WA housing statistics: Perth population growth is outpacing new construction

Western Australia completed 22,736 homes in 2024–25. That was about 88 per cent of the 25,800 homes a year needed to meet its 129,000-home National Housing Accord target by June 2029.

WA is projected to reach that target by September 2029, one quarter after the deadline. That puts it alongside Victoria as one of the strongest-performing states.

At state level, the forecast looks solid. But Perth tells a more pressured story. Greater Perth added 58,088 residents in 2024–25, the fastest growth rate of any capital city. At the same time, it approved only 335 new dwellings per 1,000 new residents, the lowest rate among the four largest capitals.

WA Accord target (to Jun 2029)

129,000

Population-share allocation; requires 25,800 homes a year

FY2024–25 completions

22,736

88% of required pace; best result since 2016–17

Greater Perth: approvals per 1,000 new residents

335

Lowest of the four largest capitals: Sydney 446, Melbourne 443

Australia has completed about 18% of its national Accord target. WA and Victoria are the two states currently projected to deliver their share by or very close to the deadline. Read full article →

WA houses took an average of 5.15 quarters from approval to completion in 2024–25, the longest of any state or territory, and up from 3.02 quarters in 2019–20. Read full article →

SECTION 01 · THE HOUSING TARGET

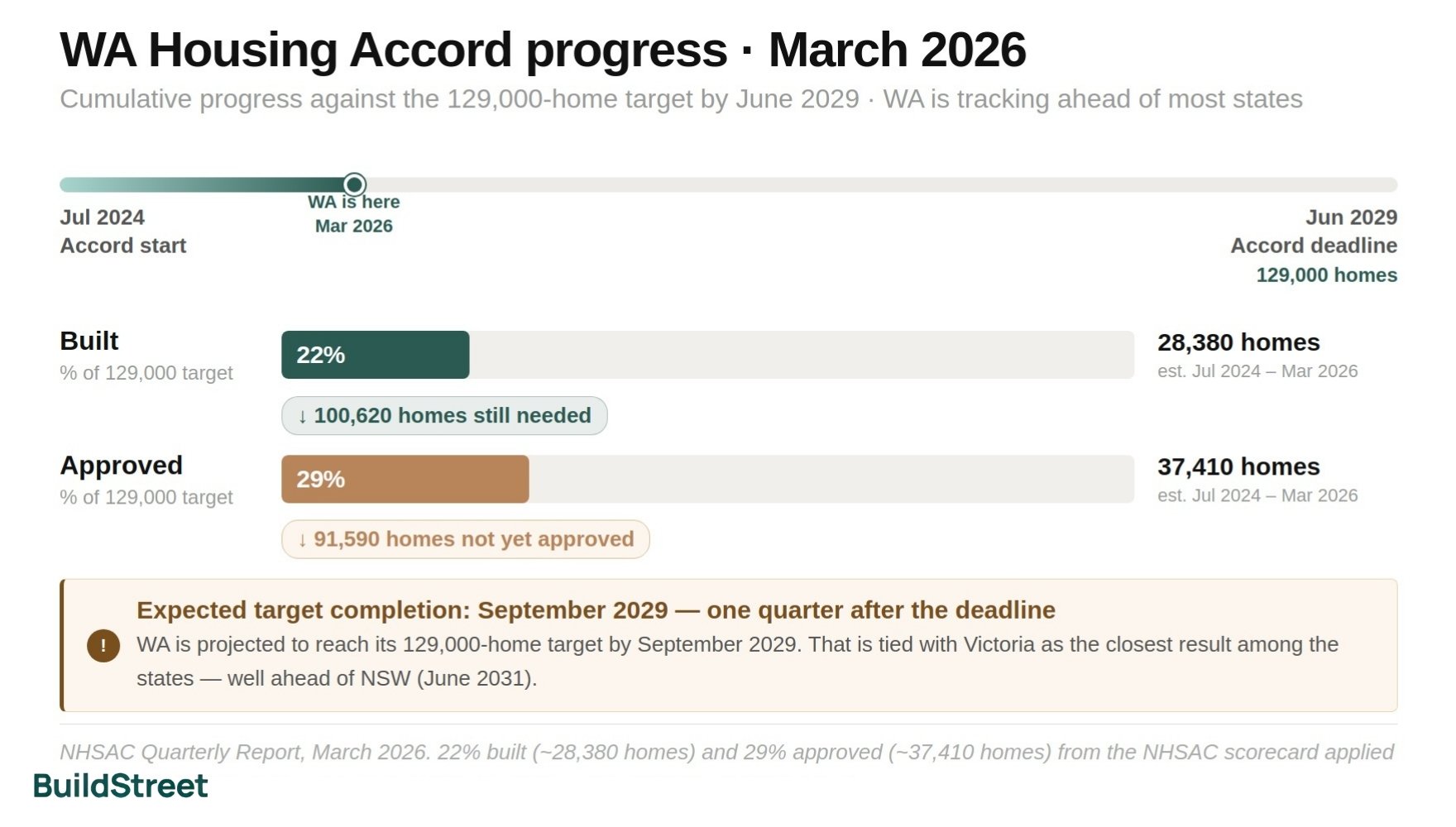

WA's 129,000-home target: how much has been built?

WA completed 22,736 dwellings in 2024–25, the state's best annual result since 2016–17. That was equal to 88 per cent of the annual pace needed to meet its National Housing Accord target.

WA is expected to reach its 129,000-home target by September 2029, one quarter after the June 2029 deadline. Among the states, only Victoria is forecast to finish as close to the deadline.

The National Housing Accord aims to deliver 1.2 million new homes across Australia between July 2024 and June 2029. WA's share is 129,000 homes, based on its population share when the Accord was agreed in 2022. That means the state needs to build about 25,800 homes a year.

As at March 2026, WA had built 22 per cent of its target, or about 28,380 homes. That leaves around 100,620 homes still to be completed.

WA had also approved 29 per cent of its target, or about 37,410 homes. That leaves around 91,590 homes not yet approved.

Current forecasts estimate WA will reach about 129,000 gross new homes by September 2029, one quarter after the Accord deadline.

WA Housing Accord progress

Cumulative progress against the target of 129,000 homes by June 2029, as at March 2026.

Mar 2026

Accord startJun 2029

Accord deadline

% of 129,000

% of 129,000

Expected target completion: September 2029

WA is projected to reach its 129,000-home target by September 2029, one quarter after the National Housing Accord deadline. That is tied with Victoria as the closest result among the states. Current forecasts estimate WA will deliver about 129,000 gross new homes over the five Accord years. That would match its target share and sit well above the 75,000 homes built in the previous five years.

WA's 129,000-home target is based on NHSAC's population-share method: 1,076 ÷ 9,962 × 1,200,000, using December 2022 population shares. The 22% built and 29% approved figures come from the NHSAC March 2026 scorecard. They reflect Accord progress from July 2024 to March 2026, using completions data to September 2025 and approvals data to January 2026. That equals about 28,380 homes built and 37,410 homes approved. WA still needs about 100,620 completions, with about 91,590 homes not yet approved. Sources: NHSAC Quarterly Report, March 2026; NHSAC State of the Housing System 2025.

How WA compares to other states

WA has built 22% of its National Housing Accord target so far, the second-highest share among the larger states behind Victoria at 23%.

The bigger difference is the expected completion date. WA and Victoria are both projected to reach their targets by September 2029, one quarter after the June 2029 deadline. NSW is projected to miss the deadline by about two years, while the Northern Territory is projected to miss it by more than five years.

| State / Territory | Target (homes) | % built | % approved | Expected delivery |

|---|---|---|---|---|

| Western Australia | 129,000 | 22% | 29% | Sep 2029 |

| Victoria | 306,000 | 23% | 28% | Sep 2029 |

| Queensland | 246,000 | 17% | 26% | Sep 2030 |

| New South Wales | 376,000 | 15% | 21% | Jun 2031 |

| South Australia | 84,000 | 19% | 27% | Sep 2030 |

| Tasmania | 26,000 | 12% | 15% | Sep 2033 |

| Australia (total) | 1,200,000 | 18% | 25% | Jun 2030 |

Methodology: Target homes for each jurisdiction are derived from NHSAC's published population-share allocation (1076 ÷ 9,962 of the 1.2 million national total for WA, with equivalent ratios for other states). "Built" and "approved" shares are NHSAC's cumulative percentages from the March 2026 scorecard. "Expected delivery" reflects NHSAC's modelled date when each jurisdiction's share is forecast to be met. Source: NHSAC Quarterly Report, March 2026.

SECTION 02 · STATE COMPARISON

Population growth vs new homes: Perth is under more pressure than WA overall

Greater Perth approved just 335 dwellings per 1,000 new residents in 2024–25. That was the lowest rate among Australia's four largest capitals, even though Perth had the fastest population growth of any capital city at 2.4%.

At the state level, WA added 66,235 residents and completed 22,736 dwellings in 2024–25. That works out to 343 dwellings per 1,000 new residents, almost the same as Queensland at 345, but below Victoria at 455 and NSW at 424.

At the capital-city level, Greater Perth's 335 approvals per 1,000 new residents compares with 371 in Greater Brisbane, 443 in Greater Melbourne and 446 in Greater Sydney.

| Capital city | Population growth 2024–25 | Housing flow FY2024–25 (approvals) | Homes per 1,000 residents added | Residents added per home |

|---|---|---|---|---|

| Greater Perth | +58,088 | 19,458 | 335 | 2.99 |

| Greater Brisbane | +58,223 | 21,588 | 371 | 2.70 |

| Greater Melbourne | +105,030 | 46,530 | 443 | 2.26 |

| Greater Sydney | +75,230 | 33,573 | 446 | 2.24 |

Methodology: Capital-city rows compare ABS Regional Population growth in 2024–25 with FY2024–25 original GCCSA dwelling approvals. State-level rows compare 30 June 2024 to 30 June 2025 population change with FY2024–25 original dwelling completions. Capitals use approvals because completions are not separately published at the GCCSA level. Source: ABS Regional Population 2024–25; ABS Building Approvals (cat. 8731.0) Tables 10 and 26; ABS Building Activity (cat. 8752.0) Table 39.

SECTION 03 · APPROVALS

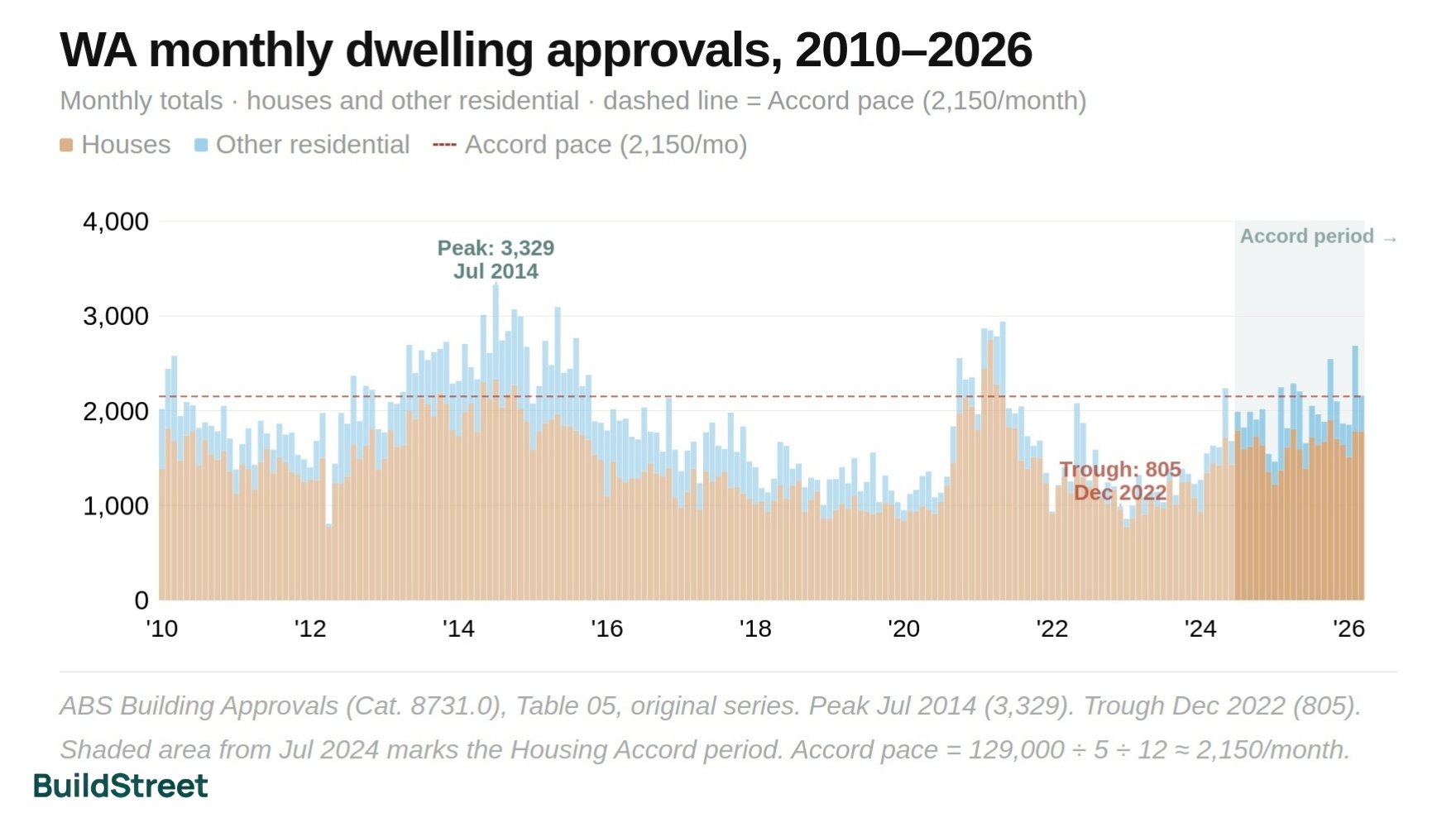

WA housing approvals remain below historical peaks

WA approved 22,945 dwellings in 2024–25, up 31.4% from 17,465 the previous year. In the 12 months to March 2026, WA approved 25,247 dwellings. That was equal to about 97.9% of the 25,800 homes a year needed to meet its Accord pace.

It was also the highest 12-month total since late 2021. However, approvals remain below WA's modern peak of 33,088 dwellings in calendar 2014 during the mining boom. They also remain below the HomeBuilder stimulus peak of 25,843 in 2021.

The current 12-month total is 23.7% below the 2014 peak. Monthly figures are still volatile. In March 2026, WA recorded 2,158 approvals, down 19.6% from the previous month.

WA monthly dwelling approvals, January 2010 to March 2026

Approvals have recovered from the 2022–23 trough but remain below the 2014 mining-boom peak and the 2021 HomeBuilder spike.

Methodology: Monthly and financial-year charts use ABS Building Approvals Table 05 (WA total, original series). Dwelling-type chart uses Table 26 (calendar years, original series). Accord pace = 129,000 ÷ 5 years = 25,800/yr or approximately 2,150/month. Source: ABS Building Approvals, Australia, March 2026 release.

SECTION 04 · WHAT IS ACTUALLY BEING BUILT

How many homes is WA completing each year?

WA completed 22,736 dwellings in 2024–25, the highest annual result since 2016–17 and up 67% from the low point of 13,654 in 2020–21.

Approvals (22,945), commencements (22,533) and completions (22,736) were all within a few hundred dwellings of each other for the first time in years. This suggests much of the post-HomeBuilder backlog has cleared.

WA is still below the Accord benchmark of 25,800 completions a year. The 2024–25 result was 3,064 homes short of that pace. However, quarterly completions have remained above 4,600 since mid-2024, and the gap has started to narrow.

What 22,736 completions a year looks like

WA dwelling approvals, commencements and completions, FY2010–11 to FY2024–25

All three pipeline series converged near 22,500 in 2024–25, the first time they have aligned since the post-HomeBuilder period.

Methodology: Annual view shows financial-year totals (July to June). Approvals from ABS Building Approvals (cat. 8731.0) Table 05, original series. Commencements and completions from ABS Building Activity (cat. 8752.0) Tables 35 and 39, original series. The quarterly view shows original-series WA completions split between detached houses and other residential dwellings, from Q1 2015 to Q4 2025. Source: ABS Building Approvals March 2026; ABS Building Activity December 2025.

SECTION 05 · CONSTRUCTION PIPELINE

Perth land approvals are rising, but build times are slowing delivery

WA had 25,458 dwellings under construction at 31 December 2025, but only 4,626 were completed in that quarter. At that pace, it would take about 16.5 months to work through everything currently under construction. Build times appear to be a key bottleneck.

WA houses took an average of 5.15 quarters from approval to completion in 2024–25, the longest of any state or territory. While that improved from 5.95 quarters in 2023–24, it is still 70% longer than the 3.02 quarters recorded in 2019–20. For comparison, NSW recorded 4.10 quarters, South Australia 4.57, and the ACT 4.33. Victoria, Queensland and the NT all completed a house in roughly three quarters or less.

A further 3,517 dwellings had been approved but not yet started as at December 2025. Apartment and townhouse projects are moving through the pipeline more slowly, with many still under construction and relatively few reaching completion each quarter.

Average house build times by state, 2019–20 vs 2024–25

Build times have lengthened in every state, but WA recorded the largest increase and is now the slowest. Queensland and the NT remain the fastest.

Methodology: Total time equals "approval to commencement" plus "commencement to completion", measured in quarters. Source: ABS Building Activity (cat. 8752.0), aggregated from Tables 34 and 39.

The land pipeline behind Perth's approvals

WA developers received conditional approval for 7,099 residential lots in the December 2025 quarter, up 17% on the previous quarter. That lifted the total conditional approval stock to 60,052 lots.

Final lot approvals reached 4,506 in the same quarter, up 33% from September. About 94.7% of all final residential lot approvals were in the Perth metropolitan area.

The lot pipeline is growing, but mostly on Perth's outer fringe. New land releases in greenfield areas usually produce detached houses, so this concentration makes it harder to increase townhouse and apartment supply.

Dec 2025 quarter

End Dec 2025

Dec 2025 quarter

Dec 2025 quarter

SECTION 06 · HOUSING MIX

Detached houses dominate WA's new home market

Detached houses made up 79.7% of WA's new residential approvals in the 12 months to March 2026, compared with 58.6% nationally. Apartments accounted for just 11.7% of approvals, roughly half the national share of 23.8%. Townhouses and semis were 8.6%, also about half the national rate of 17.6%.

Within Greater Perth, the skew towards detached houses is even more pronounced. Apartments and townhouses made up just 20.4% of approvals in 2024–25, compared with 37.0% in Greater Brisbane, 48.2% in Greater Melbourne and 61.3% in Greater Sydney.

Source: ABS Building Approvals, Australia, March 2026 release, Table 26. Series are "Houses", "Semi-detached, row or terrace houses, townhouses (Total)" and "Apartments (Total including those attached to a house)". Original monthly approvals summed over 12 months to March 2026.

Where are Perth's new housing lots being approved?

Most new lot supply is concentrated in Perth's outer growth corridors. In the December 2025 quarter, Baldivis alone accounted for 456 of WA's 4,506 final residential lot approvals.

The top five metro suburbs, Baldivis, Eglinton, Alkimos, Lakelands and Hilbert, accounted for 1,340 lots combined. The top 10 suburbs accounted for 1,909 lots, or about 42% of all final lot approvals across WA.

In regional WA, approvals were concentrated mainly around Margaret River in the South West.

Top metro suburbs by final lot approvals

Top regional WA suburbs

Methodology: Number of residential lots receiving final approval during the December 2025 quarter. Final approval is the last stage of subdivision before lots can be registered. Source: WA Department of Planning, Lands and Heritage, State Lot Activity, December quarter 2025.

SECTION 07 · APARTMENT & TOWNHOUSE SUPPLY

Apartment and townhouse supply in Perth remains below the national average

Apartments and townhouses made up just 20.4% of Greater Perth's residential approvals in 2024–25. This was the lowest share of any major Australian capital. Greater Brisbane had the next lowest share at 37.0%, while Greater Melbourne recorded 48.2% and Greater Sydney 61.3%.

The gap is clearest in apartments. In WA, apartments accounted for 11.7% of new residential approvals in the 12 months to March 2026, compared with the national share of 23.8%.

This suggests Perth's supply mix is still heavily weighted towards detached housing. It does not necessarily point to weak demand for apartments or townhouses. Greater Perth grew faster than any other capital in 2024–25, and demand is likely to be spread across different types of housing.

Non-house share of residential approvals by capital city, FY2024–25

Greater Perth has the lowest medium and high-density approval share of the four largest capitals, despite the fastest population growth rate. The gap to Greater Sydney is more than 40 percentage points.

Methodology: "Non-house" equals dwellings excluding houses (townhouses, semis, apartments). Calculated as a share of total dwelling approvals at the Greater Capital City Statistical Area level for FY2024–25 (original series). Source: ABS Building Approvals, Australia, GCCSA series for each capital city.

Why WA is struggling to build more townhouses and small-scale infill

Townhouses, walk-up flats and other small-scale infill projects make up just 8.6% of new residential approvals in WA, against 17.6% nationally. The most common barrier is cost and financing. At current construction costs, it is hard for apartment and townhouse projects to reach the level of pre-sales needed to secure a construction loan.

The WA Government's 2026–27 Budget included a $250 million Keystart Pre-sale Guarantee to help apartment projects meet those pre-sale requirements. The earlier Infrastructure Development Fund supported more than 10,000 homes across WA, including 5,400 apartments in Perth. Planning reforms around train station precincts are also aimed at encouraging more diverse housing within 800 metres of stations.

Annual approvals by dwelling type

Approvals are rising again, but both categories remain well below past highs. Apartment approvals increased from 601 in 2023 to 2,570 in 2025. Townhouse approvals more than doubled, rising from 918 to 2,232 over the same period.

However, both remain below their previous peaks. Apartment approvals reached 5,202 in 2014, while townhouse approvals reached 3,324 in 2010.

| Calendar year | Detached houses | Townhouses & semis | Apartments | Total new residential | House share | Apartment share |

|---|---|---|---|---|---|---|

| 2020 | 15,404 | 873 | 2,186 | 18,463 | 83.4% | 11.8% |

| 2021 | 22,134 | 1,029 | 2,640 | 25,803 | 85.8% | 10.2% |

| 2022 | 13,969 | 605 | 1,593 | 16,167 | 86.4% | 9.9% |

| 2023 | 12,464 | 918 | 601 | 13,983 | 89.1% | 4.3% |

| 2024 | 17,984 | 1,288 | 1,936 | 21,208 | 84.8% | 9.1% |

| 2025 | 19,204 | 2,232 | 2,570 | 24,006 | 80.0% | 10.7% |

| 12m to Mar 2026 | 20,074 | 2,161 | 2,945 | 25,180 | 79.7% | 11.7% |

SECTION 08 · PERTH VS REGIONAL WA

Perth vs Regional WA: where are most homes being built?

Greater Perth accounted for 87.7% of WA's population growth in 2024–25 and 84.8% of residential approvals. This is higher than its share of the state's total population, which was 80.6%.

Perth also accounted for 94.7% of all final residential lot approvals in WA in the December 2025 quarter.

Perth's share of WA approvals has stayed fairly steady over the past decade, sitting between 82% and 87% in both strong and weak market periods. With lot approvals now heavily focused in the metro area, Perth's share may rise slightly in the upcoming quarters.

Regional WA accounted for 15.2% of approvals, slightly higher than its 12.3% share of population growth. This was supported by lifestyle migration to the South West and steady demand around mining centres.

Source: ABS Regional Population 2024–25; ABS Building Approvals March 2026; WA DPLH State Lot Activity December 2025.

Greater Perth and Regional WA dwelling approvals, FY2019–20 to FY2025–26

Perth consistently accounts for 82–87% of all WA residential approvals each year. Regional WA's share held steady through the 2022–23 downturn. Note: 2025–26 is July to March year-to-date only.

Methodology: WA state total from ABS Building Approvals Table 05. Greater Perth total from Table 10 (Greater Perth GCCSA). Regional WA is derived as WA state total minus Greater Perth. 2025–26 is July to March year-to-date only. Source: ABS Building Approvals, cat. 8731.0, March 2026 release.

What is slowing WA's housing supply?

WA's housing pipeline is concentrated in Perth, where about 85% of the state's housing approvals occur. The slowdown is not caused by one issue. The main pressures are labour shortages, financing constraints, land supply, slower completions and strong population growth.

Six factors stand out:

- Workforce capacity. WA's construction workforce reached a record 172,500 in February 2026, but build times have still lengthened to 5.15 quarters, up from 3.02 in 2019–20.

- Trade shortages. WA and Queensland have the hardest time finding available tradespeople of any state, with infrastructure and mining projects competing for the same workers.

- Apartment project financing. Perth apartment projects have struggled to reach the pre-sales needed to secure construction loans. The WA government's 2026–27 Budget introduced a $250 million pre-sale guarantee specifically to address this.

- Greenfield concentration. Almost all new lots — 94.7% in the December 2025 quarter — were in new land releases on Perth's outer fringe. Most homes built on those lots are likely to be detached houses.

- Slow completion rates. 25,458 dwellings were under construction at the end of 2025, but only 4,626 were completed in the December quarter. At that rate, it would take about 16.5 months to work through what is currently being built.

- Demand pressure. Greater Perth grew by 58,088 residents in 2024–25 (2.4%), the fastest of any capital city.

In regional WA, the South West is drawing lifestyle migration faster than new lot supply can keep up. Margaret River made up 89 of the 238 regional lot approvals in the December 2025 quarter. Most other regional areas recorded single-digit approvals over the same period.

SECTION 09 · THE FULL PICTURE

Will WA meet its Housing Accord target?

WA is projected to reach its 129,000-home target by September 2029, just one quarter behind schedule. That is one of the strongest results among the states, alongside Victoria. Approvals are recovering, completions reached an eight-year high in 2024–25, and the backlog from earlier years is clearing.

However, the broader picture is still mixed:

- Greater Perth is growing faster than any other capital but approving fewer new homes per resident than Brisbane, Melbourne or Sydney.

- WA homes take longer to build than anywhere else in Australia.

- Perth's housing mix is the most detached-heavy of the four largest capital markets, with apartment and townhouse supply running at roughly half the national share.

These issues are not expected to stop WA from meeting its Accord share. But they help explain why conditions remain tight for renters and buyers in Perth, even as the state-level numbers improve.

Required annual pace

25,800

homes per year over 5 years (129,000 ÷ 5)

FY2024–25 completions

22,736

88% of required pace; best result since 2016–17

12m approvals to Mar 2026

25,247

97.9% of required pace

House build time 2024–25

5.15 qtrs

Longest of any state or territory; the national average is about 3.5 quarters

Perth approvals per 1,000 residents added

335

Lowest of the four major capitals

Non-house share of Perth approvals

20.4%

vs 61.3% Sydney, 48.2% Melbourne, 37.0% Brisbane

Methodology: Pace figures derived from WA's 129,000-home Accord allocation (population-share methodology). Approvals and completions from ABS releases. Build times from ABS Building Activity. Sources: NHSAC March 2026 Quarterly Report; ABS Building Approvals (cat. 8731.0); ABS Building Activity (cat. 8752.0); ABS Regional Population (cat. 3218.0).

Population growth has been the main pressure on Perth supply

WA added 97,002 residents in 2022–23 and 87,211 in 2023–24. These were the two largest annual increases on record. In 2022–23, only 15,149 homes were completed. That worked out to 6.40 new residents for every home built.

By 2024–25, the ratio had improved to 2.91 as population growth slowed and completions increased. However, it was still above the 15-year average of around 2.6.

The population jump in the mid-2020s was driven by higher net overseas migration, more people moving from the eastern states, and steady natural population growth.

Full historical data: WA pipeline summary (2010–11 to 2024–25)

General information only

This article draws on publicly available data from the ABS, NHSAC, the WA Department of Planning, Lands and Heritage, and the WA Government's 2026–27 Budget. It is general information only and does not constitute financial, investment or legal advice. All figures are sourced from official Australian government data releases. Forward-looking estimates are drawn from NHSAC modelling and may change as new data becomes available.

ABS Building Approvals, Australia, March 2026 (cat. 8731.0)

ABS Building Activity, Australia, December Quarter 2025 (cat. 8752.0)

ABS Regional Population, Australia, 2024–25 (cat. 3218.0)

ABS National, state and territory population, Sept 2025 (cat. 3101.0)

NHSAC Quarterly Report, March 2026

NHSAC State of the Housing System, 2025

Western Australian Government, 2026–27 State Budget

WA Department of Planning, Lands and Heritage, State Lot Activity, December 2025

Chart Snapshots