Where is residential land still available in Australia?

Australia has large volumes of land zoned for housing across every state, but much of it is not yet ready to build on. In New South Wales, for example, 59% of zoned residential land is constrained, while in Queensland more than half of greenfield land is still waiting on infrastructure. This gap between zoned land and development-ready land is a key factor limiting how quickly new homes can be delivered.

Homes target by 2029

1.2M

National Housing Accord

Sydney greenfield supply

3.2 yrs

Most constrained market nationally

NSW zoned land constrained

59%

More than half of zoned land can't be built on yet

Greater Bunbury supply (WA)

55 yrs

Longest reported supply in Australia

Is it cheaper to build or buy in each capital city?

From 2015 to 2025, the cost gap between building and buying shifted in ways that weren't easy to predict. The advantage of building has held nationally, but the pandemic years threw construction economics into disarray, and the effects are still being felt.

Is it cheaper to build or buy in each capital city? →What does it cost to build a house in Australia?

Detached houses remain the dominant form of housing in Australia, but their grip has been loosening. In the 2021 Census — the most recent official stock count — the Australian Bureau of Statistics recorded 9,275,217 occupied private dwellings nationally.

What does it cost to build a house in Australia? →Section 01

Development-ready land by region

Land supply is measured differently across states, and definitions and reporting cycles are not consistent. The figures below provide a state-by-state view of available land, based on the most recent data.

New South Wales

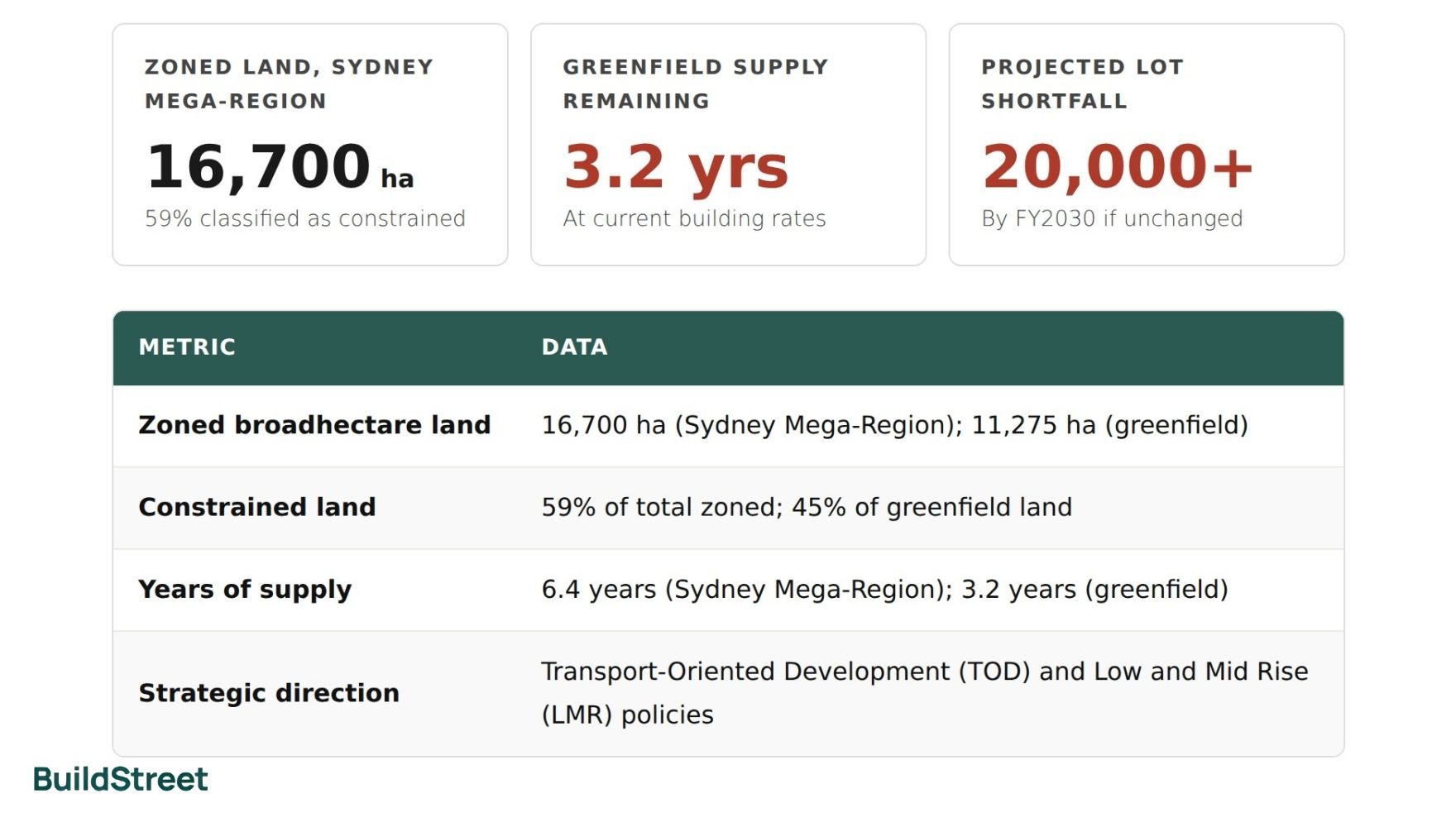

NSW has completed 55,625 new homes since July 2024, but the pipeline ahead is tight. Within the Sydney Mega-Region, 59% of zoned residential land is constrained and cannot deliver housing as planned. Only 3.2 years of greenfield supply remain at current rates, and 89% of lots expected over the next eight years aren't development-ready. The main constraints are infrastructure funding gaps and biodiversity requirements.

In the Lower Hunter alone, 22,800 homes are delayed due to unfunded road upgrades. The government has committed $237 million to bring 14,000 of those forward.

Zoned land, Sydney Mega-Region

16,700 ha

59% classified as constrained

Greenfield supply remaining

3.2 yrs

At current building rates

Projected lot shortfall

20,000+

By FY2030 if unchanged

| Metric | Data |

|---|---|

| Zoned broadhectare land | 16,700 ha (Sydney Mega-Region); 11,275 ha (greenfield) |

| Constrained land | 59% of total zoned; 45% of greenfield land |

| Years of supply | 6.4 years (Sydney Mega-Region); 3.2 years (greenfield) |

| Strategic direction | Transport-Oriented Development (TOD) and Low and Mid Rise (LMR) policies |

Victoria

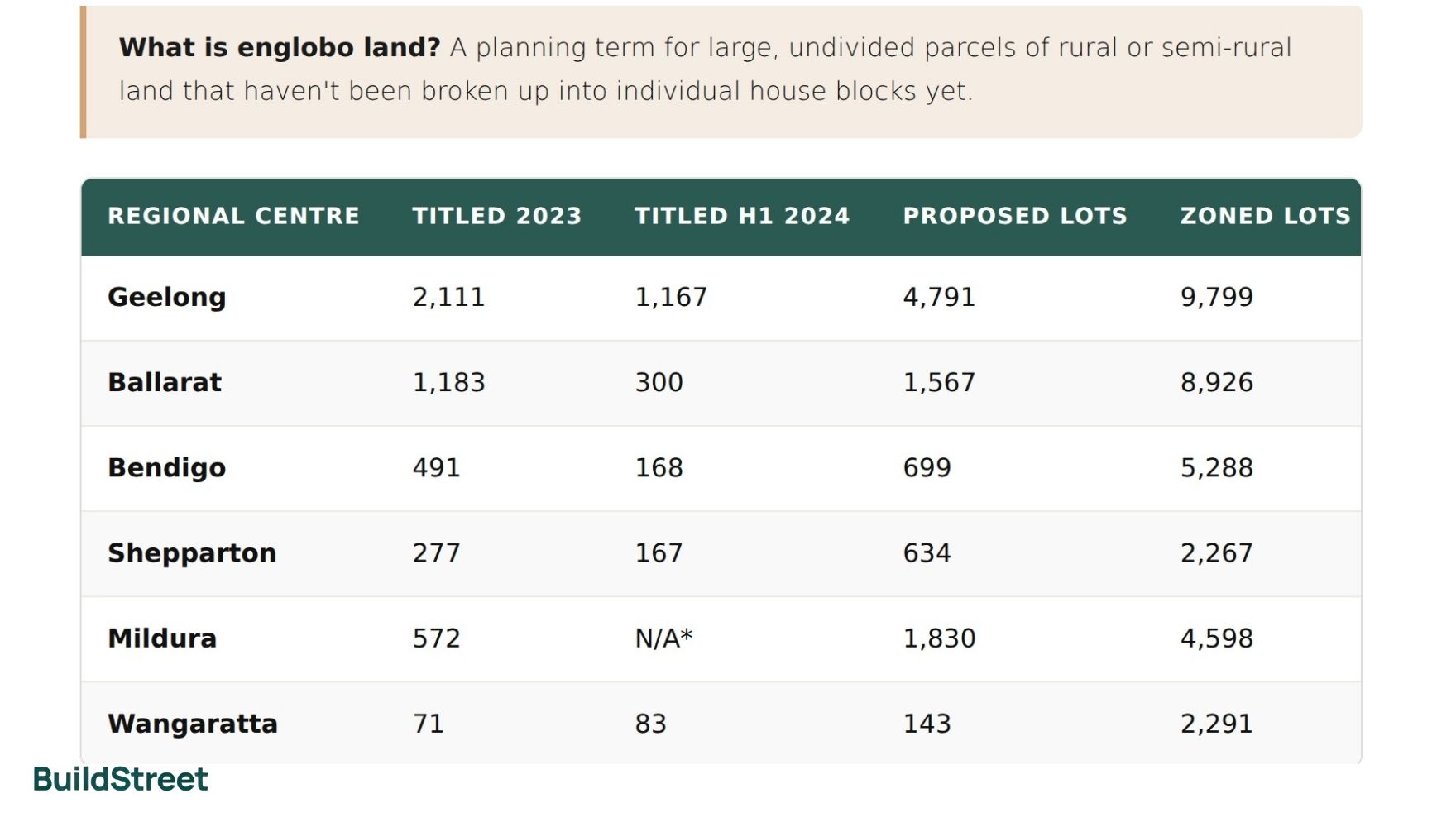

Victoria is running greenfield estates on the outer fringe alongside denser infill in established suburbs. As of January 2025, Melbourne's growth corridors held over 294,000 lots across zoned and unzoned englobo land, with 39,812 actively in subdivision. But delivery is slowing. Only 18,543 greenfield lots were titled in 2024, down from 22,727 the year before. The apartment pipeline holds 158,533 dwellings at various stages.

| Regional Centre | Titled 2023 | Titled H1 2024 | Proposed Lots | Zoned Lots |

|---|---|---|---|---|

| Geelong | 2,111 | 1,167 | 4,791 | 9,799 |

| Ballarat | 1,183 | 300 | 1,567 | 8,926 |

| Bendigo | 491 | 168 | 699 | 5,288 |

| Shepparton | 277 | 167 | 634 | 2,267 |

| Mildura | 572 | N/A* | 1,830 | 4,598 |

| Wangaratta | 71 | 83 | 143 | 2,291 |

* N/A — Data not available for H1 2024 at the time of reporting. Source: Victorian Urban Development Program 2025.

| Metric | Data |

|---|---|

| Active subdivision pipeline | 39,812 proposed greenfield lots |

| Lots titled in 2024 | 18,543 (down from 22,727 in 2023) |

| Infill pipeline | 158,533 dwellings at various stages |

| Years of supply (regional) | Up to 31 years (e.g., Horsham) |

Queensland

Queensland has zoned capacity for nearly 580,000 greenfield homes and over 1,000,000 infill homes. The bottleneck is infrastructure, not zoning. More than half of existing greenfield land is idle, waiting on roads, water and sewerage. EDQ approved 8,003 dwellings in Priority Development Areas in 2024–25 and committed $100.5 million to unlock 3,500+ homes. South East Queensland needs 104,000 more homes by 2029.

| Metric | Data |

|---|---|

| Zoned broadhectare capacity | ~580,000 homes (greenfield); ~1,000,000 homes (infill) |

| Infrastructure constraint | Over half of greenfield land awaits infrastructure |

| EDQ approvals (2024–25) | 8,003 dwellings in Priority Development Areas |

| Target supply balance | 70% infill / 30% greenfield (ShapingSEQ 2023) |

| Years of supply | Minimum 15 years (planned); 4 years (approved) |

Western Australia

WA has one of the largest raw land supplies in the country, with roughly 117,420 hectares of zoned land across Perth, Peel and Greater Bunbury, and over 26,000 hectares still undeveloped. It also filters supply by environmental constraint groups (A, B and C), making its figures more reliable than most states. Lot approvals surged 38% to nearly 24,000 in the year to June 2025. The weak spot is infill, sitting at just 39% against a much higher long-term target.

| Region | Urbanised Area (ha) | Undeveloped Area (ha) | Total Zoned (ha) |

|---|---|---|---|

| Perth Metropolitan | 78,510 | 19,790 | 98,300 |

| Peel Region | 6,550 | 2,580 | 9,140 |

| Greater Bunbury | 6,640 | 3,700 | 10,340 |

| Metric | Data |

|---|---|

| Total zoned land | 117,420 ha across Perth, Peel, and Greater Bunbury |

| Undeveloped zoned land | 26,070 ha |

| Residential lot approvals (2025) | ~24,000 (38% increase year-on-year) |

| Actual infill rate | 39% (below long-term strategic targets) |

| Years of supply | 20–26 years (Perth/Peel); 55 years (Greater Bunbury) |

South Australia

SA law requires the government to hold at least 15 years of residential land supply before unlocking new greenfield land. Greater Adelaide has 139,000 allotments already zoned and ready, well above that threshold. SA is also rolling out the largest land release in state history: 25,000 homes across Dry Creek, Concordia and Hackham. Infill historically dominates, making up 67% of new supply between 2020 and mid-2022.

| Metric | Data |

|---|---|

| Zoned allotments | ~139,000 (Greater Adelaide) |

| Total lots identified | 203,759+ |

| New mega land release | 25,000+ homes (Dry Creek, Concordia, Hackham) |

| Infill vs greenfield | 67% infill / 20% greenfield (2020–2022) |

| Years of supply | 15+ years (statutory minimum maintained) |

Tasmania

Tasmania focuses on building within its existing urban boundary rather than expanding outward. Spatial analysis found capacity for over 34,000 dwellings inside that boundary, enough to meet the 30-year forecast demand of 30,000 homes. However, areas like Scottsdale carry 35 to 40 years of theoretical supply on paper that doesn't hold up in reality. Steep terrain means many lots can't connect to standard sewerage, making them too expensive to develop.

| Metric | Data |

|---|---|

| Identified dwelling capacity | 34,000+ within existing urban boundary |

| Target supply split | 70% infill / 30% greenfield |

| Demand forecast (30 years) | ~30,000 new homes |

| Key constraint | Topography (downslope sewerage limitations) |

| Years of supply (some areas) | 35–40 years on paper (e.g., Scottsdale) |

Australian Capital Territory

The ACT releases all residential land through the Indicative Land Release Program (ILRP), a rolling five-year government plan. The current ILRP targets 21,422 new homes by 2028–29, with at least 70% as infill and 15% reserved for affordable housing. In practice, slow land servicing and rising construction costs have pushed prices up. Median block prices in Denman Prospect reached $725,000, up 4.7% in six months.

| Metric | Data |

|---|---|

| New homes targeted (2024–2029) | 21,422 via ILRP |

| Infill vs greenfield mandate | 70% infill / 30% greenfield (legally binding) |

| Affordable housing requirement | 15% of annual land releases |

| Median block price (Denman Prospect) | $725,000 (+4.7% in 6 months) |

Northern Territory

The NT has struggled to get land to market efficiently. A government review led to 23 recommendations; 15 have been actioned, cutting red tape and speeding up approvals. The Land Development Corporation (LDC) delivers residential land in Zuccoli, Kilgariff and Fannie Bay. Commencements fell below 100 per quarter in late 2023, the lowest in 30 years, but are forecast to recover to 730 in 2024–25 and peak at 990 in 2026–27.

| Metric | Data |

|---|---|

| Land pipeline | 20-year forward forecast via Land Development Strategy |

| Development-ready land | "Land Under Development": developer-held with connected services |

| Forecast commencements | 730 in 2024–25; 990 in 2026–27 |

| Key delivery body | Land Development Corporation (LDC) |

Section 02

Greenfield and infill housing targets by state

Several states and territories have set targets to increase the share of housing delivered through infill development, including apartments and townhouses in established suburbs. These policies are designed to reduce reliance on outer-fringe greenfield estates, where new roads, schools, water and sewerage infrastructure are often required.

| Jurisdiction | Target Ratio (Infill : Greenfield) | Status |

|---|---|---|

| ACT | 70% : 30% | Legally binding |

| Tasmania | 70% : 30% | Greater Hobart Plan mandate |

| Queensland | 70% : 30% | ShapingSEQ 2023 target |

| South Australia | ~67% : 20% | Historically achieved |

| Western Australia | Higher target; 39% achieved | Below long-term target |

| NSW | Focus on TOD & LMR policies | Policy-driven shift |

Apartment and townhouse projects can be more difficult to deliver where construction costs, planning requirements, labour availability and project feasibility affect development timelines. In some markets, these factors may limit how quickly infill housing can be added compared with greenfield estates.

Section 03

Years of supply: what do the numbers actually mean?

Years of supply figures vary sharply between states and are calculated differently. They measure theoretical zoned capacity, not land that's actually ready to build on. Three structural problems explain why decades of supply on paper can shrink to just a few usable years in practice.

| Jurisdiction | Reported Years of Supply | How It's Calculated |

|---|---|---|

| WA |

20–26 yrsPerth / Peel

55 yrsGreater Bunbury

|

Undeveloped urban-zoned land divided by the 20-year historical annual consumption rate. |

| SA |

15+ yrsGreater Adelaide — statutory minimum

|

139,000 zoned allotments measured against average demographic growth rates. |

| VIC (Regional) |

Up to 31 yrse.g., Horsham

|

Zoned capacity under current land use settings divided by upside demand scenarios (e.g., 82 dwellings/year). |

| TAS |

35–40 yrse.g., Scottsdale

|

Identified residential lots measured against localised population forecasts. |

| NSW |

6.4 yrsSydney Mega-Region

3.2 yrsGreenfield only

|

Unconstrained zoned land measured against annual delivery rates required by the Housing Accord. |

| QLD |

Min. 15 yrsPlanned supply

Min. 4 yrsApproved supply

|

Statutory minimums tracked by the Growth Monitoring Unit against projected demand under ShapingSEQ. |

| ACT |

Rolling 5 yrsOverall supply

~12 yrsMulti-unit infill

|

Managed via the ILRP rolling release plan, with infill capacity modelled against current demographics. |

| NT |

11 yrsGreater Darwin

8 yrsKatherine

27 yrsTennant Creek

|

"Land Under Development" (developer-held, infrastructure connected) measured against NT Treasury demand forecasts. |

Infrastructure funding gaps

Land generally needs roads, water and sewerage before housing can be delivered. In Sydney's Mega-Region, 59% of zoned land is constrained because supporting infrastructure has not yet been funded. Until funding and delivery arrangements are resolved, some zoned land may remain unavailable for development.

Environmental and biodiversity rules

Broad zoning maps do not always capture environmental constraints. Western Australia adjusts its land supply figures using environmental constraint groups, while other states report these constraints differently. In some areas, biodiversity requirements can reduce the amount of zoned land that is practical or feasible to develop.

Land fragmentation and difficult terrain

Some large residential land parcels are split across multiple owners, which can slow land assembly and subdivision. Site conditions can also affect delivery. In Tasmania, for example, steep terrain can make standard sewerage connections difficult, reducing the amount of land that is practically development-ready.

General information only

This article is based on publicly available government and industry data. It is general information only and does not constitute financial or property advice. If you are making decisions about land or property purchases, consider speaking with a licensed financial adviser or property professional.

- NHSAC State of the Housing System 2025, May 2025

- NHSAC State of the Housing System 2025, May 2024

- UDIA State of the Land Report

- NSW Urban Development Program (UDP)

- Victorian Urban Development Program 2025

- Queensland Growth Monitoring Unit / QGSO Broadhectare Studies

- WA Urban Growth Monitor Report 17

- SA PlanSA

- 30-Year Greater Hobart Plan

- ACT Indicative Land Release Program 2024–29

- NT Land Development Strategy

Chart Snapshots