How many social and affordable homes are built in Australia each year?

Australia had 450,607 social housing dwellings at 30 June 2025, spanning all four programme types: public housing, community housing, state-owned and managed Indigenous housing (SOMIH) and Indigenous community housing (ICH).

The social housing share was 4.1% of all Australian households in 2024, the latest year for which national data is available, down from 4.7% in 2008. By 30 June 2025, the public housing waitlist had increased to 189,536 households.

Governments have responded with new supply programmes, including the $10 billion Housing Australia Future Fund (HAFF) and National Housing Accord Facility (NHAF), which target 40,000 social and affordable homes over five years. Rounds 1 and 2 had contracted 18,650 homes, and Round 3 was opened to support the remaining 21,350 homes.

Total social housing dwellings

450,607

Community housing has driven most of the growth since 2005; public housing remains the largest programme at 296,541 dwellings

Social share of all households

4.1%

Down from 4.7% in 2008; varies widely by state

Public housing waitlist

189,536

At 30 June 2025; 77,425 classified as greatest need

Australia does not publish one national annual count of every social and affordable home completed across all programmes. The best national proxy is net social housing stock change, not a pure build count. Social housing stock increased by about 2,800 net dwellings per year from 2019 to 2024, with little net change in 2024–25. Under HAFF and NHAF, Rounds 1 and 2 had contracted 18,650 homes toward the 40,000-home target. Research estimates suggest Australia's social housing shortfall starts at about 435,000 additional dwellings, depending on the definition used.

Emerging home types in Australia in 2026: modular, prefab, duplexes and the shift in how we build

Social and affordable housing targets are driving demand for faster, cheaper construction methods. How are new building types changing the supply landscape?

Read full article →Build-to-rent in Australia in 2026: pipeline, locations and how fast the sector is growing

Community housing providers and institutional investors are converging on build-to-rent. Where does the model fit in the social and affordable housing delivery system?

Read full article →Section 01 · Definitions

What is social housing in Australia?

Social housing is subsidised rental accommodation for people on very low incomes or people with high housing need. Rent is usually set as a proportion of household income rather than full market rent. Four programme types make up the system, and together they accounted for 4.1% of all Australian households in 2024, the most recent year for which AIHW social-share data is available.

What is the difference between social housing and affordable housing?

Social housing rent

25–30%

Social housing rent is commonly set at around 25% to 30% of household income, depending on the programme and jurisdiction. It is generally for people with the highest housing need, including people experiencing homelessness, family or domestic violence, disability, or very low income. Eligibility is based on income, household circumstances and housing need.

Affordable housing rent

Around 80%

Affordable housing rent is often set below market rent, commonly around 80% of local market rates, depending on the programme. It is generally aimed at low- to moderate-income households that may not qualify for social housing but cannot afford suitable market rental housing. Programmes such as HAFF and NHAF fund both social and affordable homes.

Section 02 · National stock

How much social housing does Australia have?

Australia had 450,607 social housing dwellings at 30 June 2025, across public housing, community housing, SOMIH and Indigenous community housing.

The largest programme was public housing, with 296,541 dwellings. Community housing accounted for 118,425 dwellings, SOMIH for 17,163 and Indigenous community housing for 18,478.

Public housing

296,541

At 30 June 2025; state-managed

Community housing

118,425

At 30 June 2025; CHP-managed

SOMIH

17,163

At 30 June 2025; state-managed Indigenous

Indigenous community housing

18,478

At 30 June 2025; community-managed Indigenous

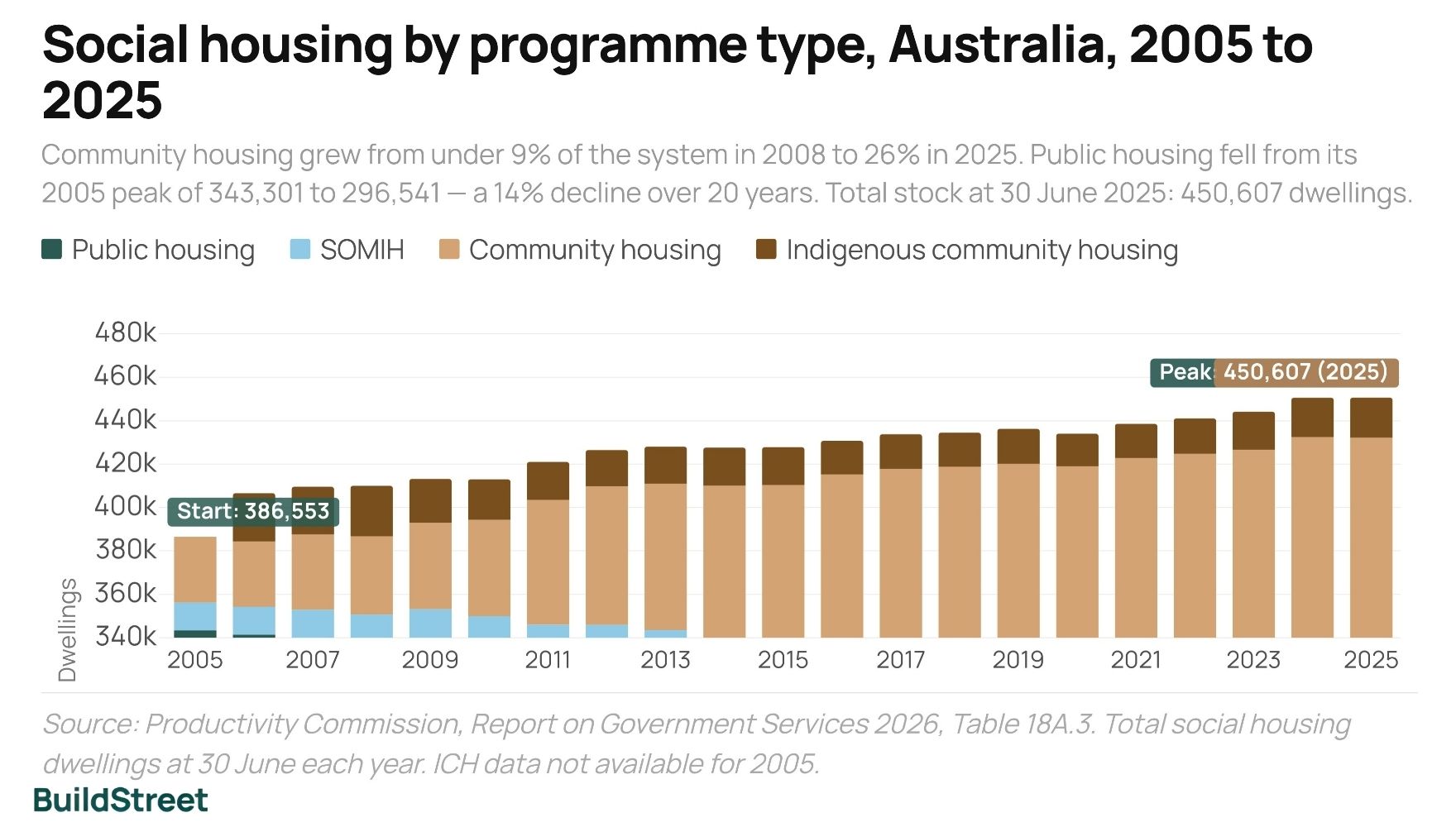

Social housing by programme type, Australia, 2005 to 2025

Community housing has grown from under 9% of the social housing system in 2008 to about 26% in 2025, while public housing's share has declined over the same period. All four programme series are shown to 30 June 2025.

Source: Total social housing dwellings at 30 June each year. All four programme series are drawn from the Productivity Commission’s Report on Government Services 2026 housing data tables and shown through to 30 June 2025. Source: Productivity Commission, Report on Government Services 2026, Table 18A.3.

Between 2008 and 2024, social housing stock increased by about 40,000 dwellings. Most of that growth came from community housing, while public housing declined from its 2005 peak of more than 343,000 dwellings.

Section 03 · Annual additions

How many social and affordable homes are built each year in Australia?

Net social housing stock grew by roughly 2,800 dwellings per year between 2019 and 2024. Australia does not publish a single annual count of all social and affordable housing completions across programmes, so net stock change is the best available national proxy.

Estimated net social housing dwellings added per year, 2019 to 2024

Total social housing stock grew by about 14,000 dwellings between 2019 and 2024, averaging roughly 2,800 per year. This net figure combines new builds and acquisitions minus removals, demolitions, and transfers out of the system.

The HAFF and NHAF programmes are designed to increase delivery from this historical pace. If the full 40,000-home five-year target is met, that would work out to roughly 8,000 additions per year. Rounds 1 and 2 had contracted 18,650 homes toward that target.

Section 04 · Long-term trend

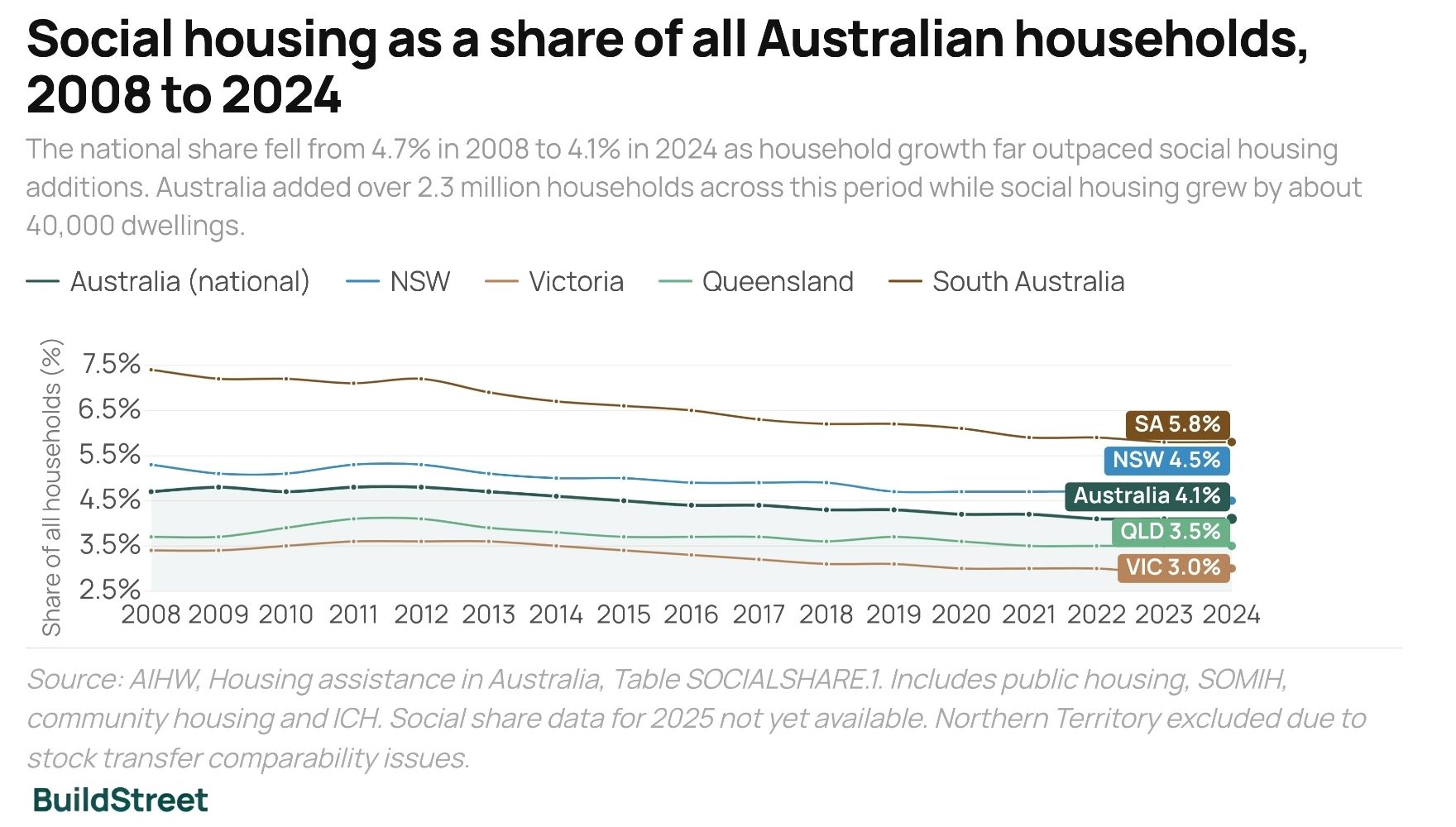

Australia's social housing share has fallen since 2008

Social housing as a share of all Australian households (2024)

Down from 4.7% in 2008, with a peak of 4.8% reached in 2009 and again in 2011 and 2012. The Northern Territory share is 14.4%; Victoria is 3.0%.

Social housing has not kept pace with growth in Australian households. Although the number of social housing dwellings increased between 2008 and 2024, total households grew much faster. As a result, social housing made up a smaller share of all households in 2024 than it did in 2008.

Between 2008 and 2024, Australia added more than 2.3 million households while social housing dwellings grew by about 40,000. The national social housing share fell from 4.7% to 4.1%.

The fall was widespread, affecting most states and territories:

- ACT: 8.6% to 6.5% (down 2.1 percentage points, the steepest fall)

- South Australia: 7.4% to 5.8% (down 1.6 percentage points)

- NSW: 5.3% to 4.5% · WA: 4.3% to 3.8% · Victoria: 3.4% to 3.0%

- Tasmania was broadly stable, moving from 6.1% to 6.2%

- NT: AIHW notes that Northern Territory data are affected by stock transfers, meaning 2024 data are most comparable with 2018 rather than earlier years. The NT social housing share was 14.6% in 2018 and 14.4% in 2024, so the apparent rise from 7.6% in 2008 should not be read as a like-for-like increase in housing provision.

Social housing as a share of all Australian households, 2008 to 2024 (latest AIHW)

Social housing households as a percentage of all Australian households at 30 June each year. Includes public housing, SOMIH, community housing, and Indigenous community housing (ICH). Source: AIHW, Housing assistance in Australia, Table SOCIALSHARE.1. Social share data for 2025 is not yet available from AIHW.

Section 05 · Government programmes

Major social and affordable housing programmes in Australia

State and territory governments spent $10.8 billion on social housing in 2024–25, made up of $5.9 billion in operational costs and $4.9 billion in capital works. Since 2023, the Commonwealth has also committed several major supply programmes, each at a different stage of delivery.

Housing Australia Future Fund and NHAF: delivery pipeline

Progress toward the 40,000-home five-year target, using Housing Australia Rounds 1 and 2 contract data and the Round 3 announcement.

Programme target

40,000

20,000 social + 20,000 affordable over five years

Contracted (Rounds 1 + 2)

18,650

279 projects; 46.6% of five-year target

Under construction

9,501

Among contracted projects

Completed

889

Finished and tenantable, reported in the HAFF Round 3 announcement

Source: Housing Australia, HAFF/NHAF Rounds 1 and 2 contract update, 3 July 2025; Housing Australia, HAFF Round 3 call for submissions, 30 January 2026.

$2 billion

One-off Commonwealth payment announced in 2023. The programme is now expected to deliver 4,251 new social homes, exceeding the original target of about 4,000.

$9.3 billion

Five-year Commonwealth/state agreement from 2024. Around $1.8 billion per year for operations and homelessness services. The agreement mainly funds social housing operations and homelessness services, rather than a separate new-build target.

1.2 million homes

Five-year total housing target (mid-2024 to mid-2029). The NHSAC estimated that around 938,000 homes would be completed by June 2029, leaving a projected shortfall of about 262,000 homes against the target.

$4 billion

10-year Commonwealth/NT agreement. Targeting up to 2,700 new homes in Aboriginal communities and upgrades to existing housing, to reduce overcrowding in remote areas.

Section 06 · Estimated shortfall

How much more social housing does Australia need?

The 189,536-household public housing waitlist at 30 June 2025 includes only registered applicants. Broader research estimates suggest the wider social and affordable housing gap is larger, although the main estimates measure different forms of need and are not directly comparable.

AHURI shortfall estimate (2023)

435,000

Shortfall for the lowest-income quintile. Extends to over 600,000 when including the next-lowest quintile.

UNSW City Futures / CHIA: unmet need (2021)

640,000+

Unmet need at the 2021 Census: homelessness, overcrowding, or severe rental stress. Projected to exceed 940,000 households by 2041.

AHURI cumulative need 2016 to 2036

727,300

Cumulative 2016–2036 need. Manifest unmet need: 46,600; evident need: 386,800; plus projected demand through 2036.

None of these figures should be treated as an official government target. The 435,000 estimate covers only the lowest-income quintile; the 640,000+ figure draws on a broader range of households from the 2021 Census; and the 727,300 figure is a cumulative 20-year projection, not a current point-in-time shortfall.

At the historical pace of about 2,800 net social housing additions per year, each estimate would imply a multi-decade delivery gap unless net additions increased substantially.

How well does public housing stock match household need?

The waitlist shows unmet demand from outside the system. But even within existing social housing, dwelling size and household need do not always align.

Nationally, 4.3% of public housing households, or about 12,300 households, were overcrowded at 30 June 2025. A larger share, 16.7%, or about 47,600 households, were living in dwellings larger than they required. This means the underutilised public housing pool was about 3.9 times the size of the overcrowded pool.

- South Australia has the highest underutilisation rate: 24.4%

- The Northern Territory has the highest overcrowding rate: 8.8%

Underutilisation typically reflects long-term tenants who remain in family-sized homes after their household has shrunk. Relocating established tenants to smaller dwellings requires suitable alternative properties nearby and may affect established community connections.

Overcrowding and underutilisation in public housing by state and territory, Australia, 2025

In most jurisdictions, underutilised dwellings (orange) far outnumber overcrowded ones. The Northern Territory is the exception: overcrowding at 8.8% is higher than the underutilisation rate of 7.5%, reflecting the concentration of large households in remote communities.

Suitability is measured using the Canadian National Occupancy Standard. Overcrowded households need more bedrooms than are available; underutilised households need fewer. Source: Productivity Commission, Report on Government Services 2026, Tables 18A.32 and 18A.39.

Section 07 · Demand and waiting

How many households are waiting for public housing in Australia?

Households on the public housing waitlist (30 June 2025)

Of these, 77,425 households, or 40.8%, were classified as greatest need: homeless households, households at risk of homelessness, or households living in housing that was inappropriate to their circumstances. A further 17,478 households were on the SOMIH waitlist for state-managed Indigenous housing.

The public housing waitlist has grown since 2018, when it stood at 140,578 households. By 2025 it had reached 189,536, an increase of about 49,000 households over seven years. The largest growth was in the greatest-need category, which rose from 45,828 in 2018 to 77,425 in 2025, an increase of nearly 69%.

Victoria has the largest count of greatest-need households on the waitlist at 24,803, even though it has one of the lower social housing shares in the country. Queensland follows closely at 24,024, then NSW at 9,906. Differences between states partly reflect how each jurisdiction defines and classifies greatest need. From 2024–25, the national greatest-need standard was amended, making the figures for that year not directly comparable with prior years for some jurisdictions.

In 2024–25, 16,016 households were newly allocated to public housing nationally, with 13,471 households, or 84.1%, classified as greatest need. As a simple scale comparison, the current waitlist is about 12 times the number of public housing allocations made in 2024–25. This is not a forecast of waiting time, because new applications, exits, eligibility rules and priority systems change over time.

Public housing waitlist, Australia, 2014 to 2025

The waitlist rose by nearly 21,000 households in 2024–25 alone, the largest single-year increase in the series. The greatest-need segment (red) more than doubled from 2018 to 2025.

Methodology: Public housing waitlist only; excludes households requesting a transfer. Greatest-need definition changed in 2024–25, and figures are not directly comparable with prior years for NSW, Vic, and WA. Source: Productivity Commission, Report on Government Services 2026, Table 18A.29.

Section 08 · State comparison

How do Australian states and territories compare on social housing?

NSW had the most social housing by volume, with 157,171 dwellings at 30 June 2025, but the Northern Territory had the highest share at 14.4% of all households, based on the latest AIHW data for 2024. Victoria had the lowest share at 3.0%, followed by Queensland at 3.5%. State totals in the table below reflect all four programme types at 30 June 2025.

Composition also varies. About 66% of Tasmania's social housing stock was community-managed, the highest proportion of any state or territory. The ACT and NT relied most heavily on government-owned stock. The NT's high share reflects Indigenous housing programmes concentrated in remote communities.

Social housing dwellings by state and territory, Australia, at 30 June 2025

All programme types at 30 June 2025 (ROGS 2026, Table 18A.3).

Source: Productivity Commission, Report on Government Services 2026, Table 18A.3 (all programme types at 30 June 2025). Social share tab: AIHW, Table SOCIALSHARE.1 (30 June 2024 data).

State and territory comparison: stock, demand and share

| State / territory | Public | Community | Indigenous | Total | Share | 2008 | Waitlist | Greatest need |

|---|---|---|---|---|---|---|---|---|

| New South Wales | 92,709 | 52,439 | 12,023 | 157,171 | 4.5% | 5.3% | 59,077 | 9,906 |

| Victoria | 64,277 | 19,625 | 2,146 | 86,048 | 3.0% | 3.4% | 56,230 | 24,803 |

| Queensland | 53,727 | 13,158 | 8,697 | 75,582 | 3.5% | 3.7% | 24,112 | 24,024 |

| Western Australia | 33,940 | 7,611 | 2,687 | 44,238 | 3.8% | 4.3% | 22,409 | 7,382 |

| South Australia | 31,611 | 13,010 | 2,057 | 46,678 | 5.8% | 7.4% | 13,687 | 3,021 |

| Tasmania | 5,051 | 10,430 | 258 | 15,739 | 6.2% | 6.1% | 5,152 | 4,124 |

| ACT | 11,097 | 1,246 | – | 12,343 | 6.5% | 8.6% | 3,402 | 1,925 |

| Northern Territory | 4,129 | 906 | 7,773 | 12,808 | 14.4% | 7.6% | 5,467 | 2,240 |

| Australia total | 296,541 | 118,425 | 35,641 | 450,607 | 4.1% | 4.7% | 189,536 | 77,425 |

Source: Productivity Commission, Report on Government Services 2026, Tables 18A.3 and 18A.29 (all stock programme types and waitlist at 30 June 2025); AIHW, Housing assistance in Australia 2025, Table SOCIALSHARE.1 (social share at 30 June 2024, latest available). Public housing waitlist excludes transfer applicants. Greatest-need definition changed in 2024–25; waitlist figures for that year are not directly comparable with prior years for NSW, Vic and WA.

Section 09 · Delivery model

Community housing providers now manage more than a quarter of Australia's social housing

Community housing providers (CHPs) managed 26.3% of all social housing at 30 June 2025, up from 7.9% in 2005. Over the same period, public housing's share of the system fell from 88.8% to 65.8%.

CHPs can access Commonwealth Rent Assistance through eligible tenants, a revenue stream not available to direct government landlords, and can draw on private funding more flexibly. Most HAFF and NHAF funding is channelled through CHPs, so the sector's share may grow as those programmes deliver.

Public housing and community housing share of all social housing, Australia, 2005 to 2025

Public housing held nearly 89% of all social housing in 2005. By 2025 that share had fallen to 65.8%, with community housing growing from under 8% to 26.3% over the same period.

Source: AIHW, Housing assistance in Australia 2025; Productivity Commission, Report on Government Services 2026, Table 18A.3.

NSW had the largest community housing portfolio nationally, with 52,439 tenancy units, followed by Victoria, with 19,625, and South Australia, with 13,010. Tasmania had the highest community housing share of any state or territory at about 66% of its total social housing stock. The ACT and NT relied most heavily on government-owned stock.

Scale of the community housing sector

More than 400 community housing organisations reported nationally at 30 June 2024. Nearly half managed fewer than 20 dwellings each. A smaller group of large providers managed portfolios of 200 or more dwellings and accounted for most of the sector's stock. Large providers are taking on increasing responsibility for new supply delivery through HAFF and related programmes.

Section 10 · Frequently asked questions

Frequently asked questions

Australia had 450,607 social housing dwellings at 30 June 2025. This total covers public housing (296,541), community housing (118,425), SOMIH (17,163) and Indigenous community housing (18,478).

General information only

This article draws on publicly available data from the AIHW, the Productivity Commission, and Housing Australia. It is general information only and does not constitute financial, investment or legal advice. Most stock, waitlist and programme figures are sourced from official Australian government data releases. Research-based shortfall estimates are drawn from AHURI and UNSW City Futures modelling and may change as new data becomes available.

Productivity Commission, Report on Government Services 2026, Part G Section 18 Housing data tables (June 2026 release)

Australian Institute of Health and Welfare (AIHW), Housing assistance in Australia 2025

Housing Australia Future Fund Facility and National Housing Accord Facility updates, including Rounds 1 and 2 contract update, 3 July 2025, and Round 3 call for submissions, 30 January 2026

Treasury, Social Housing Accelerator progress reporting

National Housing Supply and Affordability Council, State of the Housing System 2026

OECD Affordable Housing Database, PH4.2 Social Rental Housing Stock, 2023 QuASH

Australian Housing and Urban Research Institute (AHURI), Final Report 452, Australia's multi-provider social housing system, 2026; Final Report 306, Social housing as infrastructure, 2018

UNSW City Futures Research Centre / CHIA, Quantifying Australia's unmet housing need: a national snapshot.

Chart Snapshots