Queensland construction pipeline: where new homes are being built

Queensland approved 41,997 dwellings in 2025, up 12.7 per cent on 2024 and the strongest result since 2021. More than half of those approvals were in Greater Brisbane, showing how heavily the state's pipeline depends on South East Queensland.

Approvals are not yet turning into finished homes fast enough. Queensland commenced 41,157 dwellings in 2025 but completed 32,912, leaving an 8,245-home gap between starts and completions. The state's one million-home target requires a delivery pace of roughly 50,000 homes a year, a level Queensland has not yet consistently achieved.

QLD dwelling approvals, 2025

41,997

+12.7% vs 2024 · ABS Building Approvals

Greater Brisbane share of approvals

53.6%

22,502 dwellings · ABS GCCSA geography

Commencements vs completions gap

−8,245

41,157 commenced, 32,912 completed in 2025

QLD population growth rate (yr to Dec 2024)

1.9%

~23% of all national population growth · QGSO

Homes for Queenslanders target

1 million

New homes by 2046 · ~50,000 completions/yr implied

Fastest-growing SA2 (2024–25)

+15.4%

Ripley, Ipswich · QGSO Regional Population

SECTION 01 · SEQ DOMINANCE

Why South East Queensland dominates housing growth

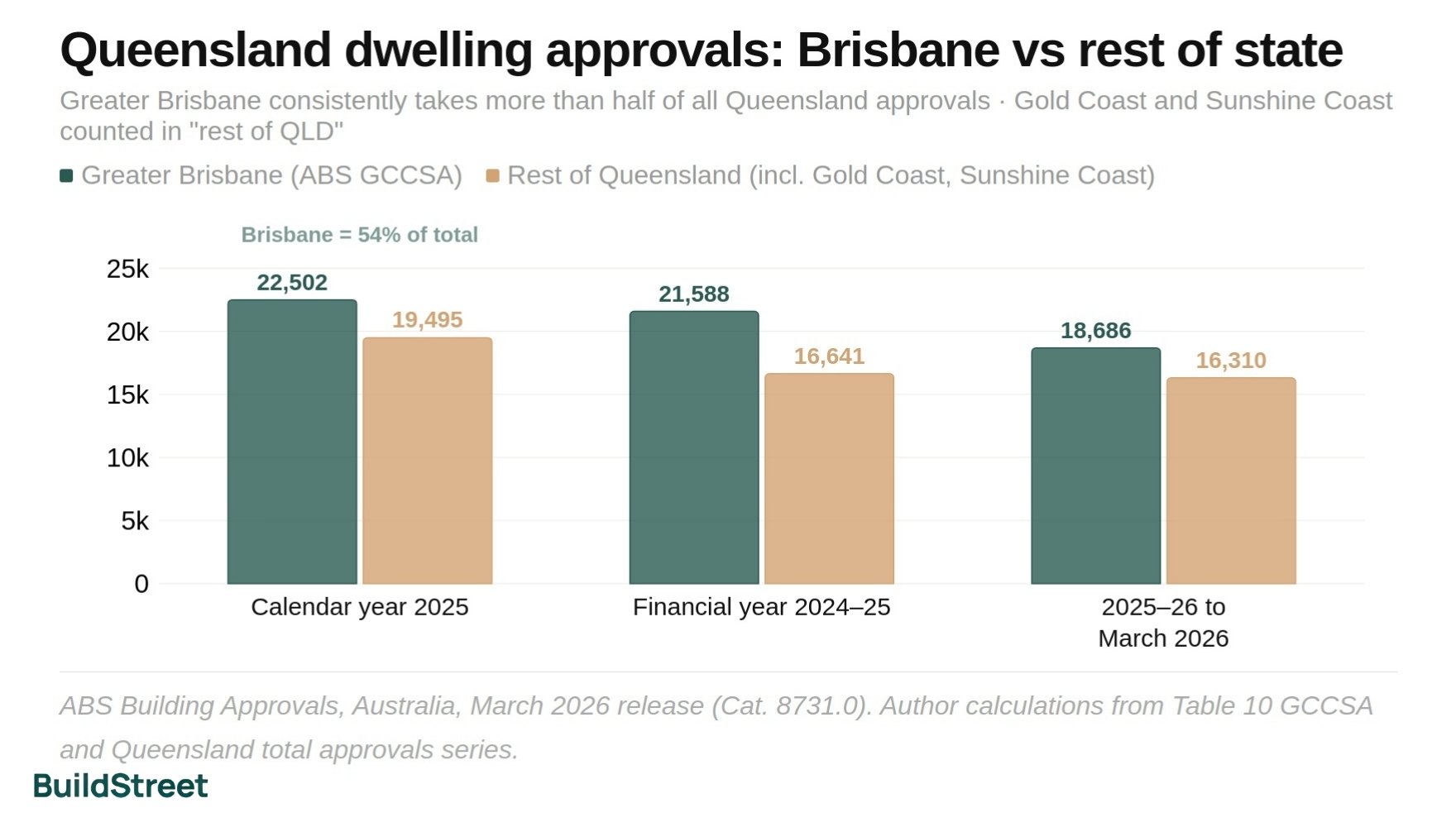

Greater Brisbane accounted for 53.6 per cent of Queensland's dwelling approvals in 2025. But this does not show the full scale of growth in South East Queensland. The Gold Coast and Sunshine Coast are counted as "rest of Queensland" in ABS data, even though they are part of the wider coastal growth corridor.

South East Queensland has grown faster than the rest of the state every year since 1992. Growth became even stronger after the pandemic. In 2022–23, the region's population grew by 3.0 per cent, the fastest rate on record. Over the previous decade, the rest of Queensland grew by just 0.7 per cent a year on average.

Growth is coming from both interstate and overseas migration. Many people moving from other states are choosing South East Queensland for jobs, lifestyle and lower housing costs than Sydney and Melbourne. Overseas migration has also risen sharply. Queensland received 87,954 net overseas migrants in the year to September 2023, up 170 per cent on pre-COVID levels. Most settled in the south-east.

Queensland dwelling approvals: Greater Brisbane vs rest of Queensland

Greater Brisbane consistently takes more than half of all Queensland approvals. Gold Coast and Sunshine Coast are counted in "rest of Queensland" due to ABS geographic definitions, so the true SEQ share is higher.

Source: Author calculations from ABS Table 10 GCCSA approvals and Queensland total approvals. ABS Building Approvals, Australia, March 2026 release.

In 2024–25, Queensland's six largest local government area (LGA) population gains were all in South East Queensland. Brisbane added 21,464 people, followed by Logan (11,949), the Gold Coast (11,944), Moreton Bay (10,951), Ipswich (9,138) and the Sunshine Coast (7,659).

Seven of Queensland's ten most populated LGAs are also in South East Queensland. Australia's geographic centre of population also shifted 1.5 kilometres south-east in 2024–25, showing that national growth is moving in the same direction.

Overseas migration drove 77 per cent of Gold Coast population growth in 2023–24. The city had 691,230 residents at June 2025 and is projected to reach over one million people by 2046, a 54 per cent increase from its 2021 base. That is a larger projected gain than any other SA4 outside Greater Brisbane. It shows that Gold Coast housing demand is likely to remain a long-term pressure, rather than a short-term cycle.

The Sunshine Coast is growing mainly through internal migration, people relocating from other states and from within Queensland rather than from overseas. The LGA had 381,957 residents at June 2025 and added 7,659 in the year. Population projections put the SA4 at 611,513 by 2046, up from 403,521 in 2021. This type of growth tends to support more demand for lower-density housing, rather than the high-rise apartment pipeline seen on the Gold Coast.

SECTION 02 · WESTERN CORRIDORS

Western growth corridors: Ipswich, Logan and Moreton Bay

Ipswich was Queensland's fastest-growing LGA in 2024–25 at 3.5 per cent. Logan has the largest dwelling pipeline of any Queensland council, with 105,895 expected dwellings as at December 2025. Moreton Bay also added 10,951 residents in 2024–25 and is home to Waraba, Queensland's largest active Priority Development Area. These western and south-western corridors are taking on more of the state's housing task. They are also where the gap between approved lots and finished homes has been most persistent.

Fastest-growing LGA in Queensland in 2024–25. Ripley Valley grew 15.4%, the fastest SA2 growth rate in the state.

Expected dwelling yield as at December 2025, the largest of any council area in Queensland.

Residents added in 2024–25. Moreton Bay includes Waraba, a major Priority Development Area expected to deliver about 30,000 dwellings.

Population data: QGSO Regional Population Growth 2024–25. Dwelling pipeline: QGSO Residential Land Supply and Development, December 2025.

Priority Development Areas approved 8,003 dwellings in 2024–25, up 15 per cent year-on-year. They now account for about half of South East Queensland's greenfield supply.

The state's facilitated development pathway also received more than 150 expressions of interest in the first half of 2024. These projects could deliver around 30,000 dwellings across Queensland. This activity is helping move greenfield land through the approval process. However, most of the supply is still new outer-suburban land rather than infill.

Lot sizes are also shrinking as land is used more efficiently. In Greater Brisbane, the average site area for approved new houses fell from 571 square metres in 2012 to 459 square metres in 2021, a 20 per cent reduction.

SECTION 03 · APPROVALS CYCLE

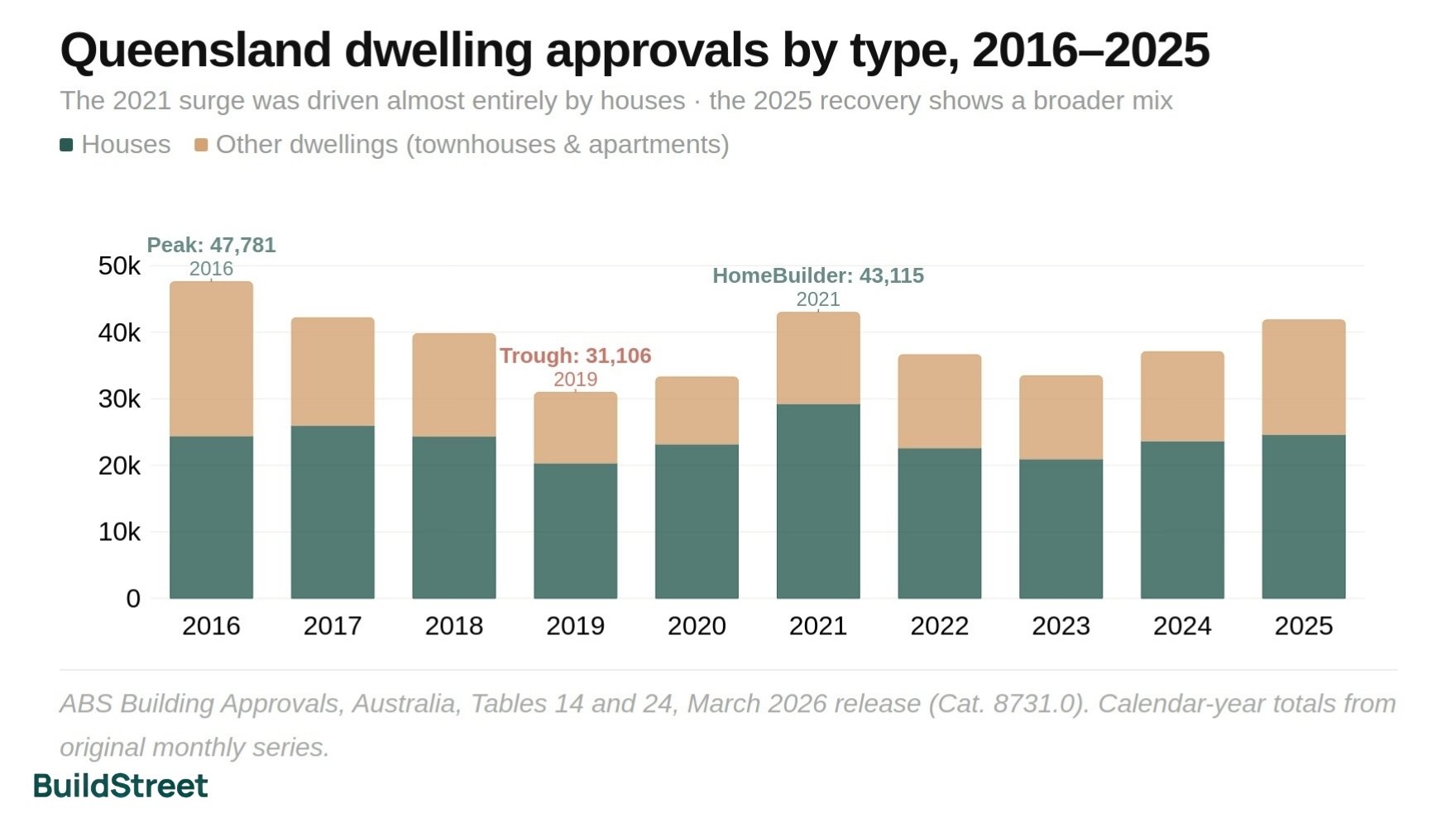

Queensland's approvals cycle: a decade of volatility

Queensland's approvals peaked at 47,781 in 2016, fell to 31,106 in 2019, rose again to 43,115 in 2021 following the federal HomeBuilder stimulus, then fell again before the current recovery. The 2025 total of 41,997 is the strongest since 2021, though still below the 2016 high.

The main difference between the 2025 recovery and the 2021 increase is the dwelling mix. The 2021 lift was concentrated in detached houses. The 2025 recovery includes a clearer return of apartments and townhouses, with the non-house share rising more strongly than at any point since 2016. That matters because detached houses alone are unlikely to absorb the scale of population growth forecast in western corridors and inner-city areas where land is becoming scarcer.

Queensland dwelling approvals by type, 2016–2025

The 2021 surge was driven almost entirely by houses. The 2025 recovery shows a broader mix, with the non-house share at its highest since 2016.

Source: ABS Building Approvals, Australia, Table 14 and Table 24, March 2026 release. Calendar-year totals are author calculations from original monthly series.

Cycle peak. Apartment approvals at 23,176, the decade high. Overseas investor demand and low interest rates drove a concentrated apartment pipeline in inner Brisbane that took years to complete and created localised oversupply.

Cycle trough. Apartment approvals fell to 10,629 as developers pulled back on new projects. Tighter credit conditions, falling land values and the aftermath of apartment oversupply all weighed on the pipeline at the same time.

HomeBuilder surge, but mostly detached houses. The federal stimulus pushed house approvals to 29,248, the highest since 2016. Apartments barely moved. The recovery was concentrated in houses, adding to the cost and labour pressures that followed.

Post-stimulus correction. Rate rises, construction cost blowouts and builder insolvencies all weighed on new approvals. The backlog from 2021 was still moving through the system while new projects were harder to make financially viable.

A broader recovery. Houses at 24,626 and other dwellings at 17,232, the strongest attached-dwelling result since 2016. With 9,921 apartment approvals in buildings of four storeys or more, higher-density supply is back in the pipeline.

Source: ABS Building Approvals, Australia, Table 14, March 2026 release. Annual changes are year-on-year comparisons.

SECTION 04 · APARTMENTS

Why did apartment approvals slow after 2016?

Other dwelling approvals, covering townhouses, terraces and apartments, fell from 23,176 in 2016 to 10,629 in 2019, a 54 per cent drop in three years. By 2023 they had only partially recovered to 12,505. The 2025 figure of 17,232 is the strongest since 2016, but the apartment share of Queensland's total pipeline is only just returning to levels that were common a decade ago.

Houses vs other dwellings approved, Queensland 2016–2025

"Other dwellings" fell sharply after 2016 and recovered slowly. Houses held steady and surged in 2021. The gap narrowed in 2025 as apartment approvals lifted.

"Other dwellings" includes townhouses, terraces, semi-detached dwellings and apartments. Source: ABS Building Approvals, Australia, Table 14 and Table 24, March 2026 release.

Four factors drove the decline and have continued to limit apartment supply:

SECTION 05 · DWELLING MIX

What is being built: the current dwelling mix

Of Queensland's 41,858 new residential dwelling approvals in 2025, houses accounted for 58.8 per cent. Townhouses and semi-detached dwellings made up 14.3 per cent, and apartments 26.8 per cent. Townhouses, semi-detached homes and apartments made up 41.2 per cent of approvals — the highest non-house share since 2016 — though detached houses still dominate.

Totals cover new residential buildings only, which is why the sum (41,858) differs slightly from the all-dwellings total (41,997). Average lot size data: ABS, New houses being built on smaller blocks. Source: ABS Building Approvals, Australia, Table 24, March 2026 release.

Policy is pushing for more density. Homes for Queenslanders allocates a $350 million Incentivising Infill Fund and requires each council to meet mandatory targets by dwelling type, not just total numbers. ShapingSEQ 2023 sets a target of 900,000 new homes in South East Queensland by 2046, including 100,000 homes close to jobs and transport. However, houses still accounted for nearly six in ten approvals in 2025, showing that detached housing remains the largest part of Queensland's current pipeline.

SECTION 06 · DELIVERY GAP

Is Queensland building enough homes each year?

Queensland completed 32,912 homes in 2025. The state's target implies around 50,000 a year. That gap of more than 17,000 homes is where the pressure lies. Approvals and commencements are trending up, but a home that is approved or started but not yet handed over does not house anyone.

Strongest since 2021. Trend approvals running ~47,700 annualised as at March 2026.

~66% of the ~50,000/yr pace the state target implies. Gap to commencements: 8,245.

Rising strongly, but completions typically lag commencements by 12–24 months.

Plus 4,798 approved but not yet commenced. Large pipeline, slow conversion.

Source: ABS Building Approvals, Australia, March 2026 release (approvals); ABS Building Activity, Australia, December 2025 release (commencements, completions, under construction).

The 48,044 dwellings under construction at December 2025 represent a large pipeline of future completions. However, a large pipeline has not always translated quickly into finished homes. The pattern since 2021 has been sustained gaps between starts and completions, driven by labour shortages, insolvencies and cost blowouts rather than a shortage of approved projects.

The same pressure is showing up nationally. Australia completed an estimated 177,000 homes in 2024 against underlying demand of around 223,000, a net shortfall of roughly 68,000 households. No state or territory is on track to meet its share of the National Housing Accord's 1.2 million target by June 2029. The projected national shortfall is around 262,000 homes.

SECTION 07 · LABOUR & DELAYS

Construction labour shortages and delivery delays

Queensland commenced 41,157 dwellings in 2025 and completed 32,912, a shortfall of 8,245 homes. That gap is not a one-off, as similar shortfalls appeared in 2021 and 2024. Each time, the causes were the same. Not enough skilled tradespeople. Constrained subcontractor capacity. Backlogs of partly-finished work competing for the same labour pool across multiple projects at once.

Insolvency data: Scale Suite, Australian Business Insolvency by Industry 2026. Wage target: industry reporting on 2026 enterprise agreement rounds. Infrastructure competition: RLB Australia Market Intelligence Update Q1 2026.

When builders become insolvent, fewer firms are available to take on new work. This can reduce competition and place upward pressure on construction costs. National construction cost growth was running at 3.4 per cent a year as at December 2025 — slower than the 2021–22 peak, but still compounding onto a base that has risen significantly since 2020.

Queensland dwelling commencements vs completions, 2016–2025

The gap that opened in 2021 has never fully closed. Commencements have been outpacing completions for most of the past four years.

Calendar-year totals are author calculations from ABS quarterly original building-activity tables. Source: ABS Building Activity, Australia, December 2025 release.

SECTION 08 · CATCH-UP

Can Queensland completions catch up with approvals?

At December 2025, Queensland had 48,044 dwellings under construction and a further 4,798 approved but not yet started. That is a substantial active pipeline that will eventually convert into completions. Rising commencements through 2025 point to more finished homes in 2026 and 2027. But pipeline size alone does not guarantee a quick conversion.

In 2021, Queensland commenced 44,657 dwellings but completed only 31,829. The gap of nearly 13,000 homes took roughly two years to clear. Builder insolvencies removed some projects from the pipeline entirely, while rising construction costs made others harder to complete.

Source: ABS Building Activity, Australia, December 2025 release. 2021 commencement figure is the calendar-year total from the original quarterly series.

Commencements are projected to peak at around 53,430 homes in financial year 2027–28. If completions follow with the typical lag, Queensland could approach the 50,000-a-year pace by 2028 or 2029. However, reaching that pace once would not be enough. The one-million-home target requires Queensland to sustain that level of delivery for around two decades.

SECTION 09 · 1 MILLION TARGET

What Queensland's 1 million-home target means

Delivering one million homes by 2046 requires around 45,500 dwellings a year on a straight-line basis, or closer to 50,000 once front-loaded demand and the social housing component are accounted for. Queensland completed 32,912 homes in 2025. The Homes for Queenslanders plan sets the ambition, including 53,500 social homes and mandatory dwelling-type targets for each council, but 95 per cent of the supply must come through the private sector.

Where Queensland sits against the implied annual pace

The ~50,000/yr figure is derived from industry analysis of the Homes for Queenslanders target. Straight-line from plan figures gives ~45,500/yr. Projected peak commencements: Master Builders QLD / HIA, April 2024. Source: Queensland Government Homes for Queenslanders; ABS Building Activity, December 2025 release.

Key policy measures include mandatory council-level housing targets by dwelling type, a $350 million Infill Fund, and the Priority Development Area programme. ShapingSEQ 2023 sets a target of 900,000 new homes in South East Queensland by 2046, including 100,000 homes close to jobs and transport. This infill target sits alongside Queensland's ongoing greenfield land release programme in the western growth corridors.

| Policy component | Detail |

|---|---|

| Social housing target | 53,500 social homes by 2046, backed by $1.25 billion over five years from 2028. Delivery rate of at least 2,000 homes/yr from that point. 1,315 already delivered at time of publication. |

| Private sector dependency | ~95% of the target relies on private delivery, leaving the plan exposed to the same feasibility, finance and construction capacity constraints that are currently slowing completions. |

| Dwelling type targets | Council-level targets now specify dwelling type, not just total numbers — a shift from earlier plans that set volume targets without specifying how much supply needed to be attached or higher-density. |

SECTION 10 · REGIONAL QLD

Regional Queensland: a clear second tier of growth

Regional Queensland grew at an average of 0.7 per cent a year over the decade to June 2023, less than half the SEQ rate. That average covers a wide range. Several regional markets are growing well above it, and population projections to 2046 show a clear hierarchy of where housing demand will concentrate outside the south-east.

Wide Bay, covering Hervey Bay, Bundaberg and the Fraser Coast, was the fastest-growing regional SA4 outside SEQ in 2022–23 at 2.1 per cent. Its growth was driven by lifestyle migration from South East Queensland. Cairns was second, supported by tourism recovery and increased infrastructure investment. Townsville and Toowoomba are the largest regional service economies, and both are expected to record sustained population growth over the next two decades.

| Region (SA4) | Projected gain to 2046 | Annual avg growth | Primary growth driver | Relative scale |

|---|---|---|---|---|

| Gold Coast | +351,964 | 1.7% | Overseas migration (77%) |

|

| Sunshine Coast | +207,992 | 1.7% | Internal migration |

|

| Cairns | +76,493 | 1.3% | Tourism, lifestyle, infrastructure |

|

| Townsville | +65,955 | 1.1% | Defence, services |

|

| Mackay–Isaac–Whitsunday | +52,812 | 1.0% | Resources, tourism |

|

| Central Queensland | +51,686 | 1.0% | Resources, services |

|

| Wide Bay | +48,467 | 1.1% | Lifestyle migration from SEQ |

|

| Toowoomba | +40,233 | 1.1% | Services, agriculture |

|

Gold Coast and Sunshine Coast SA4s sit outside the ABS Greater Brisbane GCCSA boundary but are included here as part of the broader SEQ growth corridor. Projected interstate migration gains to 2046: Gold Coast +146,000, Sunshine Coast +87,000, Wide Bay +38,000, Cairns +28,000. LGA-level approvals are published separately in the ABS Building Approvals LGA data cubes. Source: QGSO Population Projections 2023 edition, SA4 medium series; QGSO Regional Population Growth 2024–25.

The Gold Coast and Sunshine Coast are in a different league to the rest of regional Queensland, each projected to add more than 200,000 people by 2046. Cairns, Townsville, Mackay and Central Queensland form the next group, each projected to grow by 50,000 to 80,000 people over the same period. Each market has distinct housing needs. The Gold Coast, shaped by overseas migration, requires more higher-density product; Wide Bay and Toowoomba, driven by lifestyle relocation, remain predominantly detached housing markets.

General information only

This article is based on publicly available ABS data, Queensland Government publications and official QGSO releases. It is general information only and does not constitute financial or investment advice. Data is current to May 2026; some figures may be subject to ABS revision in subsequent releases. The next ABS Building Activity release (March 2026 quarter) is scheduled for 8 July 2026.

ABS Building Approvals, Australia, March 2026 release (Cat. 8731.0)

ABS Building Activity, Australia, December 2025 release (Cat. 8752.0)

QGSO Regional Population Growth 2024–25

QGSO Population Projections, SA4 series, 2023 edition

QGSO Population Growth Highlights and Trends, Queensland Regions, 2024 edition

Queensland Government, Homes for Queenslanders

ShapingSEQ 2023, Queensland Government

NHSAC State of the Housing System, May 2025

ABS, New houses being built on smaller blocks

Economic Development Queensland, 2024–25 Snapshot

Centre for Population, Regional Population 2023–24

Master Builders Queensland, Homes for Queenslanders analysis

RLB Australia Market Intelligence Update Q1 2026

Scale Suite, Australian Business Insolvency by Industry 2026

QGSO Residential Land Supply and Development

Chart Snapshots