall of 18,000 homes. This is above the 54,000 homes delivered in the previous five-year period, but the state is not projected to reach its full allocation until March 2031, after the June 2029 deadline.

| Capital city | Vacancy rate (May 2026) | Available properties | Annual rent growth | Status |

|---|---|---|---|---|

| Adelaide | 0.7% | 1,081 | +4.9% | Severely constrained |

| Perth | 0.7% | 1,265 | +6.8% | Severely constrained |

| Sydney | 1.5% | 10,820 | +7.6% | Tightening |

| Melbourne | 1.6% | 8,446 | +6.7% | Most balanced |

| National average | 1.2% | 37,844 | +7.8% | Under-supplied |

Vacancy data is for May 2026. Annual rent growth is for the week ending 12 June 2026 and covers combined houses and units. Source: SQM Research, National Vacancy Rates and Weekly Rents, May 2026.

Section 05 · Infill vs greenfield

How are infill targets and greenfield land prices reshaping Adelaide housing?

Detached houses made up 78% of South Australian dwelling approvals in calendar 2020. By 2025, that share had fallen to 67%, while apartments and townhouses rose from 22% to 33% over the same period. Despite this shift, detached houses still accounted for about two-thirds of all dwelling approvals, with much of that supply concentrated on the urban fringe.

Composition of dwellings approved: calendar 2020 vs calendar 2025

Detached houses still account for two-thirds of all approvals, despite an 11-point shift toward apartments and townhouses since 2020.

Shares calculated from monthly total-sector approvals summed over each calendar year. Source: ABS Building Approvals (Cat. 8731.0).

Greater Adelaide greenfield lot prices rose 23% in 2025 as sales fell

Greater Adelaide's median greenfield lot price rose 23% in 2025 to $377,135, the largest annual increase of any capital city, following an 18% rise the year before. Over the same period, greenfield lot sales fell 15% to 2,535. This indicates that price growth occurred while sales volumes declined, pointing to tighter development-ready land supply rather than stronger sales activity. Median lot sizes also fell below 400 sqm for the first time on record, which increased the land rate per square metre faster than the headline lot price.

Median lot price, 2025

$377,135

Up 23% on 2024; level with Perth as the equal most affordable capital city greenfield lot market

Median lot size, 2025

385 sqm

Down 6%; below 400 sqm for the first time on record

Land rate, 2025

$981/sqm

Up 31%; still the lowest capital city land rate per square metre

Greenfield lot sales, 2025

2,535

Down 15% on 2024 and 12% below the decade average

How much does a greenfield block cost in Adelaide?

Greater Adelaide's median greenfield lot price climbed 23% to $377,135 in 2025, while lot sales fell 15% to 2,535. The median lot size dropped to 385 sqm, below 400 sqm for the first time on record, lifting the land rate 31% to $981 per square metre. Higher prices, smaller lots and lower sales volumes indicate pressure in the supply of development-ready greenfield land.

+23%

lot price, 2025

Greater Adelaide lot prices rose while greenfield sales declined

Greater Adelaide's median greenfield lot price climbed 23% to $377,135 in 2025, while lot sales fell 15% to 2,535. The median lot size dropped to 385 sqm, below 400 sqm for the first time on record, lifting the land rate 31% to $981 per square metre. Higher prices, smaller lots and lower sales volumes indicate pressure in the supply of development-ready greenfield land.

Source: Urban Development Institute of Australia, State of the Land Report 2026 (pp. 8, 72–75, Greater Adelaide Greenfield Market Performance Summary Table); Researchfour. Figures are Greater Adelaide, calendar year 2025.

| Planning document | Infill target | Greenfield target | What happened |

|---|---|---|---|

| 30-Year Plan (2010) | ~70% | ~30% | Partially met |

| 30-Year Plan update (2017) | 85% | 15% | Target missed |

| GARP draft scenarios (2024) | 50–70% | 30–50% | Range tested |

| Current GARP | No fixed target | No fixed target | Rolling 15-yr land supply |

The current Greater Adelaide Regional Plan requires a minimum 15-year supply of zoned land, including five years of development-ready supply. Source: Greater Adelaide Regional Plan, current version; PlanSA; UDIA.

85%

2017 infill target

Greater Adelaide's fixed infill target was replaced with a rolling land-supply approach

The earlier 30-Year Plan set an infill-focused direction, and the 2017 update lifted the target to 85% of new housing within the existing urban footprint. That target was not met. The current Greater Adelaide Regional Plan removed fixed infill and greenfield ratios, replacing them with a rolling land-supply approach. Greater Adelaide's median greenfield lot price rose 23% in 2025 to $377,135, indicating pressure in the development-ready land market as the planning framework moved away from fixed infill targets.

Infill development in established suburbs can involve land assembly across fragmented private ownership, along with local infrastructure upgrades such as stormwater and power networks. Seaton and Southwark, which together represent more than $530 million in state investment, show the scale of public funding attached to some major infill precincts. These projects indicate that large-scale infill can require substantial upfront investment, particularly where government-owned land, infrastructure works and affordable housing commitments are involved.

General information only

This article draws on publicly available data from the Australian Bureau of Statistics, including building approvals, building activity and regional population data, as well as property vacancy data, the National Housing Supply and Affordability Council, South Australian planning documents and the 2025–26 South Australian Budget where indicated. It is general information only and does not constitute financial, investment or property advice. Estimates are subject to revision.

ABS, Building Approvals, Australia, April 2026 (formerly Cat. 8731.0), including LGA data cubes 87310DO016 and 87310DO017.

ABS, Building Activity, Australia, December 2025.

ABS, Regional population, 2024–25 financial year.

SQM Research, National Vacancy Rate Holds at 1.2%: National Asking Rents Rise by 7.8% Over the Past 12 Months, 15 June 2026.

PlanSA, Greater Adelaide Regional Plan.

PlanSA, Local Area Population Projections for South Australia, 2021 to 2041.

South Australian Government, Housing Roadmap, June 2024.

Premier of South Australia, More Homes for South Australians.

Premier of South Australia, Water investment delivering new homes for South Australian families.

InDaily, SA water bills to jump under state government plan, 25 June 2024.

South Australian Department of Treasury and Finance, 2025–26 Budget Statement.

South Australian Department of Treasury and Finance, Building Activity December 2025.

Urban Development Institute of Australia, State of the Land 2026, released March 2026.

Researchfour, Greater Adelaide Greenfield Market Performance data, calendar year 2025, cited in UDIA State of the Land 2026.

National Housing Supply and Affordability Council, State of the Housing System 2026, Table 4.1.

Chart Snapshots