Australian cities building the most homes in 2026

Melbourne approved more new homes than any other capital city in FY2024–25, recording 46,530 dwelling approvals. That was 38.6% higher than Sydney, which ranked second with 33,573 approvals despite being one of Australia's fastest-growing cities.

Across Australia, dwelling approvals rose 14.3% to 187,662, recovering from a decade low and signalling a stronger future housing pipeline. Perth recorded the fastest capital-city growth, while Queensland's major markets also showed strong momentum, with Brisbane City ranking as the top council nationally.

National total FY2024–25

187,662

Dwelling approvals · +14.3% year-on-year

Leads all capital cities

46,530

Greater Melbourne · 8th consecutive year at #1

Fastest growing capital

+30.7%

Greater Perth · from 14,889 in FY2023–24

Top LGA nationally

7,285

Brisbane City LGA · more than TAS and NT combined

SECTION 01 · CITY OVERVIEW

Melbourne leads Australian cities for new home approvals

Capital city approvals show where Australia's new housing pipeline is strongest.

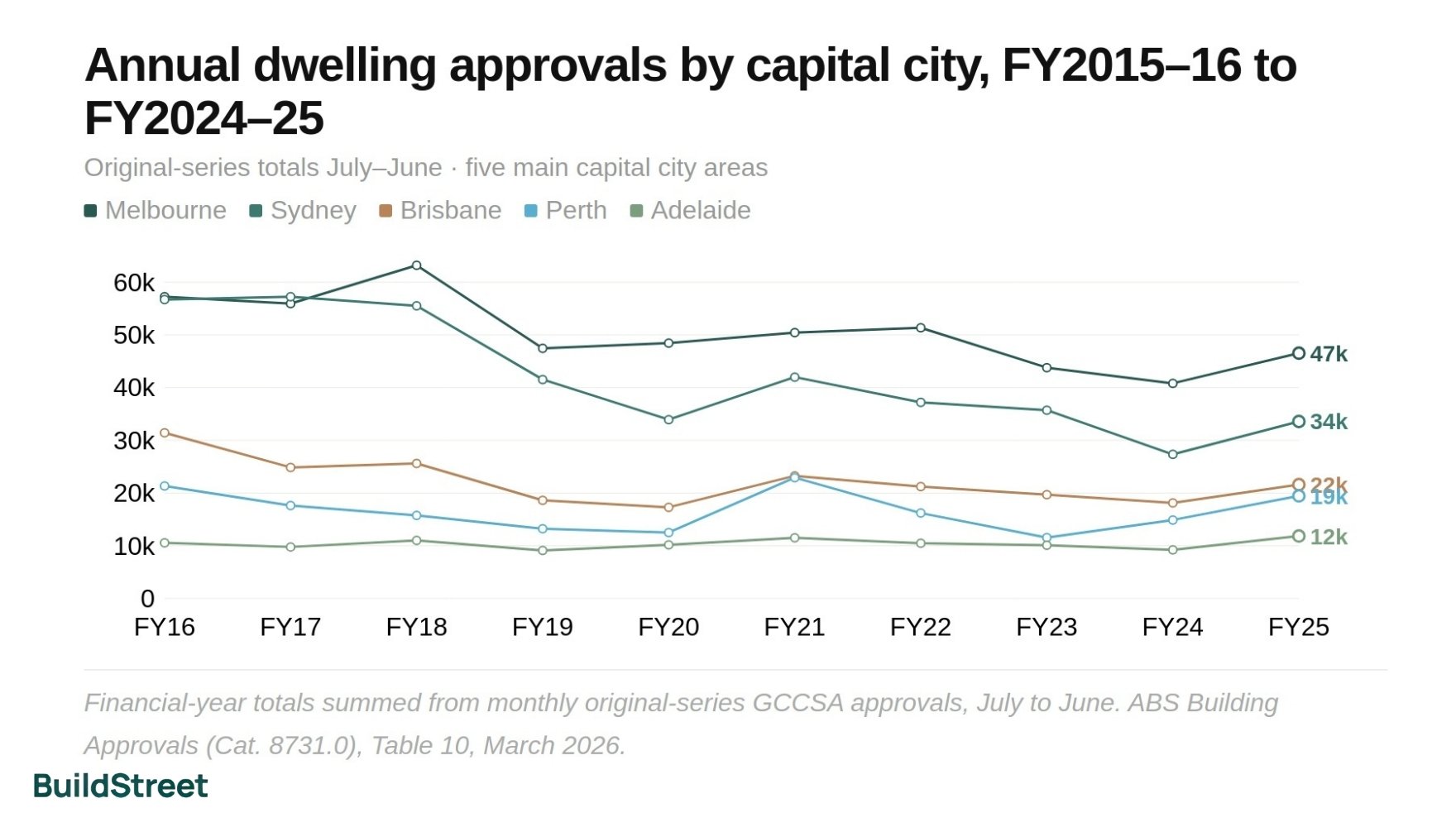

Melbourne has recorded the highest number of dwelling approvals among Australian capital cities for eight consecutive years. In FY2024–25, Greater Melbourne approved 46,530 dwellings, which was 12,957 more than Greater Sydney. That gap was larger than Greater Adelaide's total annual approvals.

Use the buttons above to compare city trajectories over the past decade.

Annual dwelling approvals by capital city area, FY2015–16 to FY2024–25

Original-series totals July–June. Click the city buttons above to show or hide individual markets. Hobart and Darwin are hidden by default.

Methodology: Financial-year totals are the sum of monthly original-series GCCSA approvals, July to June. Source: ABS Building Approvals (Cat. 8731.0), Table 10, March 2026.

Melbourne's lead over Sydney has widened

Melbourne approved 12,957 more dwellings than Sydney in FY2024–25. That gap was larger than Greater Adelaide's total annual approvals. In FY2015–16, the gap between Melbourne and Sydney was almost zero. Sydney now records 6.0 approvals per 1,000 residents, the lowest of any major capital, compared with Melbourne's 8.6 approvals per 1,000 residents.

Perth approvals are recovering from a sharp fall

Perth's approvals fell 49.6% from FY2020–21 to FY2022–23, a steeper correction than any other major capital. The recovery to 19,458 in FY2024–25 represents a 68.6% rebound from the trough over two years. Current FY2025–26 year-to-date data shows Perth approvals running 13.7% above the same period a year earlier.

About the data

This article uses ABS dwelling approvals as its primary measure. Approvals lead construction by roughly 12 to 18 months for houses and longer for multi-unit projects, and not all approvals proceed to completion. Capital city comparisons use Greater Capital City Statistical Areas (GCCSAs), the official ABS labour-market city boundaries. Regional city comparisons use SA4 boundaries. Council comparisons use individual LGA boundaries. The "non-house" category includes apartments, townhouses and all other attached dwelling forms; it is not a pure apartment count.

SECTION 02 · CITY RANKINGS

Top Australian cities for new home approvals

The four largest capital cities, Melbourne, Sydney, Brisbane and Perth, together account for 64.6% of all national approvals. Melbourne has been the clear leader since FY2017–18.

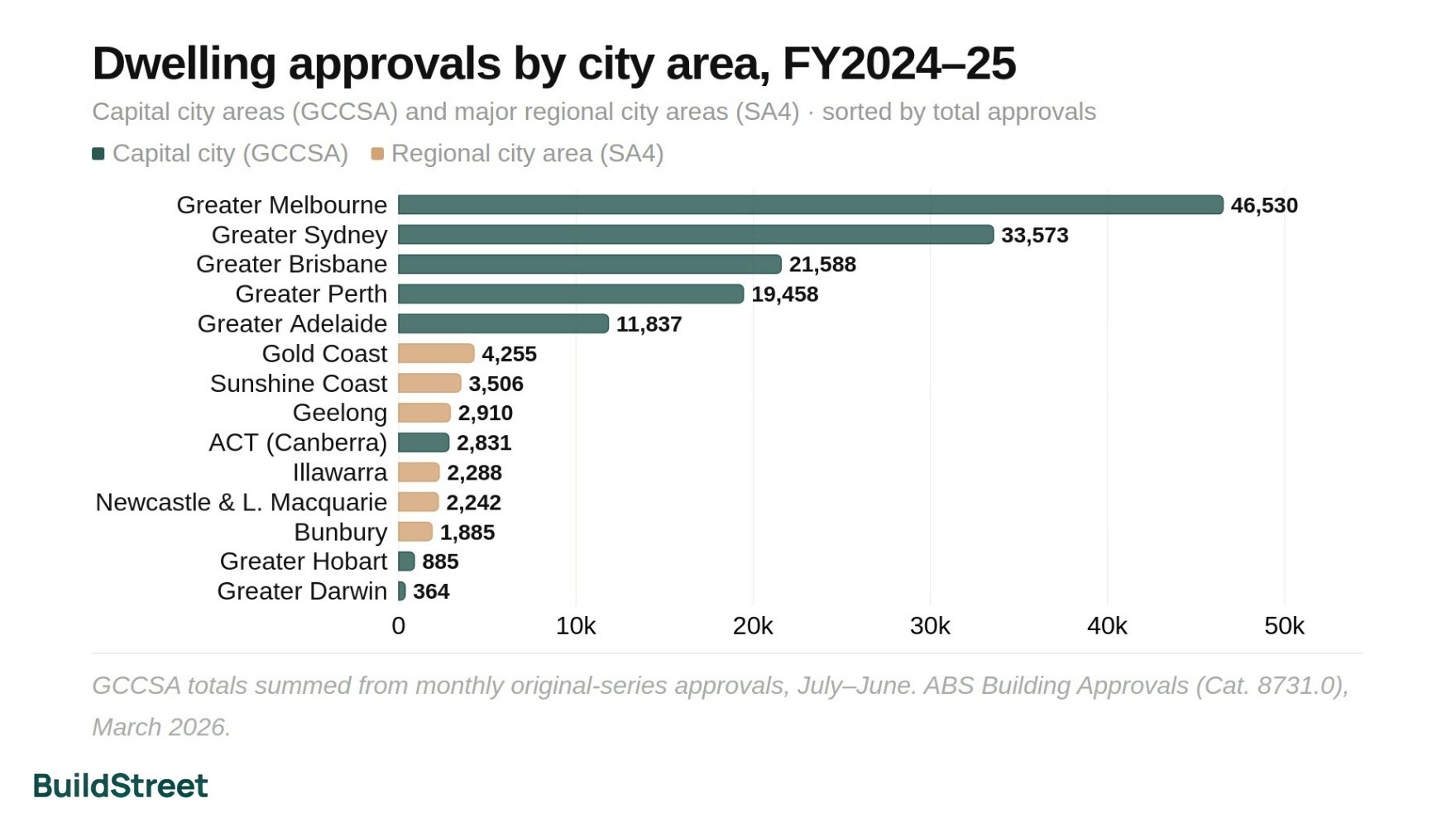

Among regional areas, the Gold Coast ranks highest at 4,255 approvals, ahead of the ACT in volume.

Bunbury's presence in the top twelve reflects the pace of Perth's extended growth corridor into southwest WA, where 95.4% of approvals are detached houses.

Dwelling approvals by city area, FY2024–25

Capital city areas (GCCSA, dark teal) and major regional city areas (SA4, amber), sorted by total approvals.

Methodology: GCCSA totals summed from monthly original-series approvals, July–June. Source: ABS Building Approvals (Cat. 8731.0), March 2026.

| City area | Type | Total approvals FY24-25 | Houses | Non-house | House % | YTD '25-26 | YTD % of FY24-25 |

|---|---|---|---|---|---|---|---|

| Greater Melbourne | GCCSA | 46,530 | 24,101 | 22,429 | 51.8% | 32,551 | 70.0% |

| Greater Sydney | GCCSA | 33,573 | 12,987 | 20,586 | 38.7% | 25,552 | 76.1% |

| Greater Brisbane | GCCSA | 21,588 | 13,606 | 7,982 | 63.0% | 18,686 | 86.6% |

| Greater Perth | GCCSA | 19,458 | 15,490 | 3,968 | 79.6% | 16,329 | 83.9% |

| Greater Adelaide | GCCSA | 11,837 | 7,857 | 3,980 | 66.4% | 9,064 | 76.6% |

| Gold Coast | SA4 | 4,255 | 1,325 | 2,930 | 31.1% | 5,633 | 132% |

| Sunshine Coast | SA4 | 3,506 | 1,984 | 1,522 | 56.6% | 2,657 | 75.8% |

| Geelong | SA4 | 2,910 | 2,434 | 476 | 83.6% | 2,556 | 87.8% |

| Australian Capital Territory | GCCSA | 2,831 | 705 | 2,126 | 24.9% | 3,285 | 116% |

| Illawarra | SA4 | 2,288 | 743 | 1,545 | 32.5% | 1,644 | 71.9% |

| Newcastle and Lake Macquarie | SA4 | 2,242 | 1,172 | 1,070 | 52.3% | 1,548 | 69.0% |

| Bunbury | SA4 | 1,885 | 1,799 | 86 | 95.4% | 1,264 | 67.1% |

| Greater Hobart | GCCSA | 885 | 822 | 63 | 92.9% | 775 | 87.6% |

| Greater Darwin | GCCSA | 364 | 297 | 67 | 81.6% | 346 | 95.1% |

Methodology: GCCSA = Greater Capital City Statistical Area (monthly original series). SA4 = ABS regional area. Non-house proxy = total minus houses. YTD = July–March 2025–26. Values above 100% (Gold Coast 132%, ACT 116%) indicate the current-year run rate already exceeds last year's full-year total. Source: ABS Building Approvals (Cat. 8731.0), March 2026.

MONTHLY TRENDS

Which capital city is approving the most new homes?

Perth's monthly recovery stands out in the data. Its approvals rose from monthly lows of between 700 and 900 in early 2023 to consistently above 1,500 per month since mid-2024. Queensland's monthly run-rate in the second half of 2025 reached its strongest sustained levels in recent years, due to strong activity across Brisbane City, the Gold Coast, Sunshine Coast, Logan and Moreton Bay.

Seasonal cycles are consistent across every capital. December and January regularly record lower approvals as building activity winds down, while spring months often bring a surge in house consents.

Sydney's monthly approvals, which briefly fell below 1,000 in January 2023, recovered strongly in 2024 and remain above their 2019–23 average. Melbourne shows increased volatility in the current year, with a sharp February 2026 reading of 4,860 following a soft January of 1,608.

Monthly dwelling approvals by capital city area, January 2015 to March 2026

Original-series monthly totals. Shaded region marks the current financial year (July 2024 onward).

- Melbourne

- Sydney

- Brisbane

- Perth

- Adelaide

Methodology: Monthly original-series GCCSA totals. Smaller markets (ACT, Hobart, Darwin) excluded for scale clarity. Source: ABS Building Approvals (Cat. 8731.0), Table 10, March 2026.

REGIONAL CITIES

Gold Coast, Sunshine Coast, Geelong: the regional cities driving approvals

The Gold Coast is the standout performer. In the nine months to March 2026, it recorded 5,633 approvals, already equal to 132% of its full FY2024–25 total.

At an annualised pace approaching 7,500, it would rank above Greater Darwin, Greater Hobart and the ACT in absolute volume.

The Sunshine Coast and Geelong are the next busiest regional areas, with 3,506 and 2,910 approvals, respectively. At the other end of the spectrum, Bunbury's 1,885 approvals are almost entirely detached houses, making it the most house-intensive major city area in the country.

The Gold Coast also has the most apartment-heavy pipeline of any regional city. At 68.2% non-house approvals, it is more apartment-intensive than Brisbane itself, driven by high-density development along the coastal corridor.

SECTION 03 · DETACHED HOUSES

Where are the most separate houses being built?

Perth approved more houses than Sydney in FY2024–25. Despite being Australia's second-largest market overall, Greater Sydney recorded only 12,987 house approvals, fewer than both Perth (15,490) and Brisbane (13,606). Greater Melbourne led the field with 24,101.

House approvals are concentrated in outer-urban growth corridors.

| Capital city area | House approvals FY2024–25 | Houses share | Key growth corridors |

|---|---|---|---|

| Greater Melbourne | 24,101 | 51.8% | Wyndham, Melton, Hume, Mitchell |

| Greater Perth | 15,490 | 79.6% | Wanneroo, Swan, Rockingham, Armadale |

| Greater Brisbane | 13,606 | 63.0% | Ipswich, Logan, Moreton Bay north |

| Greater Sydney | 12,987 | 38.7% | South West, Outer South West, Hills |

| Greater Adelaide | 7,857 | 66.4% | Playford, Onkaparinga, Gawler |

| Greater Hobart | 822 | 92.9% | Brighton, Sorell, Derwent Valley |

| Greater Darwin | 297 | 81.6% | Palmerston south |

| Australian Capital Territory | 705 | 24.9% | Molonglo, Gungahlin, Denman Prospect |

Methodology: House sub-totals from ABS GCCSA original series. Houses share = house approvals divided by total approvals. Source: ABS Building Approvals (Cat. 8731.0), March 2026.

At the LGA level, the councils with the highest house approvals are almost all in outer-urban growth corridors. Wyndham (VIC) approved 4,049 houses, followed closely by Melton (VIC, 3,991). Queensland's outer ring is led by Logan (3,435 houses) and Ipswich (2,452). In WA, Wanneroo approved 3,276 houses, 95.6% of its 3,425 total, with the Alkimos-Eglinton corridor alone contributing 1,382 dwellings. SA's Playford LGA (2,113 houses) accounts for 20.3% of all SA house approvals, driven by the Munno Para West-Angle Vale corridor, which added 1,322 dwellings in FY2024–25.

APARTMENT SUPPLY

The cities and suburbs leading apartment approvals

Melbourne and Sydney together account for 70.3% of all non-house approvals across Australia's eight capital cities. Greater Melbourne leads in volume with 22,429 non-house dwellings in FY2024–25. Greater Sydney's 20,586 is second, representing a higher share of its total at 61.3%, compared with Melbourne's 48.2%.

The ACT is the most apartment-intensive market by share at 75.1% non-house, reflecting its urban consolidation planning framework. Tasmania is at the opposite end: houses account for 92.9% of Greater Hobart approvals and 95.0% of all Tasmania approvals.

Melbourne City LGA is the most extreme example, approving just 2 houses against 3,844 non-house dwellings in FY2024-25. Parramatta and Port Phillip tell a similar story, each recording non-house shares above 90%.

Houses vs non-house dwelling approvals, FY2024–25, by capital city area

Sorted by non-house share, highest to lowest. Teal = detached houses, blue = non-house (apts, townhouses etc).

Methodology: Houses and non-house from ABS GCCSA original series. Non-house is not a pure apartment count. Source: ABS Building Approvals (Cat. 8731.0), March 2026.

SECTION 04 · POPULATION VS SUPPLY

Where population growth and housing supply are out of step

Sydney approves the fewest homes per resident of any major capital.

Despite recording population growth of 1.35%, Greater Sydney approved just 6.0 dwellings per 1,000 residents in FY2024–25, well below Melbourne's 8.6, Perth's 8.0 and Adelaide's 8.0.

| Capital city area | FY2024–25 approvals | Per 1,000 residents | Population growth 2024–25 |

|---|---|---|---|

| Greater Melbourne | 46,530 | 8.6 | +1.97% |

| Greater Perth | 19,458 | 8.0 | +2.43% |

| Greater Adelaide | 11,837 | 8.0 | +1.27% |

| Greater Brisbane | 21,588 | 7.7 | +2.10% |

| Greater Sydney | 33,573 | 6.0 | +1.35% |

| Australian Capital Territory | 2,831 | 5.9 | +1.30% |

| Greater Hobart | 885 | 3.5 | +0.21% |

| Greater Darwin | 364 | 2.3 | +1.74% |

Methodology: Approvals per 1,000 residents = FY2024–25 GCCSA approvals divided by estimated resident population × 1,000. Population growth from ABS Regional Population, 2024–25. Source: ABS Building Approvals (Cat. 8731.0); ABS Regional Population, 2024–25.

Darwin has the third-highest population growth rate among the eight capitals at 1.74%, yet the lowest approvals per 1,000 residents at 2.3. Logistics cost premiums, limited builder competition, and lower land values consistently suppress new construction relative to demand. This helps explain why both jurisdictions consistently underbuild relative to their population size and growth rate.

Hobart's population growth is the weakest of any capital at just 0.21%, and its low per-capita approval rate reflects genuinely weaker demand rather than a supply-demand mismatch.

SECTION 05 · STATE COMPARISON

Which states are building the most homes?

Victoria approved more homes than any other state in FY2024-25 at 56,581, but its current-year momentum has stalled. Its July to March 2025-26 total is running 5.5% below the same period a year earlier.

Queensland is leading on current momentum at 21.5% growth, followed by Western Australia at 13.7%. The faster percentage gains in FY2024-25 came from smaller bases, with WA up 31.4% and SA up 28.5%. New South Wales and Queensland rounded out the top three by volume at 49,515 and 38,229, respectively.

| State / territory | FY2023–24 | FY2024–25 | Change | Jul–Mar 2025–26 | YTD change |

|---|---|---|---|---|---|

| Victoria | 51,921 | 56,581 | +9.0% | 41,432 | −5.5% |

| New South Wales | 43,018 | 49,515 | +15.1% | 37,831 | +6.4% |

| Queensland | 32,995 | 38,229 | +15.9% | 34,996 | +21.5% |

| Western Australia | 17,465 | 22,945 | +31.4% | 19,097 | +13.7% |

| South Australia | 11,295 | 14,517 | +28.5% | 10,988 | +3.4% |

| ACT | 4,549 | 2,831 | −37.8% | 3,285 | +77.9% |

| Tasmania | 2,569 | 2,341 | −8.9% | 1,933 | +5.5% |

| Northern Territory | 437 | 703 | +60.9% | 559 | +8.8% |

| Australia | 164,249 | 187,662 | +14.3% | 150,121 | +7.4% |

Methodology: Financial-year totals are the sum of monthly state original-series approvals. Jul–Mar 2025–26 is compared with the same nine months in 2024–25. Source: ABS Building Approvals (Cat. 8731.0), March 2026.

SECTION 06 · LGA RANKINGS

Brisbane City leads Australia's councils on housing approvals

Brisbane City Local Government Area (LGA) is the highest-approving council in Australia. Its 7,285 approvals in FY2024–25 represent 19.1% of Queensland's entire state output from a single council, more than Tasmania (2,341) and the Northern Territory (703) combined. Its mix included 4,287 non-house dwellings and 2,974 detached houses.

The top 15 councils nationally account for roughly 30% of all approvals across the country's 537 LGAs. Wyndham (4,571) and Melton (4,563) are primarily greenfield house markets, with Wyndham's Tarneit, Truganina and Wyndham Vale corridors among the fastest-developing areas in the country. Melbourne City itself (3,903) is nearly all apartments: just 2 houses in FY2024–25.

Top 15 LGAs nationally: total dwelling approvals, FY2024–25

All states combined, coloured by state. Brisbane City LGA leads with 7,285 approvals.

Brisbane City, QLD

Methodology: LGA totals from ABS state LGA data cubes, FY2024–25. "Total dwellings" includes all new approved dwellings. Minor differences between house + non-house sub-totals and the published LGA total reflect rounding or a small residual category. Source: ABS Building Approvals (Cat. 8731.0), LGA data cubes, FY2024–25.

In WA, Wanneroo's 3,276 house approvals include 1,382 dwellings in the Alkimos-Eglinton corridor alone. In SA, Playford's Munno Para West-Angle Vale corridor contributed 1,322 of the LGA's 2,302 total.

In NSW, The Hills Shire and Parramatta represent opposite ends of the supply spectrum. The Hills recorded 3,702 approvals, predominantly greenfield house-and-land. Parramatta is 90.2% non-house across 3,213 approvals, driven by high-rise projects in the Parramatta CBD and the Carlingford renewal corridor (1,059 non-house approvals)

KEY DRIVERS

The reasons why some cities are building more homes than others

Melbourne's approval rate of 8.6 per 1,000 residents, compared with Sydney's 6.0, is one of the sharpest contrasts in the data. Five factors explain most of the variation between cities, and they interact differently in each market.

Land supply and greenfield release programmes

Cities with active land release programmes, including outer Melbourne, Perth's northern and southeastern corridors and SEQ's outer ring, consistently produce higher approval volumes. Sydney's lower approvals per 1,000 residents may reflect a mix of land constraints, planning settings, rezoning timelines and project feasibility issues. The exact mix of causes is debated.

Population growth and migration patterns

Perth's approval surge from FY2023–24 tracks a major migration wave tied to the resources sector. Brisbane and the Gold Coast have sustained strong interstate migration from Sydney and Melbourne. Darwin and Hobart have low per-capita approval rates that correspond with weaker population growth, though Darwin's case is also heavily influenced by construction costs.

Multi-unit project feasibility

Apartment and townhouse approvals depend on pre-sales to secure construction finance, which in turn depends on market confidence and pricing. In markets where values have risen strongly, such as Perth, Brisbane and the Gold Coast, feasibility has improved and non-house approvals have grown. In Melbourne, higher land tax on investment properties and state government policy changes appear to have reduced investor appetite.

Freight and logistics cost penalties

Tasmania and the Northern Territory face structural cost disadvantages. Materials shipped across Bass Strait or from southern ports add significantly to every build, suppressing new construction relative to demand. This helps explain why both jurisdictions consistently underbuild relative to their population size and growth rate.

Planning approval speed and local implementation

State planning reforms have accelerated some development application processing, but council-level implementation remains uneven. Queensland's current approval momentum suggests its pipeline is moving faster than several other states, though approval speed can vary significantly by council and project type.

SECTION 7 · BUYERS & RENTERS

What the approval data means for buyers and renters

Australia's national approval rate of roughly 187,000 to 200,000 dwellings per year still falls short of the National Housing Accord target of approximately 240,000 per year.

The gap points to continuing supply pressure in most major markets, with NSW and Victoria needing to close the shortfall significantly to meet the 2029 milestone.

Approvals lead construction by roughly 12 to 18 months for houses and longer for multi-unit projects. The current approval pattern points to where new supply will be concentrated over the next two years.

The National Housing Accord target tracker covers the full shortfall in detail. For context on how long approved homes actually take to build, see building times by state.

General information only. This article is based on publicly available ABS data. It does not constitute financial or investment advice. If you are making property or investment decisions, consider speaking with a licensed financial adviser.

ABS Building Approvals, Australia, March 2026

ABS Regional Population, 2024–25

ABS Australian Statistical Geography Standard (ASGS), Edition 3

NHSAC Quarterly Progress Report, March 2026

Australian Treasury: National Housing Accord

Chart Snapshots