Why is Australia falling short of its housing target?

Australia is behind the pace needed to meet its 1.2 million-home target. By March 2026, 219,000 homes had been completed, equal to about 18% of the National Housing Accord goal. To reach the target by June 2029, the country would now need to deliver about 261,600 homes a year, a pace it has not previously reached.

The shortfall reflects several constraints across the housing pipeline. Approvals remain below the required pace, construction labour is stretched, material costs are still rising, and homes are taking longer to build than before the pandemic.

Accord target

1.2M

New homes by 30 June 2029

Annual pace required

240,000

Completions every year, July 2024 to June 2029

Actual completions FY2024–25

174,981

27.1% below the required annual pace

Annual shortfall (FY2024–25)

65,019

Homes below the 240,000 target pace

How many homes does Australia need to build each year to meet the target?

The target of 1.2 million homes over five years requires 240,000 completions per year. That pace was already demanding before a single home was built. The highest annual completion figure on record is FY2016–17 at 224,490 dwellings, still short of what the Accord requires every year.

The Accord originally required 240,000 completions a year, or about 20,000 homes a month, from July 2024 to June 2029. Because the first five quarters fell short, Australia now needs closer to 261,600 completions a year to catch up.

The task has grown harder since the Accord began. The March 2026 quarterly progress report recorded 219,000 completions across the first five quarters, leaving roughly 981,000 homes still needed over the remaining 15 quarters to June 2029.

That implies a required rate of 65,400 completions a quarter, or 261,600 a year, about 9% above the straight-line pace.

| Measure | Value | Note |

|---|---|---|

| National Housing Accord target | 1,200,000 | Gross completions, 1 July 2024 to 30 June 2029 |

| Straight-line annual pace | 240,000/yr | 1.2M divided by 5 years |

| Straight-line quarterly pace | 60,000/qtr | 1.2M divided by 20 quarters |

| Homes completed (first 5 quarters) | 219,000 | NHSAC March 2026 quarterly report |

| Homes still needed by June 2029 | 981,000 | 1.2M minus 219,000 |

| Required catch-up pace | 65,400/qtr | 981,000 divided by 15 remaining quarters |

| Required annualised catch-up pace | 261,600/yr | 65,400 multiplied by 4 |

Methodology: Catch-up pace calculated by dividing remaining target (1.2M minus 219,000) by the 15 quarters remaining to June 2029. Source: Treasury housing pages, May 2026; NHSAC Quarterly Report, March 2026.

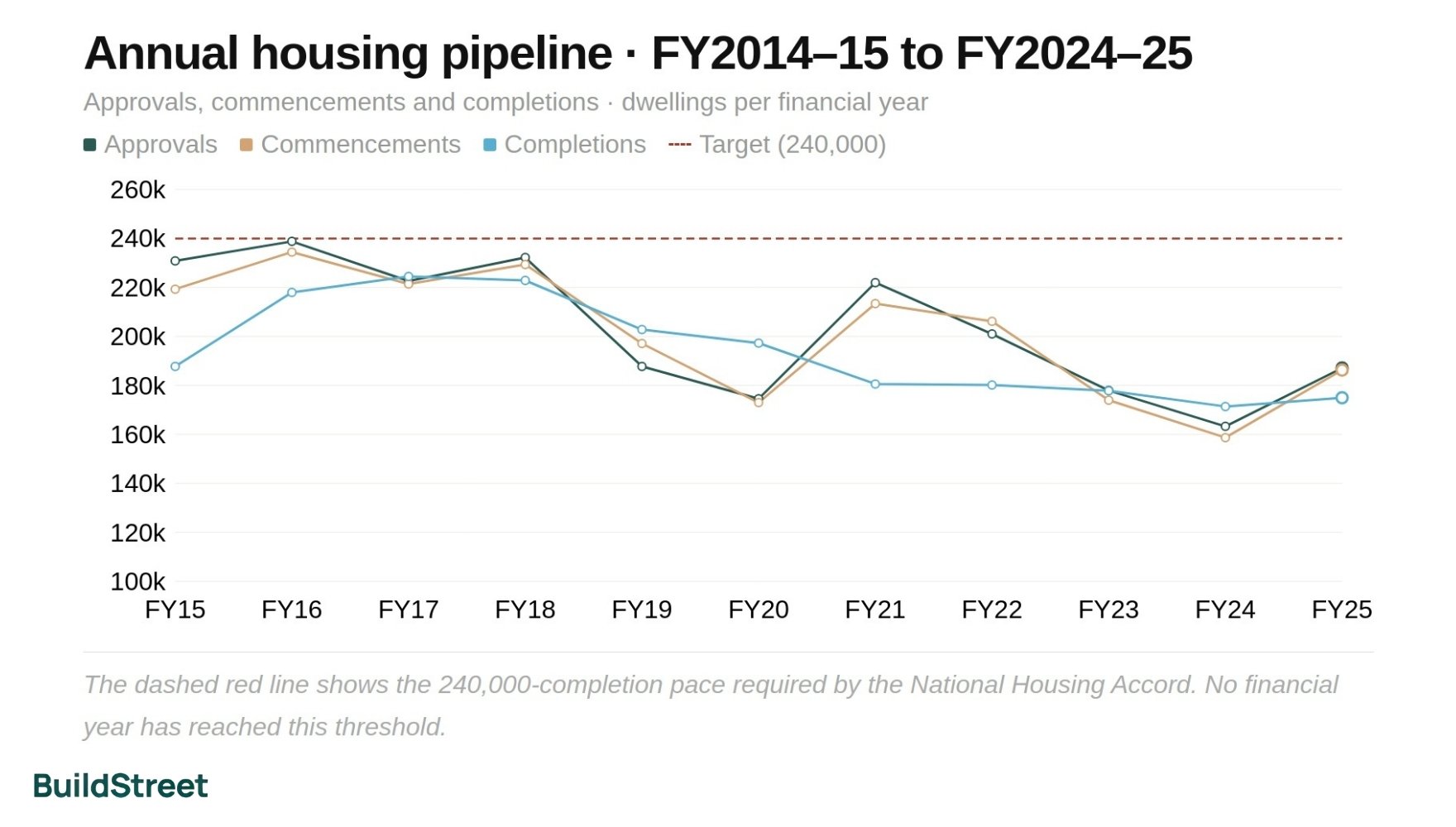

Housing completions: Australia remains well below the required pace

Australia completed 174,981 dwellings in FY2024–25, up just 2.1% from 171,402 the previous year.

Approvals increased by 14.6% to 187,084, and commencements rose 17.4% to 186,261, but completions are the only measure that counts toward the Accord target, and they barely moved.

The year-by-year data on Australian building approvals shows that completions have consistently fallen well short of the 240,000 annual pace in every year on record.

The gap between actual completions and the required pace has remained wide and consistent. The recent upturn in approvals and commencements is a positive signal, but it has not yet translated into higher completion numbers.

Annual housing pipeline: approvals, commencements and completions, FY2014–15 to FY2024–25

The dashed red line shows the 240,000-completion pace required by the National Housing Accord. No financial year has reached this threshold.

Methodology: Annual financial-year totals from ABS Building Approvals and Building Activity workbooks. Source: ABS Building Approvals (Cat. 8731.0); ABS Building Activity (Cat. 8752.0), FY2024–25.

In the December 2025 quarter, commencements reached 53,567 while completions were only 43,536. Dwellings under construction climbed to 236,858, up from 212,616 a year earlier, suggesting projects are entering the system faster than they are being finished.

Is Australia on track to build 1.2 million homes by 2029?

NHSAC 2025 forecast

938,000

78% of target; shortfall of 262,000 homes

NHSAC 2026 forecast

980,000

82% of target; improved but still 220,000 short

Expected national completion

Sep 2030

15 months past the June 2029 Accord deadline

Dec qtr 2025 completions

43,536

33.4% below the 65,400 catch-up quarterly rate now needed

Even that improved outlook still leaves a 220,000-home shortfall against the Accord target. There is also a downside risk, with modelled scenarios involving higher fuel and petrochemical costs potentially reducing completions by 10,000 to 33,000 homes before mid-2029.

Seasonally adjusted approvals for January to March 2026 totalled 50,886 dwellings, annualising to roughly 203,544 for the year, below both target paces. Detailed state-level progress and scenario forecasts are in the National Housing Accord progress tracker.

Why is housing construction falling behind?

Construction is not falling short because of a single problem. A chain of linked constraints spans the entire building pipeline, from the approvals system through to the labour market, financing conditions, build times and the planning framework that determines what gets built and where.

01

Approvals still below pace

187,084

FY2024–25 approvals, 52,916 below the 240,000 annual target pace.

02

Longer build times

33 months

Average apartment completion time in FY2024–25, up from under 21 months in FY2014–15.

03

Labour shortages

21,600

Construction vacancies in February 2026, up from 16,600 before the pandemic.

04

Material costs still rising

+4.2%

Building construction output price, year-on-year to March 2026.

05

Tight financing

7.03%

Small business outstanding lending rate, February 2026.

06

Builder insolvencies

+33.2%

Rise in first-time company external administrations, FY2024–25 vs FY2023–24.

07

Apartment recovery too slow

44.5%

Higher-density share of Dec 2025 commencements, but annual approvals still below mid-2010s peak.

08

Land and planning barriers

$1.5B

Commonwealth Housing Support Program funding to unlock enabling infrastructure for new supply.

1. Building approvals are not high enough

Approvals are the earliest large-scale pipeline signal, and they remain below target. FY2024–25 approvals of 187,084 were 52,916 below the 240,000 annual Accord pace.

Monthly approvals in early 2026 have been volatile and consistently below the 20,000-per-month threshold the Accord requires:

- January 2026: 14,564 approvals

- February 2026: 19,022 approvals

- March 2026: 17,300 approvals

An approvals flow below target now will translate into a completions flow below target in 12 to 33 months, depending on dwelling type.

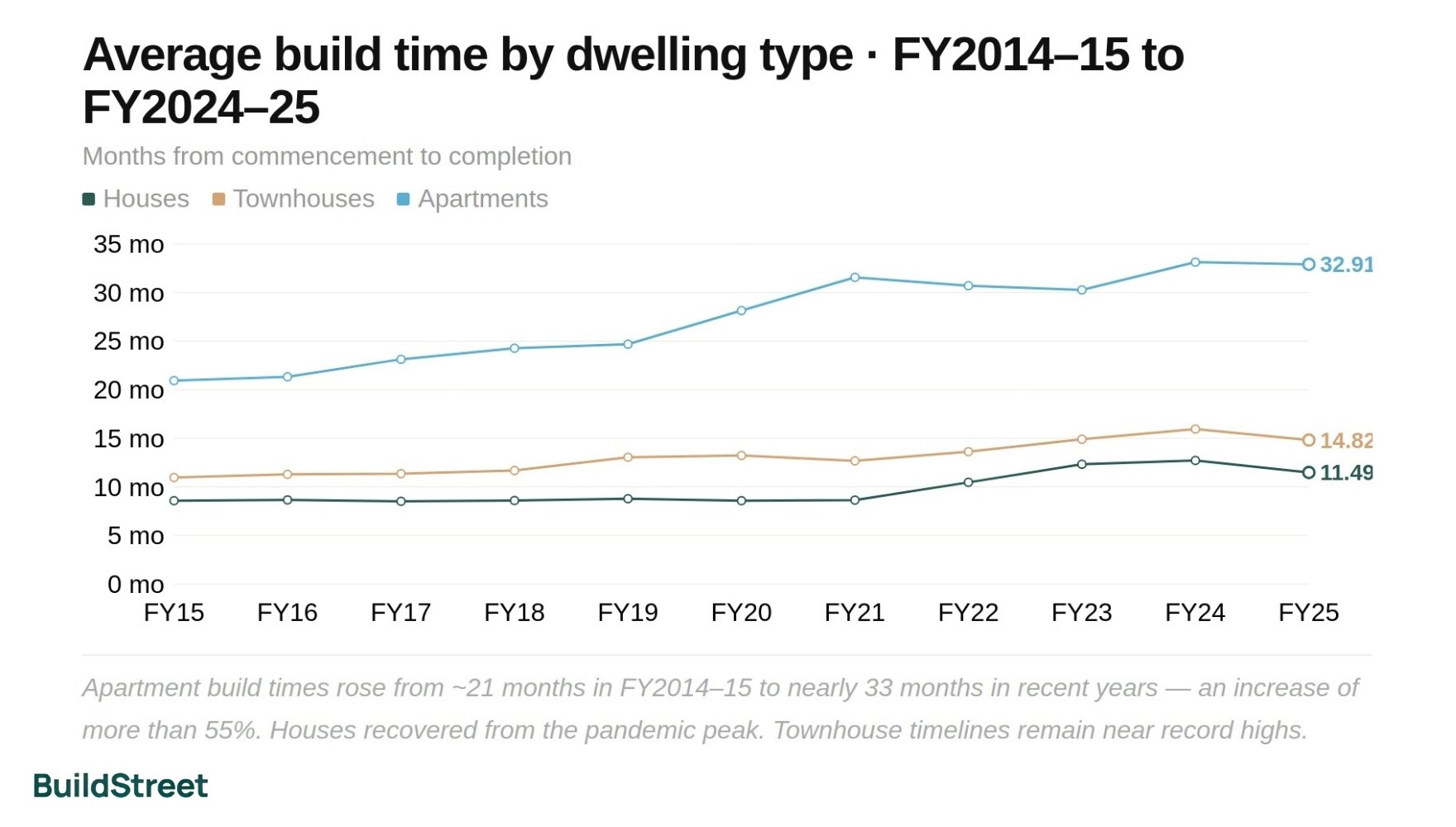

2. Homes are taking longer to build

The average house took 11.5 months from commencement to completion in FY2024–25, an improvement from the pandemic-era peak of 12.72 months. Townhouses still averaged around 15 months and apartments around 33 months, compared with roughly 9 months for a new house in 2019-20.

Longer build times reduce the number of completions any given approvals flow can produce. They also extend the period over which financing costs accumulate before projects generate revenue.

Average build time by dwelling type (months, commencement to completion), FY2014–15 to FY2024–25

Apartment build times have risen from around 21 months in FY2014–15 to nearly 33 months in recent years, an increase of more than 55%. Houses have recovered from the pandemic peak. Townhouse timelines remain near record highs.

Methodology: Build time is the average period between commencement and completion. Source: NHSAC State of the Housing System 2024 and 2026; ABS Building Activity (Cat. 8752.0).

3. Labour shortages are slowing construction

There were 21,600 construction vacancies in February 2026, up from 18,500 in February 2025 and from 16,600 before the pandemic in February 2020, a 30% rise over that period.

Nearly half of all trade roles remain in shortage, with construction particularly affected. These pressures have eased from their pandemic-era peak but remain a supply constraint.

4. Building material costs remain high

Building construction output prices rose 4.2% in the year to March 2026, and new dwelling prices in the consumer price index were up 4.5% over the same period.

Cost inflation has slowed sharply from the double-digit surges of 2021–22, but the industry is still building in a materially more expensive environment than before the pandemic.

| Cost measure | Year-on-year change to March 2026 |

|---|---|

| Input prices for house construction | +2.5% |

| Output price of building construction | +4.2% |

| House construction output price | +4.1% |

| Other residential building construction | +4.2% |

| CPI: new dwelling prices | +4.5% |

Source: ABS Producer Price Indexes (Cat. 6427.0), March quarter 2026; ABS Consumer Price Index (Cat. 6401.0), March quarter 2026.

5. Higher interest rates made projects harder to finance

The cash rate target was 4.35% as of May 2026. Small-business lending rates were also elevated, sitting at 7.03% on outstanding loans and 6.91% on new loans as of February 2026.

This matters because residential projects are expensive to fund upfront. Financing costs build up throughout construction, often before any revenue comes in. Higher rates make some projects harder to justify, even though borrowing conditions eased slightly through 2025.

6. Builder insolvencies reduced industry capacity

The number of companies entering external administration for the first time reached 14,722 in FY2024–25, up 33.2% from 11,053 in FY2023–24. Construction was the largest insolvency sector by volume in FY2023–24, accounting for 2,975 companies or 27% of all first-time administrations.

Each insolvency removes completed projects, partly-built homes and experienced workers from the pipeline, while raising risk premiums across the sector for those that remain.

7. Apartment construction has not recovered enough

Higher-density dwellings accounted for 44.5% of all new commencements in the December 2025 quarter, with 23,849 commencements out of 53,567. However, annual apartment approvals remain well below the mid-2010s peak.

Given that apartments take around 33 months to move from commencement to completion, a sustained recovery in approvals needs to begin now for those projects to count toward the June 2029 deadline. If apartment supply does not recover materially, detached housing cannot carry the Accord target on its own.

8. Land release and infrastructure are slowing new supply

Australia's housing package includes a National Planning Reform Blueprint covering planning, zoning, land release and approval pathways, with a specific emphasis on medium- and high-density housing in well-located areas.

A separate $1.5 billion Housing Support Program funds enabling infrastructure, community amenity and planning capacity to help meet the Accord target. Reviews of the housing system have consistently called on governments to improve planning systems and increase the supply of developable, serviced land.

The inclusion of dedicated funding and intergovernmental coordination suggests these issues are recognised as significant constraints on new housing supply, rather than peripheral concerns.

Which states are furthest behind on housing supply?

New South Wales has the biggest gap to close in raw numbers. Just 15% of its 376,000-home target has been built, and it won't be done until June 2031.

In proportional terms, the Northern Territory and Tasmania are even further off the pace.

- Northern Territory: 5% built, projected past 2034

- Tasmania: 12% built, projected September 2033

- New South Wales: 15% built, projected June 2031

The ACT and Western Australia are the only jurisdictions predicted to meet or exceed their implied target shares.

State-by-state housing progress: 2026 forecast and completions to date

NHSAC analytical allocations based on each jurisdiction's December 2022 population share. Green = on or near target; amber = moderate shortfall; red = significant shortfall.

NHSAC early-2026 no-conflict outlook: forecast gross completions as a share of each state's Accord allocation by June 2029.

Methodology: State target allocations are NHSAC's analytical apportionment based on each jurisdiction's December 2022 population share. These are analytical benchmarks, not formal intergovernmental quotas. Source: NHSAC Quarterly Report, March 2026; NHSAC State of the Housing System 2026.

| State / territory | Implied target | Built to date | Approved to date | 2026 forecast | Expected completion |

|---|---|---|---|---|---|

| New South Wales | 376,000 | 15% | 21% | 69% | Jun 2031 |

| Victoria | 306,000 | 23% | 28% | 94% | Sep 2029 |

| Queensland | 246,000 | 17% | 26% | 83% | Sep 2030 |

| Western Australia | 129,000 | 22% | 29% | 100% | Sep 2029 |

| South Australia | 84,000 | 19% | 27% | 78% | Sep 2030 |

| Tasmania | 26,000 | 12% | 15% | 51% | Sep 2033 |

| Australian Capital Territory | 21,000 | 23% | 25% | 103% | Sep 2029 |

| Northern Territory | 11,000 | 5% | 9% | 34% | After 2034 |

| Australia (national) | 1,200,000 | 18% | 25% | 82% | Sep 2030 |

Apartments are critical to meeting the housing target

Apartments matter because the target cannot be met through detached housing alone.

Higher-density dwellings accounted for 44.5% of all new commencements in the December 2025 quarter, with 23,849 of 53,567 new homes falling into this category. Detached houses alone cannot deliver the volumes the Accord requires, and if the higher-density share is not sustained and increased, the national pipeline will remain structurally short regardless of what happens in the detached segment.

The planning blueprint explicitly targets medium- and high-density housing in well-located areas close to transport, amenities and jobs. The states that need to deliver the most volume, particularly NSW and Victoria, depend heavily on the apartment and townhouse pipeline near established infrastructure. These are also the areas where new land for detached housing is limited, unavailable or impractical.

Higher-density commencements (Dec qtr 2025)

23,849

44.5% of all commencements that quarter

Average apartment build time

33 months

vs 11.5 months for a new house in FY2024–25

Higher-density approvals (March 2026, seas. adj.)

6,632

Monthly figure: volatile and still below what the target needs

The housing shortfall is increasing pressure on buyers and renters

The national mean dwelling price reached $1,074,700 in the December 2025 quarter. NSW recorded the highest state mean at $1,301,100, which was 21% above the national figure and more than $235,000 higher than Queensland, the next most expensive state.

These are mean dwelling values across all residential property, not median sale prices, but they reflect the price environment buyers face in a market where new supply has consistently fallen short of demand.

Mean residential dwelling price by state, December quarter 2025

National mean: $1,074,700. NSW is 21% above the national figure. Victoria and South Australia recorded the lowest state means at just over $930,000.

Methodology: Mean dwelling price = total estimated value of all residential dwellings / number of dwellings. Not equivalent to median sale price. Source: ABS Total Value of Dwellings (Cat. 6432.0), December quarter 2025.

For renters, conditions have improved from their worst point but remain under strain. Rents rose 3.7% over the year to March 2026, driven by low vacancy rates across capital cities.

Around 1.4 million income units received Commonwealth Rent Assistance in the September 2025 quarter. Of those, approximately 590,000 remained in rental stress even after receiving support, still spending more than 30% of gross income on rent.

National mean dwelling price

$1,074,700

December quarter 2025

NSW mean dwelling price

$1,301,100

Highest state mean, December 2025

Rent inflation

+3.7%

Year-on-year to March 2026; driven by low vacancy rates

CRA recipients

1.4M

Income units receiving Commonwealth Rent Assistance, Sep qtr 2025

In rental stress after CRA

590,000

Income units spending more than 30% of gross income on rent despite receiving CRA

Public housing waitlist

169,000

Households on public housing waitlists at 30 June 2024

Source: ABS Total Value of Dwellings (Cat. 6432.0), December quarter 2025; ABS Consumer Price Index (Cat. 6401.0), March quarter 2026; AIHW Housing Assistance in Australia, September quarter 2025.

The path to 1.2 million homes: what would need to change

Australia is not on track to deliver 1.2 million homes by June 2029 on current production settings, but the outlook has improved.

The most recent forecast points to around 980,000 completions by the Accord deadline, with the full target not expected to be met until around September 2030.

The 2026 forecast is stronger than the previous year's outlook, lifting the projected five-year total from 938,000 to 980,000 homes. This is equal to 82% of the target. The updated no-conflict estimate puts the national completion date at September 2030, more than 15 months after the Accord deadline.

Even that improved outlook still leaves a 220,000-home shortfall against the Accord target. There is also a downside risk: modelled scenarios involving higher fuel and petrochemical costs could reduce completions by 10,000 to 33,000 homes before mid-2029, which could push the total below 82% of the target without corrective action.

| Scenario | Projected homes | % of target | Expected date to reach 1.2M |

|---|---|---|---|

| NHSAC 2025 forecast | 938,000 | 78% | Not modelled |

| NHSAC 2026 no-conflict forecast | 980,000 | 82% | Around September 2030 |

| NHSAC 2026 downside (fuel and petrochemical cost shock) | 947,000–970,000 | 79–81% | Later than September 2030 |

| Accord target | 1,200,000 | Not on current track | June 2029 |

Methodology: Downside scenario estimated by subtracting NHSAC's modelled range of 10,000–33,000 fewer completions from the 980,000 no-conflict forecast. Source: NHSAC State of the Housing System 2025 and 2026.

General information only

This article draws on publicly available data from the ABS, NHSAC, Treasury, RBA, ASIC and AIHW. It is general information only and does not constitute financial or investment advice.

ABS Building Approvals, Australia, March 2026

ABS Building Activity, Australia, December Quarter 2025

ABS Total Value of Dwellings, December Quarter 2025

ABS Producer Price Indexes, March Quarter 2026

ABS Consumer Price Index, March Quarter 2026

ABS Job Vacancies, Australia, February 2026

NHSAC Quarterly Report, March 2026

NHSAC State of the Housing System, 2026

NHSAC State of the Housing System, 2025

Treasury — Increasing housing supply, accessed May 2026

RBA Cash Rate Target and Lending Rates, May 2026 and February 2026

ASIC Insolvency Statistics, FY2024–25, FY2023–24

AIHW Housing Assistance in Australia, June 2025

Jobs and Skills Australia — Occupation Shortage List 2025

Chart Snapshots