Is Australia on Track to Build 1.2 Million Homes by June 2029?

Australia has completed 262,592 homes in the first six quarters of the National Housing Accord, leaving the country 97,408 homes behind the pace needed to reach 1.2 million by June 2029.

Australia is still not on track. In August 2023, National Cabinet committed to building 1.2 million new, well-located homes over five years. To hit that number, the construction industry needs to average 240,000 completions every year through to June 2029, at 20,000 homes a month for 60 straight months. Data for the first 18 months shows Australia is building faster than the 2023–24 trough, but it remains well behind the required pace.

National Housing Accord target

1.2M

New homes by 30 June 2029

Required pace (unmet)

20,000/mo

240,000 completions per year, every year

Actual pace (first 18 months)

14,588/mo

262,592 completions · ABS Building Activity, Dec 2025

What the Accord actually set out to do

The original 2022 National Housing Accord targeted one million homes. But population growth outpaced expectations, with roughly 1.5 million people arriving in Australia between 2023 and 2025 alone, prompting National Cabinet to lift the target to 1.2 million in August 2023. The $3 billion New Home Bonus rewards states and territories that exceed their per-capita share, while the $500 million Housing Support Program funds infrastructure to unlock well-located land. The target also includes 20,000 affordable homes co-funded by the Commonwealth and the states.

The gap so far, in plain numbers

ABS data shows 262,592 completions over the first six quarters of the Accord. At that pace, the five-year total would reach about 875,000 homes, roughly 325,000 short of target. Expert forecasts put the shortfall between 166,000 (Master Builders Australia) and 262,000 (NHSAC). Even the most optimistic forecast has Australia delivering only around 83–86% of what the target requires.

Target pace vs actual pace for Australia's 1.2 million homes target

To put 240,000 annual completions in context: the best year Australia managed in the decade before the Accord was around 225,000 dwellings. The target asks the industry to beat that record every year for five years, while carrying a chronic labour shortage and a backlog of multi-year projects.

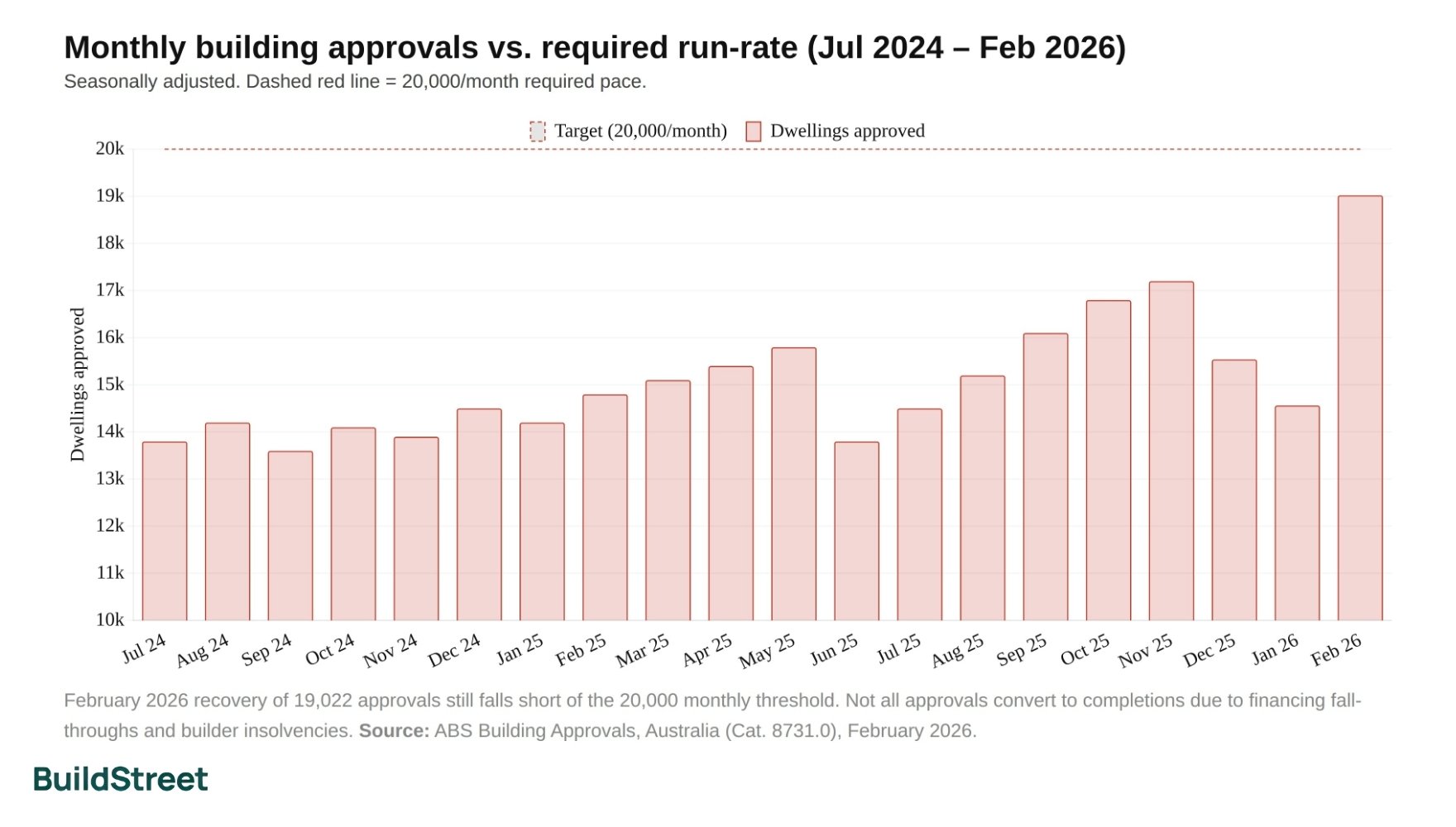

The NHSAC's first quarterly progress report (March 2026) confirmed that building approvals and commencements have both risen 17% nationally since the Accord began. Physical completions are what count toward the target, and at 262,592 across six quarters, the monthly average sits at around 14,588, some 27% below the required 20,000 per month.

Monthly building approvals vs. required run-rate (Jul 2024 – Feb 2026)

Seasonally adjusted. Dashed red line = 20,000/month required pace.

- Dwellings approved

February 2026 recovery of 19,022 approvals still falls short of the 20,000 monthly threshold. Not all approvals convert to completions due to financing fall-throughs and builder insolvencies. Source: ABS Building Approvals, Australia (Cat. 8731.0), February 2026.

| Period | Total approved | Monthly change | Year-on-year | Key driver |

|---|---|---|---|---|

| December 2025 | 15,540 | −9% | n/a | Sharp 31.4% drop in multi-unit approvals, the most volatile segment. |

| January 2026 | 14,564 | −7.2% | −15.7% | Continued softness; private houses steady at 9,753 (+1.1%). |

| February 2026 | 19,022 | +29.7% | +14.0% | Multi-unit surge: +101.2% MoM to 8,922 units. Houses flat at 9,847. |

Building Approvals: seasonally adjusted, ABS Building Approvals, Australia (Cat. 8731.0). Building Activity: seasonally adjusted, ABS Building Activity, Australia (Cat. 8752.0). The February 2026 recovery of 19,022 approvals still falls short of the 20,000 monthly threshold. Dec 2025 commencements of 53,567 annualise to around 214,000, still below the 240,000 annual target. Not all approvals convert to completions.

Quarter-by-quarter Accord tracker

| Quarter | Actual completions | Quarterly gap | Cumulative actual | Cumulative target | Cumulative gap |

|---|---|---|---|---|---|

| Sep 2024 | 44,618 | −15,382 | 44,618 | 60,000 | −15,382 |

| Dec 2024 | 45,317 | −14,683 | 89,935 | 120,000 | −30,065 |

| Mar 2025 | 43,584 | −16,416 | 133,519 | 180,000 | −46,481 |

| Jun 2025 | 41,233 | −18,767 | 174,752 | 240,000 | −65,248 |

| Sep 2025 | 44,304 | −15,696 | 219,056 | 300,000 | −80,944 |

| Dec 2025 | 43,536 | −16,464 | 262,592 | 360,000 | −97,408 |

Straight-line target = 60,000 per quarter (240,000 per year). Completions have averaged 43,765 per quarter, roughly 73% of the required pace. Six of the Accord's 20 quarters have elapsed but only 21.9% of the target has been delivered. Source: ABS Building Activity, Australia, December 2025 (seasonally adjusted, with revisions to earlier quarters).

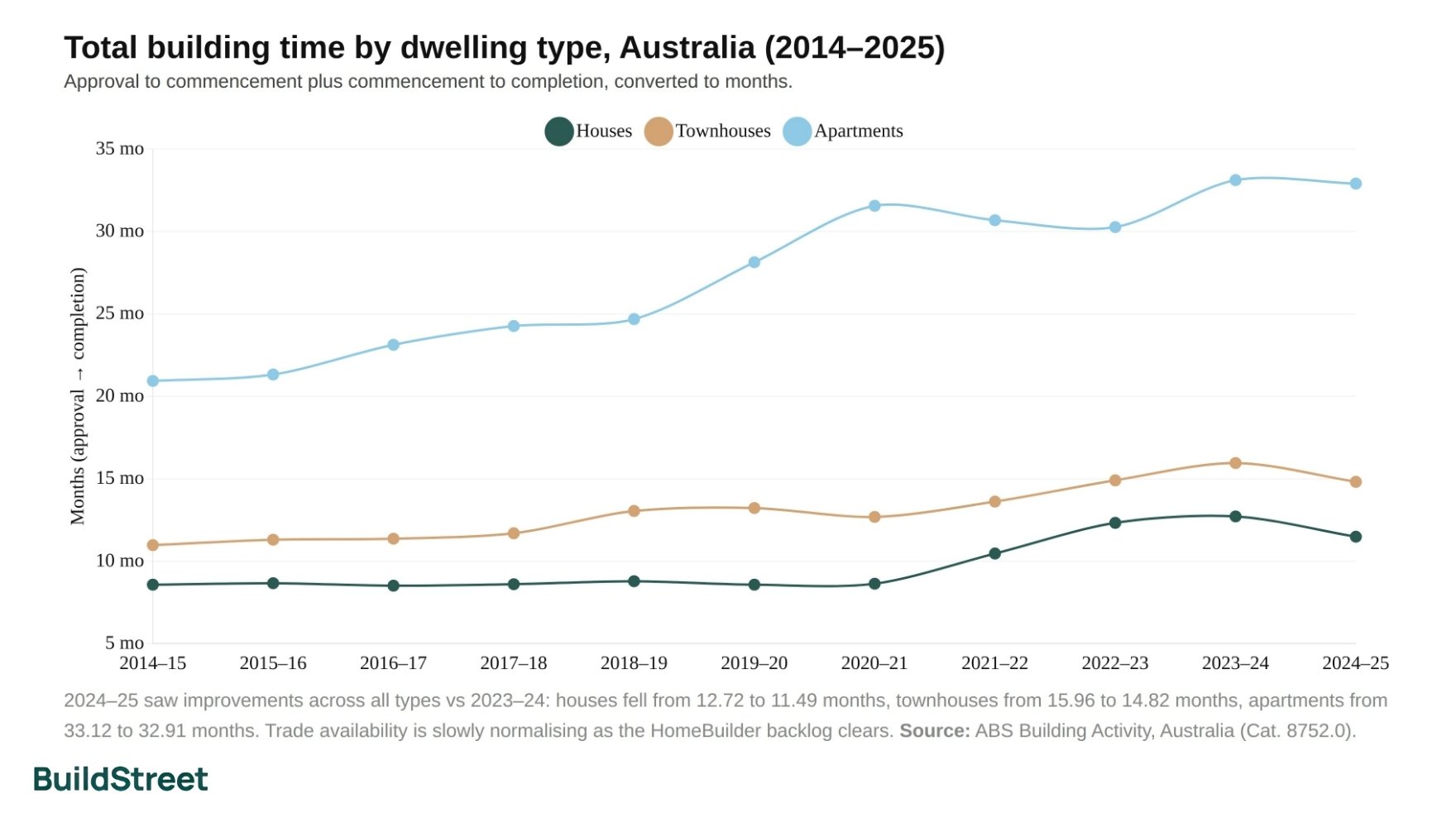

The building time blowout: how long it actually takes to finish a home in 2025

Longer build times are one of the biggest drags on the target. The longer a home takes to finish, the longer capital and trades are locked in, choking the flow of new projects. The pipeline gets bigger, but supply does not.

Total house building time (from approval to completion) has risen from 8.58 months in 2019–20 to 11.49 months in 2024–25. Apartments are in a worse position: build times stretched from 28.14 months to 32.91 months over the same period.

Total building time by dwelling type, Australia (2014–2025)

Approval to commencement plus commencement to completion, converted to months.

2024–25 saw improvements across all types vs 2023–24: houses fell from 12.72 to 11.49 months, townhouses from 15.96 to 14.82 months, apartments from 33.12 to 32.91 months. Trade availability is slowly normalising as the HomeBuilder backlog clears. Source: ABS Building Activity, Australia (Cat. 8752.0).

State-by-state comparison of housing targets and delivery

The Accord splits the 1.2 million target across states and territories on a per-capita basis. Master Builders Australia's five-year forecast shows no state or territory is on track to fully meet its share, with gaps ranging from a 4.3% shortfall in WA to a 66% deficit in the NT.

| State / Territory | Accord target | MBA forecast | Shortfall | Gap |

|---|---|---|---|---|

| New South Wales | 375,730 | 303,280 | −72,460 | −19.3% |

| Victoria | 306,940 | 286,500 | −20,440 | −6.7% |

| Queensland | 245,980 | 224,282 | −21,698 | −8.8% |

| Western Australia | 129,700 | 124,128 | −5,572 | −4.3% |

| South Australia | 83,430 | 58,527 | −24,903 | −29.8% |

| Tasmania | 25,810 | 14,304 | −11,506 | −44.6% |

| ACT | 21,030 | 19,100 | −1,930 | −9.1% |

| Northern Territory | 11,380 | 3,841 | −7,539 | −66.2% |

| National total | 1,200,000 | 1,033,962 | −166,038 | −13.8% |

The NHSAC projects a larger shortfall of approximately 262,000 based on more conservative assumptions on interest rates and multi-unit feasibility. Source: Master Builders Australia, Building and Construction Industry Forecasts.

- New South Wales has the largest allocation (375,730 homes) but only 15% built against a 25% pace benchmark. Approvals are up 8% and completions up 21%, with 70,000+ homes under construction, but NSW isn't expected to complete its share until June 2031, two years late.

- Victoria targets 800,000 homes over ten years, more ambitious than its federal share, yet recorded its lowest annual completions since 2014 in the year to September 2025. Approvals have fallen 1%, and the state's high property tax burden and projected $192.6 billion net debt are pushing developer capital to other states.

- Queensland and Western Australia are the standout performers. QLD approvals are up 16% and completions up 26%. WA is the closest large state to its target at a 4.3% projected shortfall, with completions surging 29%. Both are expected to complete their share by September 2029.

- South Australia, Tasmania and the Northern Territory face the deepest gaps: SA at 30% below target, Tasmania at 45% and the NT at 66%. In smaller markets, planning reform only goes so far; industry capacity is the binding constraint.

Forecast delivery as a share of Accord target, by state

MBA five-year projection to June 2029. Green = within 5% of target; amber = 6–20% behind; red = 20%+ behind.

No state or territory is forecast to fully meet its per-capita share by June 2029. WA at 95.7% is the closest; the NT at 33.7% is the furthest behind. Source: Master Builders Australia, Building and Construction Industry Forecasts.

Forecast volumes tell only part of the story. The NHSAC's March 2026 quarterly report also projects when each state is likely to complete its Accord share, based on current approval and build rates. Only Victoria, Western Australia and the ACT are tracking close to the June 2029 deadline.

When each state is on pace to complete its Housing Accord share

| State / Territory | Share approved to date | Share built to date | Gap to 25% pace | Expected completion |

|---|---|---|---|---|

| New South Wales | 21% | 15% | −10 pp | Jun 2031 |

| Victoria | 28% | 23% | −2 pp | Sep 2029 |

| Queensland | 26% | 17% | −8 pp | Sep 2030 |

| South Australia | 27% | 19% | −6 pp | Sep 2030 |

| Western Australia | 29% | 22% | −3 pp | Sep 2029 |

| Tasmania | 15% | 12% | −13 pp | Sep 2033 |

| Northern Territory | 9% | 5% | −20 pp | After 2034 |

| ACT | 25% | 23% | −2 pp | Sep 2029 |

| Australia | 25% | 18% | −7 pp | Jun 2030 |

pp = percentage points. "Gap to 25% pace" is the difference between each state's share built to date and the NHSAC's 25% benchmark at the six-quarter mark. Green = within 3 pp; amber = 4–9 pp behind; red = 10+ pp behind. State and territory targets are implied population-share targets, not formal negotiated quotas. Source: NHSAC Quarterly Report, March 2026.

The size of the shortfall: three forecasts, one clear answer

Australia's three leading forecasters all agree the 1.2 million target won't be met. Where they differ is on how large the miss will be.

NHSAC projection (most pessimistic)

−262,000

Avg. 183k/yr rising to 197k · 78% of target

HIA projection (middle estimate)

−190,000

1.01M forecast starts · 84% of target

MBA projection (most optimistic)

−166,000

1.034M forecast starts · 86% of target

- The NHSAC projects gross supply averaging 183,000 dwellings per year to early 2027, rising to a peak of 197,000 by 2028–29. That peak barely matches the pre-Accord decade average and falls around 43,000 homes per year short of target. The Council's conclusion: for every five homes the target demands, the industry is on track to build four.

- The HIA has progressively upgraded its forecast to 1.01 million commencements as approvals recover. Multi-unit starts are projected to nearly double from their 2024 trough to around 100,000 per year by 2029. That optimism hinges on one assumption: rising house prices restoring the financial viability of off-the-plan apartments. If prices rise enough, the shortfall narrows. If rates stay elevated, it widens.

- Master Builders Australia forecasts 1.034 million starts, a 13.8% miss, based on detailed state-by-state capacity modelling. The MBA also notes the Accord launched from its weakest starting point in over a decade: FY 2023–24 recorded just 158,690 new starts, an 8.8% annual fall.

The chart below maps each forecaster's projected annual output against the 240,000-per-year required rate. All three project steady acceleration through 2027–29, but none reaches 240,000 in any single year.

Annual completions: Year 1 confirmed vs. three forecast scenarios (FY 2024–25 to FY 2028–29)

FY 2024–25 is confirmed at 174,752. FY 2025–26 onwards are MBA, HIA and NHSAC projected annual completions.

- Required (240k/yr)

- MBA forecast

- HIA forecast

- NHSAC forecast

FY 2024–25 completions are confirmed at 174,752, the shared starting point for all three scenarios. The MBA projects a climb to around 220,000 by FY 2028–29; the NHSAC peaks near 205,000. No scenario reaches 240,000 in any year of the Accord. Source: ABS Building Activity, Australia (Cat. 8752.0); Master Builders Australia; Housing Industry Association; NHSAC.

What's actually holding the build back

The gap is not a demand problem. Australians need housing urgently. It is a supply-side problem, and no single policy can resolve it on its own.

- Labour shortage. BuildSkills Australia estimates the sector needs 90,000 additional workers immediately to meet the Accord target, with the biggest gaps in bricklaying, carpentry, tiling and roofing. A shortfall in one trade delays every trade that follows. Skilled migration helps, but it also adds to housing demand.

- Costs at a permanently elevated baseline. Construction costs are up 39.7% since before the pandemic. The NHSAC confirmed costs are now 0.9% lower in real terms than at the Accord's start, a positive sign, but the absolute baseline remains elevated. A 2025 feasibility review found that mid-rise apartment projects cannot deliver a standard profit margin in mainland capitals without subsidy or lower land costs.

- Planning reform is uneven. NSW and VIC have introduced major top-down changes, but local council implementation is inconsistent. Resident opposition, planning tribunal backlogs and politically-charged rezonings add time to approvals and cost to projects.

- Apartments are still the missing piece. Multi-unit dwellings account for the bulk of homes needed to reach 1.2 million; detached houses cannot fill the gap alone. The high-density sector has been largely stalled since 2022. Developers need pre-sales to start, buyers are hesitant at current borrowing costs, and banks will not release finance without enough pre-sales. This deadlock is beginning to ease, but it has already cost the Accord its first two years of apartment pipeline.

The road ahead: slow progress is still progress

Australia is still falling short. Even on the MBA's most optimistic forecast, the country will miss about 1 in 8 of the homes needed by June 2029. On the NHSAC's central forecast, the shortfall is closer to 1 in 5.

The second half of 2025 brought some genuine momentum. Commencements and completions improved in consecutive quarters. Build times eased across every state. NSW planning approvals are moving 15% faster under the Housing Delivery Authority. While February 2026's 101% spike in multi-unit approvals is volatile, it may be the first real sign that the long-delayed apartment pipeline is starting to move.

For people building now, two practical points stand out:

- Trade availability is improving as the HomeBuilder backlog clears. The build time data across most states confirms this trend is real.

- Competition for trades will likely intensify again by 2027–28 as the apartment pipeline scales up. The next 12 to 18 months may represent better trade availability than what follows.

General information only

This article is based on publicly available ABS data and third-party forecasts. It is general information only and does not constitute financial or investment advice. If you are making decisions about saving for a property purchase, consider speaking with a licensed financial adviser.

ABS Building Approvals, Australia (Cat. 8731.0), February 2026

ABS Building Activity, Australia (Cat. 8752.0), December Quarter 2025

ABS Average Dwelling Completion Times

NHSAC, State of the Housing System 2025

NHSAC Quarterly Progress Report, March 2026

Master Builders Australia, Building and Construction Industry Forecasts

Housing Industry Association, Housing and Economic Outlook Report

Treasury.gov.au, National Housing Accord

Institute of Public Affairs, 36,000 Homes Behind Target

Western Sydney University / NHSAC, 262,000 shortfall modelling

Chart Snapshots