NSW housing supply statistics: is the state building enough homes?

New South Wales is projected to fall 118,000 homes short of its Housing Accord target and will not reach it until June 2031, two years late. The state needs to build 75,400 homes a year to stay on track. In the year to December 2025, it completed 45,145, around 40% below the required pace.

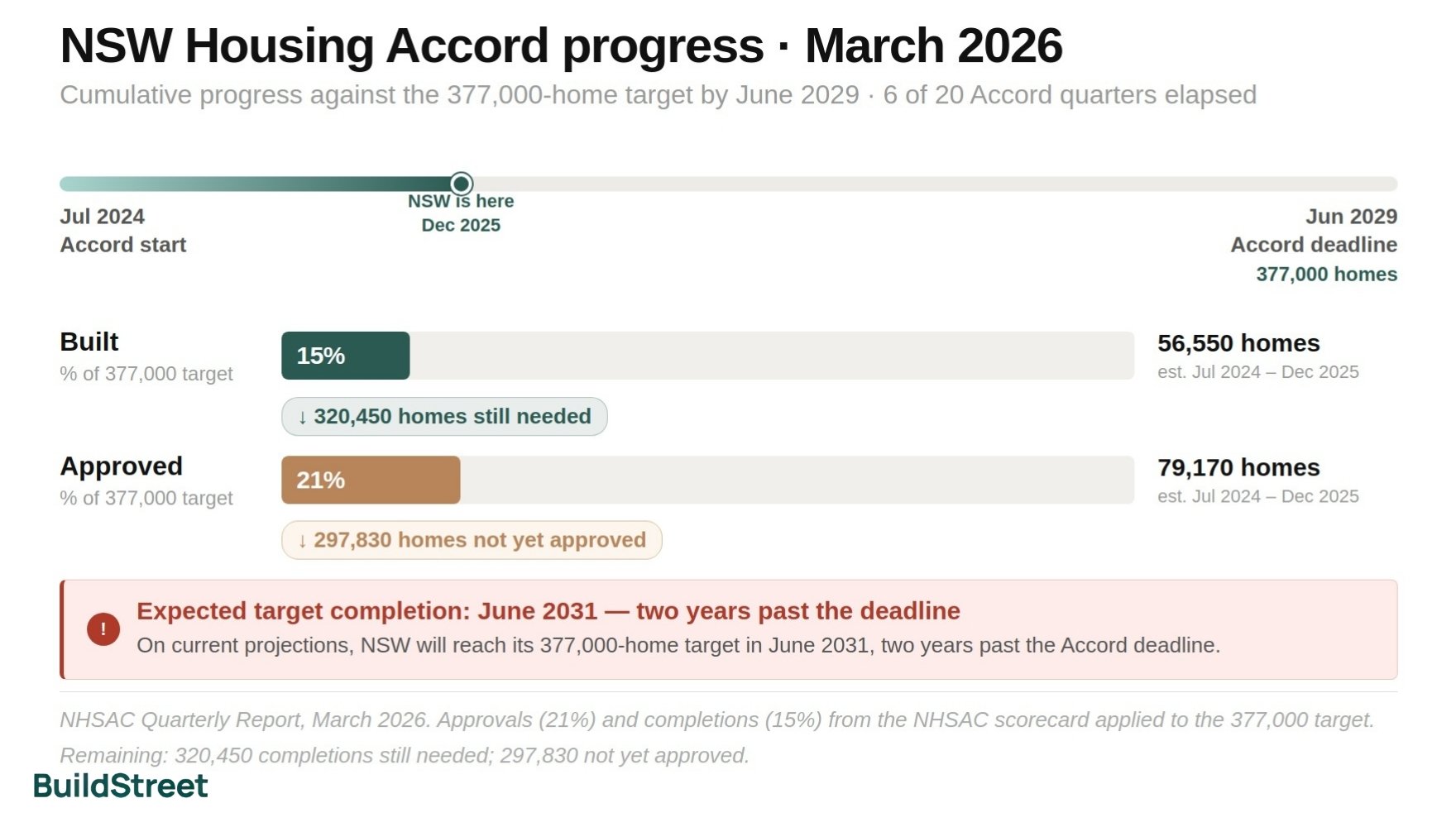

After six quarters of the five-year Accord period, NSW has completed around 15% of its 377,000-home target, against a benchmark of 30%.

NSW Accord target (to 2029)

377,000

75,400 homes a year over 5 years from July 2024

Rolling 12m completions (to Dec 2025)

45,145

59.9% of required annual pace; 30,255 homes below target rate

Expected target completion

Jun 2031

Two years past the June 2029 Accord deadline

SECTION 01 · THE HOUSING TARGET

Housing Accord 2026: how far behind is NSW?

The National Housing Accord is a federal-state agreement targeting 1.2 million new homes across Australia between July 2024 and June 2029. NSW's share is 377,000 homes, or 75,400 a year. The Accord is not legally binding but comes with $3.5 billion in Commonwealth funding to support delivery.

The most reliable way to track progress is completions, because these are the homes actually added to the housing stock. NSW completed 42,646 homes in 2024–25, or 56.6% of the required annual pace. The rolling four-quarter figure to December 2025 was 45,145.

NSW is projected to build around 258,000 new homes over the five-year Accord period, against its allocation of 377,000. That points to a shortfall of roughly 118,000 homes by June 2029, with the target not reached until June 2031.

NSW Housing Accord progress

Cumulative progress against the target of 377,000 homes by June 2029, as at the latest NHSAC quarterly scorecard.

Dec 2025

Accord startJun 2029

Accord deadline

% of 377,000

% of 377,000

Expected target completion: June 2031

On current projections, NSW will reach its 377,000-home target in June 2031, two years past the Accord deadline.

Approvals (21%) and completions (15%) progress figures are taken directly from the National Housing Supply and Affordability Council (NHSAC) quarterly scorecard. Derived estimates (79,170 and 56,550) are calculated by applying those percentages to the 377,000 target and may differ from a direct count by a few thousand homes. Remaining homes are 377,000 minus each cumulative measure: 320,450 completions still needed and 297,830 homes not yet approved. Source: NHSAC Quarterly Report, March 2026.

How NSW compares to other states

NSW has built just 15% of its Housing Accord target so far, the lowest completion rate among the major eastern states. Victoria is at 23%, Queensland at 17%, and Western Australia at 22%.

Nationally, the figure is around 18%. NSW is not expected to reach its allocation until June 2031, two years after the deadline.

| State / Territory | Target (homes) | Completions to date (est.) | % of target built | % approved to date | Expected delivery |

|---|---|---|---|---|---|

| NSW | 377,000 | 56,550 | 15% | 21% | June 2031 |

| Victoria | 342,000 | 78,660 | 23% | 28% | Sep 2029 |

| Queensland | 231,000 | 39,270 | 17% | 26% | Sep 2030 |

| Western Australia | 110,000 | 24,200 | 22% | 29% | Sep 2029 |

| South Australia | 84,000 | 15,960 | 19% | 27% | Sep 2030 |

| Tasmania | 35,000 | 4,200 | 12% | 15% | Sep 2033 |

| Australia | 1,200,000 | 216,000 | 18% | 25% | June 2030 |

Source: NHSAC Quarterly Report, March 2026. Completions to date are estimates derived by applying each jurisdiction's published percentage share to its Accord target.

SECTION 02 · APPROVALS

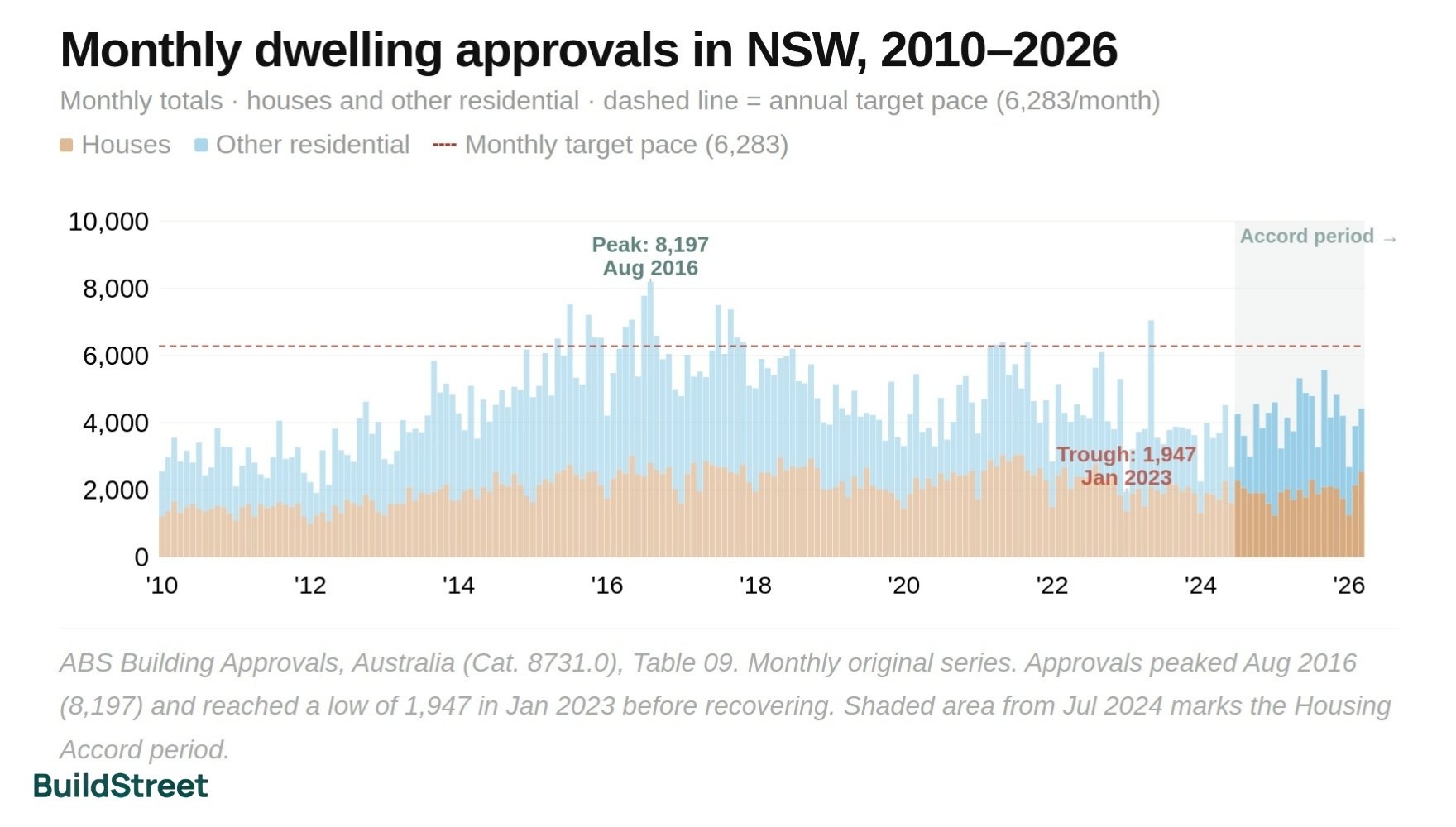

NSW dwelling approvals increased in 2024-25

NSW approved 49,515 dwellings in 2024–25, up 15.1% from 43,018 in 2023–24. This represented an increase in approval activity, although volumes remain below the level needed to support long-term housing supply.

The increase continued into 2025–26. In the nine months from July 2025 to March 2026, NSW approved 37,831 dwellings, up 6.4% compared with the same period a year earlier. On a rolling 12-month basis, approvals reached 51,791 dwellings in March 2026.

In 2024–25, NSW approved 22,381 houses and 27,134 non-house dwellings, including apartments, townhouses and other attached housing. Non-house dwellings accounted for 54.8% of total approvals.

Apartment approvals were concentrated mainly in Inner Sydney, while detached house approvals were more common in outer suburban council areas, including Blacktown, Liverpool, Camden and Campbelltown.

Monthly dwelling approvals in NSW, January 2010 to March 2026

The chart shows annual financial year totals. Approvals peaked in 2015–16 at 73,489 and have remained well below the 75,400-per-year Accord pace since.

Methodology: Annual financial-year totals from ABS Building Approvals, Table 09: NSW total dwelling units. Target pace = 377,000 ÷ 5 years = 75,400/year. Source: ABS Building Approvals, cat. 8731.0, March 2026 release.

What is holding back housing approvals?

Approval numbers are improving, but the pipeline is still being slowed by several practical constraints. These affect how quickly projects move from planning policy into approved, financeable and buildable homes.

Several issues are holding back the approvals pipeline:

- Planning delays: Many sites zoned for medium- or high-density development still face slow development application processes, even after state-level upzoning through the Transport Oriented Development program.

- Project viability: Higher construction costs, financing rates and slower apartment pre-sales have made some projects harder to progress, particularly across inner and middle-ring Sydney.

- Builder insolvencies: The rise in builder insolvencies between 2022 and 2024 added further uncertainty for developers and lenders.

SECTION 03 · COMMENCEMENTS

Approved homes are moving into construction more slowly

NSW commenced construction on 46,686 dwellings in 2024–25, up 15.9% from 40,267 the year before. This was still below the 2016–17 peak of 74,126 and around 38% below the annual pace required under the Accord.

Momentum improved in late 2025. The December 2025 quarter recorded 16,604 commencements, the strongest quarterly result in several years. On a rolling four-quarter basis, NSW reached 52,878 commencements in the year to December 2025, equal to about 70% of the annual pace required.

At December 2025, 79,304 dwellings were under construction in NSW, including 20,966 houses and 57,938 other residential dwellings. A further 12,870 dwellings had been approved but not yet commenced, including 9,209 other residential dwellings and 3,477 houses. The backlog of approved-but-not-started dwellings was concentrated in higher-density housing, which can be more difficult to progress due to project viability, financing and pre-sale requirements.

NSW dwelling commencements by type, 2004–05 to 2024–25

Commencements recovered in 2024–25 but remain far below both the 2016–17 peak and the Accord target pace.

Methodology: ABS Building Activity, Table 34 (NSW Total Sectors, quarterly), aggregated to financial years. Other residential is derived as total minus houses. 2025–26 bar covers July to December 2025 only. Source: ABS Building Activity, cat. 8752.0, December 2025 release.

Why are approvals not converting into construction starts?

An approval is an important step in the housing pipeline, but it does not guarantee that work will begin straight away. Projects still need labour, finance, builder capacity and, in many cases, enough buyer demand to move from approval into construction.

Three main barriers are slowing progress:

- Trades shortages: Skilled workers, including carpenters, concreters, electricians and plumbers, remain in short supply nationally.

- Builder insolvencies: Insolvencies between 2022 and 2024 left some approved projects without a builder, requiring a replacement before work could begin.

- Financing and pre-sales: For apartment and medium-density projects, difficult financing conditions and pre-sale targets have led some developers to pause or rework projects before breaking ground.

SECTION 04 · COMPLETIONS

Housing completions remain below target despite late-2025 improvement

NSW completed 42,646 homes in 2024–25, down 9.0% from 46,865 in 2023–24. The rolling four-quarter figure improved to 45,145 by December 2025, as more homes already under construction started reaching completion. The December 2025 quarter recorded 13,358 completions, the highest quarterly result in recent periods.

For context, NSW completions last peaked at 74,683 in 2018–19, supported by a large volume of construction starts between 2015 and 2018. The current pipeline is much smaller. In 2024–25, NSW completed 22,698 houses, 19,374 other residential dwellings and 574 conversions, showing that the apartment and medium-density pipeline has not yet fully flowed through to completed homes.

Build times have also increased. In 2024–25, a new NSW house took 4.10 quarters, or about 12.3 months, from approval to completion. That was up 31% from 3.13 quarters in 2019–20. This helps explain why a large number of homes under construction are not turning into finished homes as quickly as they did in the late 2010s.

NSW housing completions vs Accord target pace, 2010–11 to 2025–26

Completions peaked in 2018–19 and have declined in most years since. At 42,646 in 2024–25, they are 43% below the Accord pace of 75,400 a year.

Methodology: ABS Building Activity, Table 39 (Total Sectors, Total Type of Building, Total Type of Work), quarterly original series aggregated to financial years. The 2025–26 bar reflects July to December 2025 only. Source: ABS Building Activity, cat. 8752.0, December 2025 release.

SECTION 05 · SYDNEY VS REGIONAL NSW

Where are new homes being approved in NSW?

Housing approvals in NSW are heavily concentrated in Greater Sydney, which means the state's overall supply pipeline is closely tied to Sydney's approval activity.

Greater Sydney accounted for 33,573 of the state's 49,515 approvals in 2024–25, or 67.8%. In the first nine months of 2025–26, Sydney's share remained similar at 67.5%. The five most active councils in 2025–26 year-to-date were Parramatta, with 2,480 approvals, The Hills Shire with 2,319, Blacktown with 1,845, Liverpool with 1,590 and Canada Bay with 1,404. Outside Greater Sydney, the most active regional markets in 2025–26 year-to-date were Wollongong with 1,029 approvals, Maitland with 935, Central Coast with 918, Lake Macquarie with 896 and Shoalhaven with 661.

These are solid local approval numbers, but no individual regional market is large enough on its own to offset slower activity in Sydney.

Greater Sydney vs regional NSW dwelling approvals, 2019–20 to 2025–26

Sydney has consistently driven about 68% of all NSW approvals. Sydney's share of non-house (apartment and medium-density) approvals is even higher, at about 75%.

2024–25 Breakdown

Methodology: NSW state total from ABS Building Approvals Table 09. Greater Sydney total from Table 10 (Greater Sydney GCCSA). Regional NSW is derived as NSW total minus Greater Sydney. 2025–26 is July to March YTD only. Source: ABS Building Approvals, cat. 8731.0, March 2026 release.

Why regional NSW is struggling to build enough

Regional NSW has different housing supply pressures from Greater Sydney, but the outcome is similar: new housing is not being delivered quickly enough to meet demand. In many areas, the challenge is not only planning approval, but whether land, infrastructure, labour and project economics can support new homes at scale.

Regional NSW faces several supply challenges:

- Infrastructure gaps: Many regional growth corridors lack the water, sewerage and road capacity needed to support new housing at scale. Rezoning land is only useful when the infrastructure to service it is also in place.

- Higher build costs: Limited local tradespeople, shorter supply chains and transport costs can push build prices in regional NSW above those on the metropolitan fringe.

- Lower presale prices: In smaller towns and cities, lower property prices mean developers have less room to cover costs, making apartments and townhouses harder to justify financially.

- Rental pressure: Rents on new leases in regional NSW were among the least affordable in the country in 2025, driven by years of limited new supply relative to population growth.

SECTION 06 · THE SHORTFALL

The NSW housing target gap remains large

NSW is projected to complete around 258,000 homes over the five Accord years to June 2029, compared with its allocation of 377,000. That leaves a projected shortfall of about 118,000 homes.

The gap reflects the same issues seen throughout the pipeline: approvals are improving, construction starts are rising, and completions have lifted in recent quarters, but none are yet moving fast enough to close the shortfall.

To reach the target, the state would need a sustained lift in completions, supported by faster approvals, stronger project viability, more construction capacity and infrastructure that can support new housing at scale.

NSW cumulative completions vs Housing Accord target pace, July 2024 to December 2025

NSW is tracking at roughly half the pace needed. By December 2025, it had completed 68,882 homes against a straight-line target of 113,100 for the same period.

Methodology: Target pace = 377,000 ÷ 20 quarters = 18,850/quarter, accumulated from 1 July 2024. Actual quarterly completions from ABS Building Activity, Table 39. The gap of 44,218 at December 2025 is the difference between the straight-line benchmark (113,100) and actual cumulative completions (68,882). Source: ABS Building Activity, cat. 8752.0, December 2025 release; NHSAC Housing Accord target.

How the housing gap is affecting renters and buyers

For renters and buyers, the housing shortage has had clear financial consequences. National rental affordability reached a record low in 2025, with 33.1% of median household income needed to service a new lease. Rental stress also increased, with 29% of renter households in rental stress in 2024, up from 24% in 2021. In regional New South Wales, rents on new leases were among the least affordable in the country. At the same time, the time needed to save a 20% deposit rose to 11.2 years in 2025, a national record.

Deposit saving time (2025)

11.2 yrs

Years to save a 20% deposit nationally, a record high

Rental affordability (2025)

33.1%

Median household income share needed for a new lease; worst on record

Renter households in stress

29%

Of all renter households in 2024, up from 24% in 2021

Projected shortfall by 2029

118,000

Homes below NSW Accord target by June 2029 (estimate)

Homes behind pace (Dec 2025)

44,218

NSW completions below straight-line Accord pace after 6 quarters

Expected target date

Jun 2031

Two years past the June 2029 Accord deadline

Source: NHSAC State of the Housing System, 2025; NHSAC Quarterly Report, March 2026.

Population growth is outpacing housing delivery

Across the 15 financial years to 2024–25, NSW averaged about 2.2 people for every home completed. The ratio was strongest in 2018–19, when NSW completed 74,683 homes while the population increased by 92,272 people. This equalled 1.24 people per completed home.

The gap widened from 2022. In 2022–23, NSW added 174,289 residents but completed only 48,615 homes, equal to 3.59 people per completed home. By 2024–25, the ratio had eased to 2.36 as population growth slowed, but it remained above the long-run average, indicating continued pressure on housing availability.

SECTION 07 · HISTORICAL CONTEXT

How today's NSW housing pipeline compares with past cycles

The last time NSW came close to the current Accord pace was 2018–19, when it completed 74,683 homes. That was just 1% below the 75,400 homes needed each year. By comparison, the 2024–25 result of 42,646 completions was 43% below the 2018–19 peak. On approvals, the closest NSW has come to the current annual pace was 2015–16, when 73,489 dwellings were approved.

At December 2025, NSW had 79,304 homes under construction, which was close to the late-2010s high. However, homes are now taking longer to complete, meaning the construction pipeline is not converting into finished homes at the same rate.

Approvals peak (since 2010–11)

73,489

2015–16; about −2.5% versus today's required pace

Completions peak (since 2010–11)

74,683

2018–19; the only year within 1% of the Accord pace

2024–25 vs 2018–19 peak

−43%

42,646 completed vs 74,683 at the peak; same state, half the output

Stock under construction

79,304

At Dec 2025, near the 2017–18 high, but converting more slowly

+View full historical data table16 financial years · 4 toggleable views

| FY | Approvals | Commencements | Completions | Under construction (EOY) | Approved, not yet started (EOY) |

|---|---|---|---|---|---|

| 2010–11 | 34,631 | 32,309 | 32,367 | 32,540 | 10,392 |

| 2011–12 | 35,204 | 30,827 | 28,233 | 35,146 | 12,359 |

| 2012–13 | 42,823 | 42,377 | 33,063 | 43,670 | 11,336 |

| 2013–14 | 54,095 | 47,595 | 38,981 | 51,529 | 14,298 |

| 2014–15 | 63,419 | 57,746 | 47,684 | 60,785 | 16,551 |

| 2015–16 | 73,489 | 70,263 | 53,478 | 76,193 | 19,647 |

| 2016–17 | 72,731 | 74,126 | 63,463 | 85,023 | 18,216 |

| 2017–18 | 72,856 | 71,776 | 65,063 | 89,973 | 20,047 |

| 2018–19 | 57,982 | 62,460 | 74,683 | 75,766 | 15,433 |

| 2019–20 | 48,748 | 50,123 | 59,935 | 64,686 | 13,759 |

| 2020–21 | 60,213 | 59,558 | 51,202 | 71,203 | 10,990 |

| 2021–22 | 55,574 | 54,501 | 45,192 | 78,514 | 12,611 |

| 2022–23 | 52,315 | 50,234 | 48,615 | 78,911 | 13,675 |

| 2023–24 | 43,018 | 40,267 | 46,865 | 71,456 | 16,884 |

| 2024–25 | 49,515 | 46,686 | 42,646 | 75,762 | 15,790 |

| 2025–26 YTD* | 37,831 | 29,419 | 26,236 | 79,304 | 12,870 |

Methodology: Approvals: ABS Building Approvals (cat. 8731.0) Table 09. Commencements: ABS Building Activity (cat. 8752.0) Table 35 & 34. Completions: Table 39. Under construction (EOY): Table 77. Approved-but-not-yet-commenced: Table 80. NSW population: ABS Regional Population (cat. 3218.0). * 2025–26 YTD covers nine months of approvals (Jul 2025 to Mar 2026) and two quarters of commencements/completions (Jul–Dec 2025); stock at December 2025. † Approvals YTD vs 9-month pro-rated target of 56,550. ‡ Commencements/completions YTD vs half-year pro-rated target of 37,700. Sources: ABS Building Approvals (cat. 8731.0) March 2026; ABS Building Activity (cat. 8752.0) December 2025; ABS Regional Population (cat. 3218.0) 2024–25 release.

General information only

This article draws on publicly available data from the ABS, NHSAC and NSW Planning. It is general information only and does not constitute financial, investment or legal advice. All figures are sourced from official Australian government data releases. Forward-looking estimates are drawn from NHSAC modelling and may change as new data becomes available.

ABS Building Approvals, Australia, March 2026 (cat. 8731.0)

ABS Building Activity, Australia, December Quarter 2025 (cat. 8752.0)

NHSAC Quarterly Report, March 2026

NHSAC State of the Housing System, 2025

NSW Planning — Greater Sydney housing forecast and Housing Delivery Authority

Australian Government — National Housing Accord, August 2023

Chart Snapshots