Construction labour shortages in Australia: which trades are most needed?

Australia's construction workforce has reached a record 1.37 million workers, but the sector is still short of the trades needed to keep up with housing demand. Core residential trades are in shortage across states and territories, while job vacancies remain well above pre-pandemic levels.

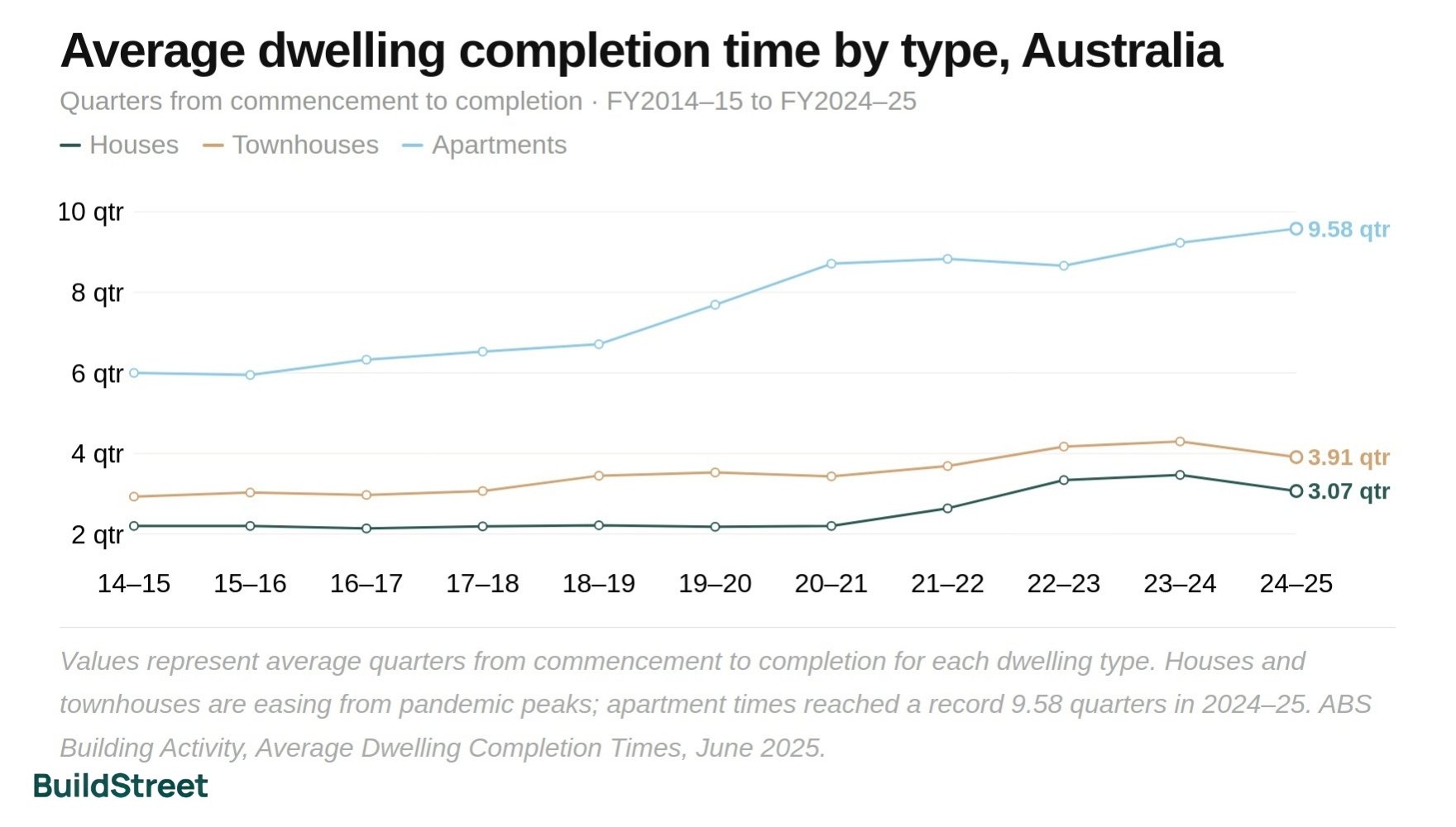

The strain is showing in the delivery numbers. House build times have risen from 2.18 quarters in 2019–20 to 3.07 quarters in 2024–25, apartment build times have reached a record 9.58 quarters, and construction costs are now 39% above their 2019 level.

Construction workforce

1.37M

Trend employment, Feb 2026, a record high

Job vacancies (Feb 2026)

21,600

30% above the 2019 annual average

Trades in national shortage

13 of 15

Core housing trades tracked, JSA 2025; all states affected

Is Australia on track to build 1.2 million homes by June 2029?

Australia has completed 262,592 homes in the first six quarters of the National Housing Accord, well short of the 360,000 needed to stay on pace. Labour shortages remain one of the central constraints on supply.

Read full article →How long does it take to build a house in Australia?

The average new house now takes 3.07 quarters to complete, up from 2.18 in 2019-20. Post-pandemic build times are still elevated, even as delays for houses and townhouses start to ease.

Read full article →SECTION 01 · SHORTAGE OVERVIEW

The state of Australia's construction workforce

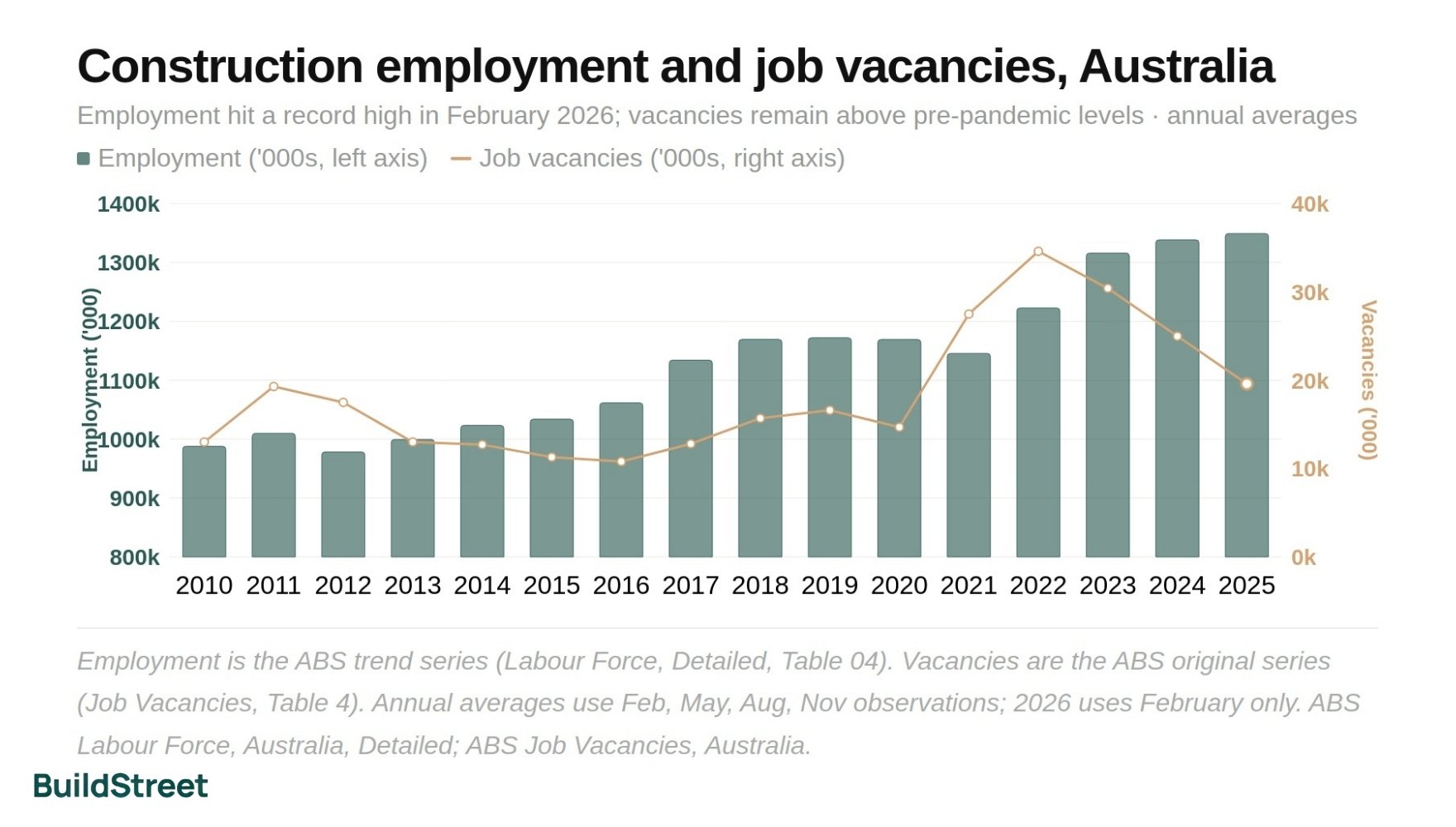

The construction industry employed a record 1.37 million workers in February 2026 and still could not fill 21,600 job vacancies. Even after falling 46% from the May 2022 peak, vacancies remain 30% above the 2019 annual average. The workforce has never been larger, and it is still not large enough.

Construction is classified as an industry under heightened shortage pressure. Nationally, 30% of all occupations were in shortage in 2025, down from 36% in 2023, and tradespeople and technicians account for 53% of the 123 occupations in continuous shortage since 2021.

Against that backdrop, 13 of 15 core residential trades remain in shortage across every state and territory.

Construction employment and job vacancies, Australia

Employment hit a record high in February 2026, while vacancies remain well above pre-pandemic levels. Annual averages shown.

- Employment ('000, trend)

- Vacancies ('000)

2010

Methodology: Employment is the ABS trend series from Labour Force, Australia, Detailed (Table 04). Vacancies are the ABS original series from Job Vacancies, Australia (Table 4). Annual averages use quarterly observations (Feb, May, Aug, Nov); the 2026 column uses February 2026 only. Source: ABS Labour Force, Australia, Detailed, Table 04; ABS Job Vacancies, Australia, Table 4.

About the trade counts in this article: Three occupation groups are used depending on context. The headline stat card and heatmap cover 15 core residential trades drawn from the shortage list. The trade summary table groups those into 10 occupation categories for readability. The state breadth comparison uses 19 housing-related occupations from the full six-digit download, which includes additional plumber subcategories and electrician subclasses not shown in the heatmap.

SECTION 02 · TRADES IN SHORTAGE

Which construction trades are in shortage in Australia?

Of the 15 core residential building trades tracked nationally, 13 are in shortage across every state and territory. The exceptions are Building Associates, which is affected only in the Northern Territory, and Project Builder, which is affected only in Tasmania and the ACT. The shortage type differs by trade, and that distinction matters for how each gap can be closed.

The trades divide into three shortage types, each requiring a different response.

| Trade group | 2025 status | Jurisdiction breadth | Shortage driver | Employment |

|---|---|---|---|---|

| Carpenters and joiners | Shortage | All 8 jurisdictions | Retention gap | 149,600 |

| Electricians (general) | Shortage | All 8 jurisdictions | Suitability gap | 197,300 |

| Plumbers (general) | Shortage | All 8 jurisdictions | Long training gap | 53,400 |

| Bricklayers and stonemasons | Shortage | All 8 jurisdictions | Suitability gap | 25,464 (unit group) |

| Plasterers and renderers | Shortage | All 8 jurisdictions | Suitability gap | Not specified |

| Wall and floor tilers | Shortage | All 8 jurisdictions | Suitability gap | Not specified |

| Painters | Shortage | All 8 jurisdictions | Retention gap | Not specified |

| Roof tilers | Shortage | All 8 jurisdictions | Not separately identified | 9,400 |

| Construction project managers | Shortage | All 8 jurisdictions | Suitability gap | 134,300 |

| Building associates | Not short | NT only | Not specified | Not specified |

Source: Jobs and Skills Australia 2025 Occupation Shortage List (six-digit download); JSA 2025 Occupation Shortage Drivers tables; JSA occupation profiles.

About the employment figures: Employment counts differ depending on whether an occupation is measured at the specific occupation level or the broader unit-group level. This article uses the specific occupation figure where available (e.g. Plumbers (general): 53,400). Figures marked as "unit group" cover a wider set of related occupations.

Carpenters and joiners

With 149,600 employed nationally and median weekly earnings of $1,539, carpenters and joiners are one of the largest shortage groups in the country. The shortage is classified as a retention gap. The problem is not just that too few people enter the trade, but that too many leave it. NSW accounts for 32.3% of the workforce, Victoria 29.9%, and Queensland 19.2%.

Electricians

Electricians are both the largest and highest-paid of the shortage trades, with 197,300 employed on median weekly earnings of $2,000. The shortage is classified as a suitability gap. There are applicants, but employers report that candidates frequently lack the specific experience, site readiness, or capability that roles require.

Plumbers

Plumbing is a long training gap shortage. The category applies where there are too few qualified applicants and the qualification pathway is long, typically a Certificate III or above, taking three to four years. This means even a significant lift in apprenticeship starts today will not relieve the shortage quickly. The broader plumber unit group employs 103,675 workers across all plumbing subcategories.

Bricklayers and stonemasons

Bricklaying employs around 25,464 workers nationally, smaller than carpentry or electrical, but critical to the sequence of a build. Without completed brickwork, trades that follow cannot begin work. This is classified as a suitability gap shortage, which is in shortage nationally and across all jurisdictions.

Plasterers, tilers, painters, and roofers

All finishing trades are in shortage across every state and territory. Plasterers, renderers, and wall and floor tilers are suitability gap shortages, and painters are a retention gap. Roof tilers employ around 9,400 workers nationally. That is a small enough workforce that even a modest lift in demand can create a bottleneck at the final stages of a build.

Construction managers and site supervisors

The management layer is also under pressure. Construction project managers are in shortage nationally and in all jurisdictions, with 134,300 employed and median weekly earnings of $2,928. The broader construction managers unit group is classified as a suitability gap shortage. The building associate category is not nationally short, though it is in shortage in the Northern Territory.

The three causes behind construction trade shortages

Construction labour shortages have three distinct causes, and each requires a different response. A long training gap means too few people are moving through the qualification pipeline. A suitability gap means candidates exist but lack the job-readiness employers need. A retention gap means workers are leaving faster than they can be replaced.

Long training gap: plumbers

Too few qualified applicants per vacancy, and the qualification pathway takes years. Even large increases in apprenticeship starts cannot close this gap quickly. The pipeline needs to grow and keep flowing.

Suitability gap: electricians, construction managers, plasterers, bricklayers, tilers

There may be enough nominally qualified people, but employers cannot fill roles because candidates lack the specific experience, site readiness, or job-readiness required. More supply alone does not solve a suitability gap. The match between training outcomes and employer expectations needs to improve.

Retention gap: carpenters and joiners, painters

People are entering these trades but not staying. Retention shortages are linked to working conditions, pay, culture, and access barriers. Attracting more entrants does not fix a retention problem if the conditions that drove the previous cohort out remain unchanged.

Housing construction also competes with a large public infrastructure pipeline for the same workers. An estimated $1.08 trillion of construction activity is currently underway nationally, including a $213 billion five-year public infrastructure pipeline. Housing and infrastructure are drawing from the same constrained workforce through to at least 2029.

SECTION 03 · STATE BREAKDOWN

Construction trade shortages: a state-by-state breakdown

The Northern Territory has the broadest shortage profile, with 19 of 19 tracked trades affected, followed by Western Australia at 18 of 19. NSW, Victoria, and Queensland each recorded 17 of 19 in shortage, with Tasmania and the ACT at 16 of 19.

The practical workforce gap is largest in NSW, Victoria, and Queensland, which account for 81.4% of all carpenters and joiners and 80.3% of all construction project managers nationally. The shortage is widest in NT and WA by count, but the scale of unmet demand is greatest where most new housing needs to be built.

Occupation shortage status by state and territory, 2025

Core housing trades. S = Shortage · NS = Not in shortage · R = Regional shortage only.

Filter by state or territory

Filter by trade group

| Trade | NSW | VIC | QLD | SA | WA | TAS | ACT | NT | National |

|---|---|---|---|---|---|---|---|---|---|

| Carpenter and Joiner | S | S | S | S | S | S | S | S | S |

| Carpenter | S | S | S | S | S | S | S | S | S |

| Joiner | S | S | S | S | S | S | S | S | S |

| Bricklayer | S | S | S | S | S | S | S | S | S |

| Stonemason | S | S | S | S | S | S | S | S | S |

| Painter | S | S | S | S | S | S | S | S | S |

| Plasterer | S | S | S | S | S | S | S | S | S |

| Renderer | S | S | S | S | S | S | S | S | S |

| Roof Tiler | S | S | S | S | S | S | S | S | S |

| Wall and Floor Tiler | S | S | S | S | S | S | S | S | S |

| Plumber (General) | S | S | S | S | S | S | S | S | S |

| Electrician (General) | S | S | S | S | S | S | S | S | S |

| Construction Project Manager | S | S | S | S | S | S | S | S | S |

| Project Builder | NS | NS | NS | NS | NS | S | S | NS | NS |

| Building Associate | NS | NS | NS | NS | NS | NS | NS | S | NS |

Source: Jobs and Skills Australia 2025 Occupation Shortage List, six-digit download. Project Builder (shortage in TAS and ACT only) and Building Associate (shortage in NT only) are the two occupations in this selection that are not nationally short.

SECTION 04 · BUILD TIMES

How labour shortages affect building times

When qualified tradespeople are hard to find, projects stall between stages, waiting for a framer, a plumber, an electrician, or a tiler to become available. Those delays compound across the build sequence.

Average house build times have eased to 3.07 quarters in 2024-25, down from the pandemic peak of 3.47 in 2023-24, but still about one full quarter longer than before the pandemic. Apartment build times moved in the opposite direction, reaching a record 9.58 quarters in 2024-25.

Average dwelling completion time by type, Australia

Houses and townhouses are easing from pandemic-era highs; apartment times hit a record in 2024-25. Quarters from commencement to completion, FY2014-15 to FY2024-25.

- Houses

- Townhouses

- Apartments

Methodology: Values represent average quarters from commencement to completion for each dwelling type and financial year. Month equivalents use a three-month per quarter conversion and are approximate. Source: ABS Building Activity, Average Dwelling Completion Times dataset, June 2025 release.

SECTION 05 · BUILDING COSTS

How labour shortages affect building costs

House construction input costs are 39% above their 2019 level, with the input price index at 164.3 in March 2026. Annual cost growth has eased sharply from a peak of 17.3% in mid-2022 to 2.5% by March 2026, but the industry is operating on a structurally higher cost base than before the pandemic.

Current index level

164.3

House construction input price index, March 2026

Year-on-year change

+2.5%

Annual growth rate, March quarter 2026, easing but positive

Above 2019 average

+39%

Current index vs 2019 annual average; cost base is structurally higher

Peak annual growth

+17.3%

June quarter 2022, the sharpest annual increase in the series

The worst of the cost surge has clearly passed. Annual growth in input prices peaked at 17.3% in June quarter 2022 and has eased to 2.5% by March 2026. But with the index at 164.3, input costs are still 39% above their 2019 level.

Labour shortages were one contributor to this increase, alongside materials costs, supply chain disruption, energy costs, and elevated demand. A persistent inability to staff projects at scale added to the pressure during the peak period.

Note on causation: The input price index measures prices paid for labour and materials combined. It does not isolate labour shortages as a cause. Multiple factors, including material supply chains, fuel and energy costs, global commodity prices, and strong demand, all contributed to the 2020-2022 cost surge. Labour shortages were a significant factor but not the sole driver.

Source: ABS Producer Price Indexes, Australia, Table 18: Input to the House Construction Industry, March quarter 2026.

SECTION 06 · HOUSING TARGETS

Labour demand from the 1.2 million homes target

Australia commenced 45,156 dwellings in June quarter 2025, equal to 75.3% of the 60,000-per-quarter pace required to hit the 1.2 million homes target by June 2029.

At the current rate, the five-year total would reach roughly 900,000 homes, about 300,000 short of the target. Building approvals of 17,300 in March 2026 suggest the pipeline is not yet accelerating fast enough to close that gap.

To meet combined housing and infrastructure demand, the construction labour force needs to grow by around 300,000 workers over five years, roughly 60,000 a year. At current commencement rates, that growth is not happening.

Housing accord pace: required vs actual commencements

Quarterly dwelling commencements vs target rate of 60,000 per quarter.

Target: 60,000 dwellings per quarter

National Housing Accord, 1.2 million homes by June 2029

Actual: 45,156 commencements (75.3% of target pace)

June quarter 2025, ABS Building Activity

Approvals annualised: approx. 207,600 (86.5% of target pace)

17,300 approvals in March 2026 x 12 months, ABS Building Approvals

Source: ABS Building Activity, June quarter 2025; ABS Building Approvals, March 2026; National Housing Accord target confirmed by National Cabinet, August 2023. NHSAC State of the Housing System 2026.

SECTION 07 · APPRENTICESHIPS

Construction apprenticeships: growth, gaps, and the pipeline ahead

Apprenticeship commencements are rising strongly, with 297,925 active apprentices and trainees recorded in September 2024. Growth was led by bricklayer and stonemason starts, up 40.7%, and carpenter and joiner starts, up 39.4%. But completions lag starts by three to four years, meaning today's new entrants will not ease today's shortage until 2027-28 at the earliest.

In the nine months to September 2024, there were 34,615 more commencing contracts and 8,690 more completions than in the same period of 2023. Growth was strongest in the trades under the most acute pressure:

- +40.7% Bricklayer and stonemason commencements

- +39.4% Carpenter and joiner commencements

- +24.8% Plumber commencements

- +14.9% Electrician commencements

These are meaningful increases. But completions are what actually relieve the shortage, and completions lag starts by three to four years.

Apprenticeship commencement growth by trade, nine months to September 2024

Bricklaying and carpentry recorded the strongest growth, reflecting their acute shortage status. Percentage change compared with the same nine months of 2023.

Methodology: Figures compare commencements for the nine months to 30 September 2024 with the same period of 2023. Source: NCVER Australian Vocational Education and Training Statistics: Apprentices and Trainees, September quarter 2024.

SECTION 08 · MIGRATION

Skilled migration in filling construction trade gaps

Employer-sponsored visa pathways give construction businesses a route to recruit experienced workers from overseas when domestic candidates are unavailable.

In 2024-25, 5,510 primary visa grants were made to construction industry sponsors, a 30.9% increase from 4,210 in 2023-24.

Migration is helping at the margin, particularly for experienced and specialised roles, but the scale is modest against a workforce of 1.37 million and a required growth of 300,000 over five years.

Key trades, including Carpenter, Carpenter and Joiner, Electrician (General), and Plumber (General) are on the skilled occupation list for employer-sponsored pathways, including the 482 and 186 visas. Migration is most effective at filling specific gaps where domestic pipelines are slowest to respond. It supplements domestic training and retention efforts; it cannot replace either at current volumes.

SECTION 09 · SOLUTIONS

What can help reduce construction labour shortages?

No single policy closes the gap across the whole sector because the shortage has three main causes. Effective responses differ by trade type, with plumbing needing more completions, electrical and management roles needing better training-to-work pathways, and carpentry and painting needing improved working conditions.

For long-training-gap trades: lift completions, not just starts

For plumbing specifically, more apprenticeship commencements are necessary but not sufficient. What relieves the shortage is qualified workers completing their training and staying in the industry. Employer capacity to supervise and train, apprentice support programs, and training-to-employment transitions are the key levers.

For suitability-gap trades: improve experience pathways

For electricians, construction managers, plasterers, bricklayers, and tilers, the gap between training outcomes and what employers actually need is the problem. That requires stronger training-to-work transitions, more structured site experience, better pre-qualification assessment, and clearer alignment between what training delivers and what the industry requires.

For retention-gap trades: make the work sustainable

For carpenters and painters, attracting more entrants will not fix the problem if the conditions that drove previous workers out remain unchanged. Retention shortages are linked to pay, working conditions, culture, and access barriers. More stable pipelines of work, safer and better-managed sites, and more consistent employment are the relevant remedies.

Better coordination between housing and infrastructure pipelines would reduce direct competition for the same workers. Reform of the National Construction Code and greater use of modern construction methods would reduce pressure on scarce trades more broadly. Housing and major public infrastructure are in direct competition for the same workers through to at least 2029.

SECTION 10 · BUYER IMPACTS

What construction labour shortages mean for homebuyers

With input costs still 39% above 2019 levels and average house build times more than 40% longer than before the pandemic, labour shortages now have direct practical effects for anyone building or buying a new home, from longer wait times and higher costs to greater contract and financing risk.

Builds may take longer

When trades are hard to schedule, projects stall between stages. Average house times are still about one full quarter longer than before the pandemic.

Labour costs are elevated

Input costs are 39% above their 2019 level. Quotes may carry higher labour and subcontractor rates than a few years ago, particularly for electrical, plumbing, and finishing trades.

Fixed-price contracts carry more risk

In a tight labour market, builders may have less flexibility to absorb cost overruns in fixed-price contracts. Some have included rise-and-fall clauses or price review mechanisms.

Delays affect loan timing and planning

Construction loans often have staged drawdown schedules tied to build milestones. Delays can affect interest periods, rental overlap costs, and moving plans if the handover timeline shifts significantly.

Apartments are affected differently

Apartment build times hit 9.58 quarters in 2024-25, a record, and have not yet started to ease. Buyers in the off-the-plan market face more timeline uncertainty than buyers of detached houses.

Builder selection matters more

A builder's relationships with subcontractors can affect scheduling reliability. A builder with strong trade relationships is more likely to maintain consistent site access and build pace.

General information only This article is based on publicly available data from ABS, Jobs and Skills Australia, NCVER, and other official sources. It does not constitute financial, legal, or construction advice. If you are making decisions about building, contracting, or investment, consider speaking with a licensed builder, financial adviser, or other relevant professional.

ABS Labour Force, Australia, Detailed, Table 04, February 2026

ABS Job Vacancies, Australia, Table 4, February 2026

Jobs and Skills Australia 2025 Occupation Shortage List, 2025. Six-digit shortage ratings by occupation and jurisdiction.

ABS Building Activity, Australia, June quarter 2025

ABS Producer Price Indexes, Australia, Table 18, March quarter 2026

NCVER Apprentices and Trainees, September quarter 2024

Department of Home Affairs: Temporary Resident (Skilled) Report, 30 June 2025

NHSAC State of the Housing System, 2026

Infrastructure Australia 2025 Market Capacity Report, 2025

ABS Building Approvals, Australia, March 2026

Chart Snapshots