Build-to-rent statistics in Australia 2026

Australia's build-to-rent sector is expanding quickly, with market-source estimates counting 12,000 operational apartments as at October 2025 and 4,660 units delivered in 2024 alone. The national pipeline is estimated at between 51,000 and 63,500 apartments, depending on which development stages are counted. Victoria holds the largest share of total stock, and New South Wales recorded the largest pipeline increase of any state over the past 12 months.

National pipeline (Property Council / BDO)

51,000

Apartments worth $40.1 billion, May 2026

Units delivered in 2024

4,660

Across 18 schemes nationally; a record at that point

DA-approved, not yet started

20,500

Approved apartments waiting to convert to construction starts

Why is housing construction falling short of targets?

Feasibility, financing and construction capacity constraints may be delaying some approved BTR projects.

Read full article →Is Australia on track to build 1.2 million homes by June 2029?

BTR is one delivery channel within the National Housing Accord.

Read full article →SECTION 01 · DEFINITIONS

What is build-to-rent in Australia?

Build-to-rent is a model where an entire apartment building is constructed specifically for long-term rental, owned by a single entity, and professionally managed as one asset.

For Commonwealth tax purposes, build-to-rent is defined by ownership structure. Under Commonwealth tax legislation that commenced on 1 January 2025, a development must meet five conditions to qualify:

- At least 50 dwellings

- All dwellings and common areas owned by a single entity

- Dwellings available for residential leasing to the public

- At least 10% of dwellings designated as affordable dwellings

- The development must enter a 15-year build-to-rent compliance period

SECTION 02 · PIPELINE SIZE

How many build-to-rent apartments are in Australia's pipeline?

Australia's build-to-rent pipeline is growing, but the total depends on whether early-stage, approved, under-construction and operational projects are counted together.

Published pipeline estimates range from 51,000 to 63,500 apartments, depending on which development stages are included and when each count was taken. These figures are market-source estimates and are not directly comparable.

Three published pipeline totals: scope and reference date

Property Council / BDO

51,000

May 2026

Single total; no national stage-by-stage breakdown. Tracks year-on-year pipeline value alongside unit count.

Knight Frank

60,000

Q4 2024, published Feb 2025

Two-stage split: delivered or under construction versus planned, including pre-DA projects.

JLL

63,500

October 2025

Combined total from four reported stages: operational, under construction, approved and in planning.

Property Council of Australia / BDO: 51,000 apartments, May 2026

The national BTR pipeline reached 51,000 apartments worth $40.1 billion in May 2026, up from 39,300 apartments and $30.1 billion a year earlier. This is the most recent of the three pipeline readings and the only one with a 2026 reference date. It does not include a national stage-by-stage breakdown.

Pipeline, May 2026

51,000

Apartments nationally; valued at $40.1 billion

Year-on-year increase

+11,700

Up from 39,300 a year earlier; a 29.8% increase in units and 33.2% in value

Knight Frank: nearly 60,000 units, Q4 2024

As of Q4 2024, 19,308 units had been delivered or were under construction since 2018, with a further 40,191 units planned, for a combined total of just under 60,000 units. The planned category includes early-concept projects not yet DA-approved, which helps explain why this total is higher than counts limited to approved or construction-ready projects.

Delivered or under construction since 2018

19,308

Units on site or completed

Planned units (including pre-DA)

40,191

Not yet started; some without DA approval at time of count

JLL: 63,500 units across four reported stages, October 2025

JLL's October 2025 figures listed 12,000 operational units, 3,600 under construction, 23,600 approved and 24,300 in planning. Together, these categories total 63,500 units.

Australia's build-to-rent pipeline by development stage, October 2025

Of the 63,500 units counted across the four stages, 15,600 were operational or under construction. The remaining 47,900 units were approved but not yet started or still in planning.

Operational

12,000

19% of total; tenanted and operating

Under construction

3,600

6% of total; on site now

Approved

23,600

37% of total; DA granted, not yet started

In planning

24,300

38% of total; concept or early stage

Source: JLL Australia, Australia's Living Sector: Growth, Resilience and Capital Attraction, October 2025.

The 23,600 approved-but-not-started units have cleared the planning stage, but construction has not yet begun. The 24,300 units still in planning had not yet reached approval or construction. Together, these two groups account for three in every four units in JLL's count.

SECTION 03 · DELIVERIES AND GROWTH

How fast is build-to-rent growing in Australia?

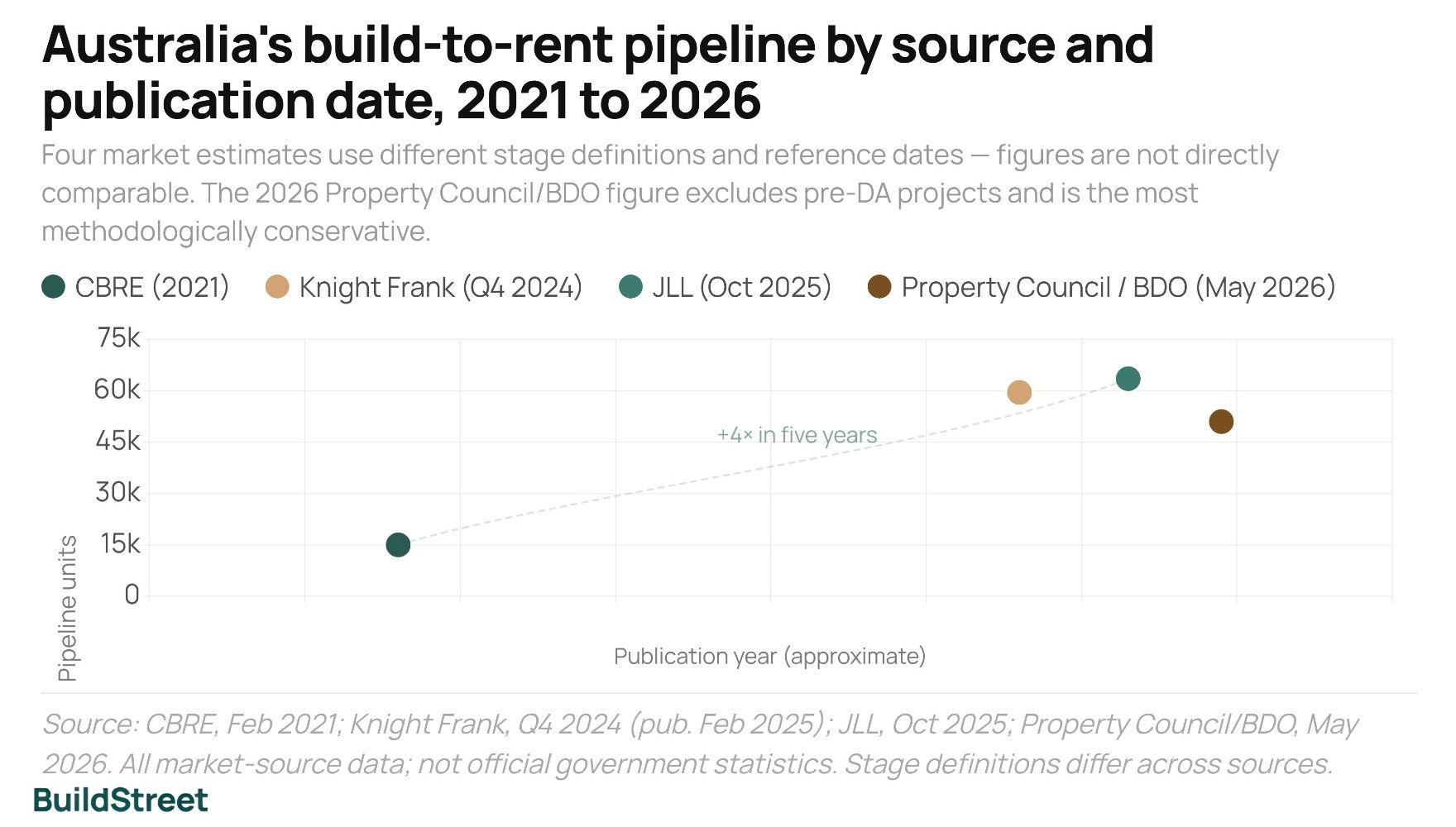

The national BTR pipeline grew from approximately 15,000 units across 40 projects in 2021 to between 51,000 and 63,500 units by 2025–26, depending on the source. Annual deliveries reached a record 4,660 units in 2024, with 6,000 forecast for 2025.

Australia's build-to-rent pipeline size by source and publication date, 2021–2026

Each data point uses a different stage definition and reference date; figures are not directly comparable.

Source: CBRE Feb 2021; Knight Frank Q4 2024 (published Feb 2025); JLL Oct 2025; Property Council/BDO May 2026. All figures are market-source data.

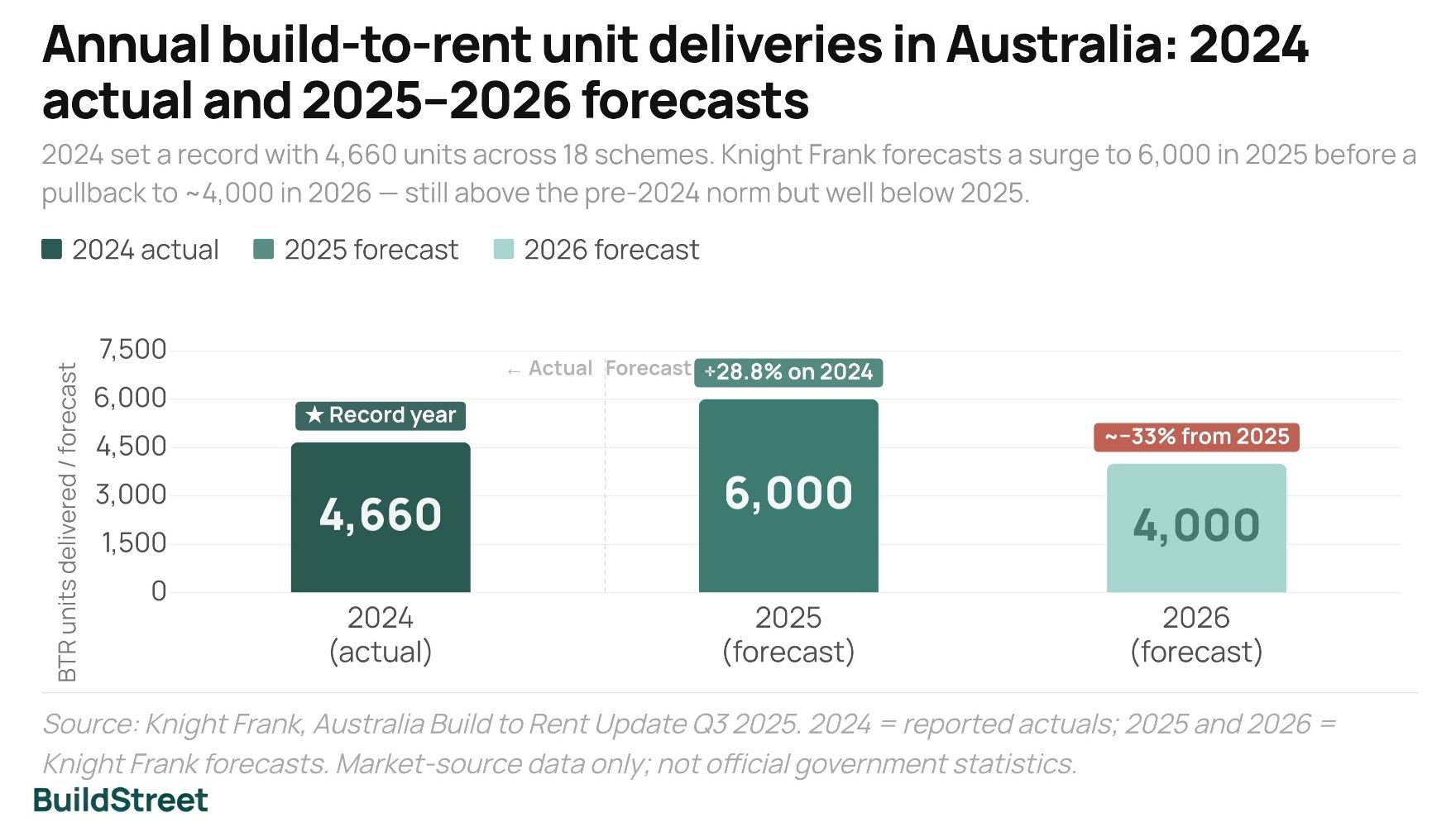

Build-to-rent deliveries reached 4,660 units in 2024

Knight Frank records the following annual BTR delivery figures for Australia:

- 4,660 units delivered across 18 schemes in 2024, the highest annual figure recorded to that date

- Four schemes opened in the first half of 2025, adding 1,298 units before mid-year

- Full-year 2025 forecast: 6,000 units, up 28.8% on the 2024 actual

- Full-year 2026 forecast: around 4,000 units, down approximately 33% from the 2025 forecast

Knight Frank forecasts a delivery dip in 2026, with full-year completions expected to fall from 6,000 units in 2025 to around 4,000 units in 2026. At 4,000 units, 2026 deliveries would sit about 14% below the 2024 actual, despite a pipeline that has grown in total unit count.

Annual build-to-rent unit deliveries in Australia: 2024 actual and 2025–2026 forecasts

2024 figure is reported actuals. 2025 and 2026 are Knight Frank forecasts. About 20,500 DA-approved units had not started construction at Q3 2025.

Source: Knight Frank, Australia Build to Rent Update Q3 2025. Market-source data.

Approval-to-construction gap

Around 20,500 units held DA approval but had not started construction as at Q3 2025. Knight Frank identifies feasibility, financing and construction capacity as constraints for the sector, rather than planning approval alone.

SECTION 04 · LOCATIONS

Where is build-to-rent being built in Australia?

Victoria held the largest share of the national BTR pipeline at Q4 2024, with 25,538 units in total. New South Wales had overtaken Queensland for second place at Q4 2024, recording 15,089 units against Queensland's 14,390. The remaining states each had fewer than 2,000 units: ACT (1,723), WA (1,568) and SA (1,191).

Build-to-rent pipeline by state in Australia, Q4 2024

Completed or under-construction units shown against planned units. ACT (1,723), WA (1,568) and SA (1,191) excluded due to limited stage-level data.

Source: Knight Frank, Australia Build to Rent Update Q4 2024, published February 2025.

Melbourne also had the most completed BTR deliveries nationally by mid-2025, while Brisbane recorded two openings in the first half of 2025. NSW planning zone changes that took effect in 2023 permit BTR wherever residential flat buildings or shop-top housing are allowed. Knight Frank forecasts Sydney will account for a larger share of new completions from 2025 onward, after those planning changes. At project level, delivery has concentrated in inner-city and near-CBD precincts, including Brunswick, Footscray, Newstead, Parramatta and Docklands.

Three cities hold most operational and under-construction BTR stock

Melbourne, Sydney and Brisbane held the largest share of operational and under-construction build-to-rent stock nationally at Q4 2024. Knight Frank forecasts Sydney will account for a larger share of new completions from 2025 onward, after NSW planning zone changes in 2023 broadened permissible build-to-rent locations.

Victoria

25,538

Pipeline units, Q4 2024

New South Wales

15,089

Pipeline units, Q4 2024

Queensland

14,390

Pipeline units, Q4 2024

ACT

1,723

Pipeline units, Q4 2024

WA

1,568

Pipeline units, Q4 2024

SA

1,191

Pipeline units, Q4 2024

SECTION 05 · INVESTORS AND DEVELOPERS

Who is building build-to-rent projects in Australia?

Offshore institutional capital accounted for approximately 57% of the national BTR pipeline in 2021, according to CBRE's February 2021 pipeline report. By 2024–25, project examples showed a broader mix of capital sources, including:

- Joint ventures between Australian listed developers and offshore institutional investors

- Domestic superannuation-aligned investors

- Offshore pension funds from North America, Europe and Asia

- Specialist living-sector platforms backed by large institutional capital pools

Brunswick, VIC

Footscray, VIC

Parramatta, NSW

Docklands, VIC

South Brisbane & Fortitude Valley, QLD

Source: Knight Frank, Australia Build to Rent Update Q3 2025. Selected examples only.

Other capital activity recorded in 2024–25 included:

- Pembroke entering the sector through a site purchase in Fitzroy

- Scape securing a $700 million equity commitment from South Korea's National Pension Service

- Australian Ethical backing Cedar Pacific's Quay Street project in Brisbane, alongside Grosvenor, Moata Ventures and Sumitomo Forestry

SECTION 06 · POLICY SETTINGS

Tax and planning settings for build-to-rent in Australia

A federal tax framework took effect on 1 January 2025, offering two concessions to qualifying BTR developments:

- A capital works deduction of 4%, up from the standard 2.5%

- A managed investment trust withholding tax rate of 15% for eligible foreign investors from information-exchange countries, down from 30%

NSW, Victoria, Queensland and South Australia each have published BTR land-tax concessions. All four use land-tax relief as their primary state-level instrument. No official national dataset shows how many projects have claimed these concessions or how many state tax reliefs have been granted.

Commonwealth · From 1 January 2025

Federal tax concessions

- 4% capital works deduction (up from 2.5%)

- 15% MIT withholding tax for eligible foreign investors (down from 30%)

- Requires 50+ dwellings, single ownership

- Requires 10% affordable dwellings over 15 years

- Affordable dwellings capped at 74.9% of market rent

New South Wales

NSW concessions

- 50% reduction in land value for land tax

- Exemptions from surcharge purchaser duty and surcharge land tax

- BTR permissible in residential flat building and shop-top housing zones

- State-significant development pathway for larger schemes

- No subdivision for 15 years in most relevant zones

Victoria

VIC concessions

- Land tax calculated on 50% of taxable land value

- Exemption from absentee owner surcharge

- Benefits available for up to 30 years

Queensland

QLD concessions

- 50% discount on taxable value for land tax

- Foreign surcharge land tax does not apply

- Additional foreign acquirer duty concession (can reduce to nil)

- Available for up to 20 years or until 30 June 2050

South Australia

SA concession

- 50% reduction in site value for eligible BTR land from 2023–24 up to and including 2039–40

Source: Treasury Laws Amendment (Responsible Buy Now Pay Later and Other Measures) Act 2024, Schedule 1; ATO; Revenue NSW; SRO Victoria; QRO; RevenueSA; NSW Planning.

SECTION 07 · RENTAL SUPPLY

How does build-to-rent contribute to Australia's rental supply?

The 2021 Census recorded that 30.6% of occupied private dwellings were rented, across 10.85 million private dwellings nationally. Annual rent growth was 3.5% in the year to April 2026, down from 3.7% in March 2026. For longer-term context, ABS reported annual rent growth of 7.6% in the September quarter of 2023.

BTR's structural contribution to rental supply is that dwellings remain in the rental pool under single ownership rather than being sold individually. This is one reason BTR is treated separately in federal and state policy settings. Treasury's National Housing Accord targets 1.2 million new homes over five years from mid-2024. The ABS does not identify build-to-rent as a separate category in its tenure classifications, so BTR's share of rental stock or its effect on vacancy rates cannot be stated from official data.

Private dwellings rented (2021 Census)

30.6%

Share of all occupied private dwellings

Rent increase, year to April 2026

3.5%

ABS CPI rents series; down from 3.7% in March 2026. ABS reported 7.6% in Sep qtr 2023.

BTR units delivered in 2024

4,660

Delivered as rental stock; 6,000 forecast for 2025

Annual rent change in Australia, year-ended quarterly, September 2021 to March 2026

BTR deliveries are not separately identified in the ABS CPI rental series. Figures reflect broader market rental price changes.

Source: ABS, Consumer Price Index, Australia, rent component, year-ended change.

Data gap: build-to-rent rents versus private market rents

No official Australian source publishes a national comparison of build-to-rent (BTR) asking rents versus equivalent private-market rents. Project-level listing data exists, but differences in location, building age, amenities, lease terms and furnished or unfurnished status make direct comparisons unreliable. No matched, city-level BTR-versus-private-rental comparison is available from the sources reviewed.

General information only

The data on this page is drawn from publicly available sources including Commonwealth legislation, ABS statistical releases, Treasury, state revenue authorities, NSW Planning and market-source reports. It is general information only and does not constitute financial, investment or legal advice. Market-source pipeline figures are not methodologically identical and should not be treated as interchangeable.

Australian Taxation Office: Build to rent development tax incentives

Federal Register of Legislation, Treasury Laws Amendment (Responsible Buy Now Pay Later and Other Measures) Act 2024

Treasury, Delivering the National Housing Accord

ABS, Consumer Price Index, Australia, April 2026

ABS, Consumer Price Index, Australia, September Quarter 2023

ABS, Housing: Census, 2021

NSW Planning: Build-to-rent housing

Revenue NSW: Build to rent ruling

SRO Victoria: Discount for build-to-rent developments

Queensland Revenue Office, Build-to-rent concessions

RevenueSA, Tax concessions to promote new housing opportunities

BDO – 2026 Build to Rent report

Property Council of Australia: Build-to-rent hits $40bn as Sydney drives next phase of growth

Knight Frank Australia, Australian Build to Rent Update Q4 2024

Knight Frank Australia, Australian Build to Rent Update Q3 2025

JLL Australia, Australia's Living Sector: Growth, Resilience and Capital Attraction

CBRE Australia, Australia ViewPoint: Build-to-Rent Development Pipeline 2021

Chart Snapshots