Northern Territory housing supply: what's driving development in Darwin?

Northern Territory dwelling approvals reached 823 in 2025, up 59% from 518 in 2024 and 69% above the 2023 low of 486. Despite the recovery in approvals, dwelling completions remained weak. The NT completed 408 dwellings in FY2024–25, down 83% from the FY2014–15 peak of 2,385.

Darwin accounts for most residential building activity in the Territory, but NT housing supply data is affected by factors that are less prominent in larger states. These include remote community housing programmes, a relatively high public sector share of housing approvals, and population growth that combines overseas migration gains with net losses to other states.

CY2025 total approvals

823

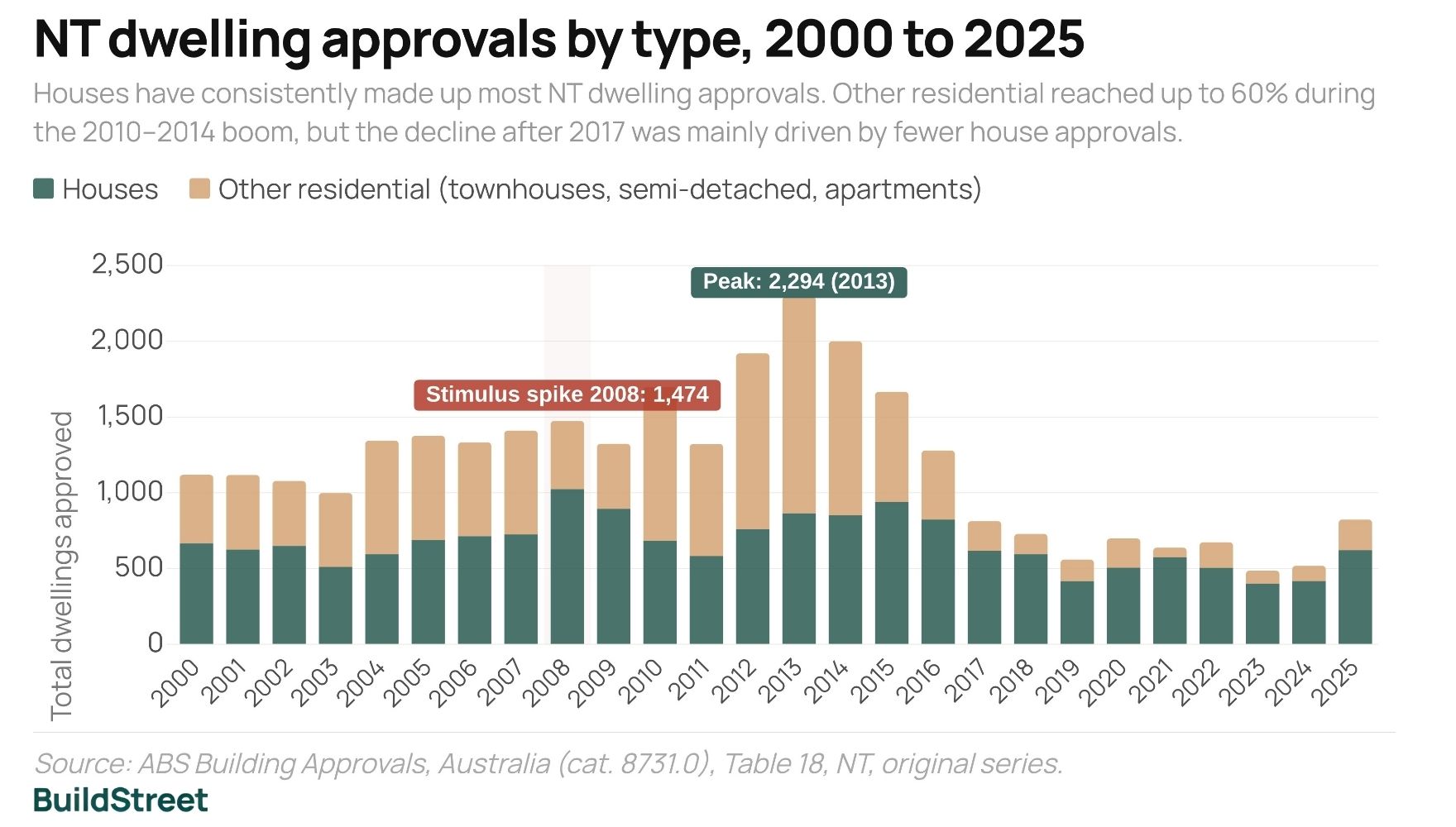

Up 59% from 518 in 2024; still 64% below the 2,294 recorded in 2013

FY2024–25 completions

408

Down 83% from the FY2014–15 peak of 2,385; completions fell for the second consecutive year.

NT population growth 2024–25

+3,672

Up 1.4%; net internal migration was negative at −2,105, with more residents leaving for other states than arriving

SECTION 01 · WHAT IS BEING BUILT

What types of homes are being approved in the NT?

NT dwelling approvals reached 823 in 2025, up 59% from 518 the year before and the strongest annual total since 2016. That recovery is real, but approvals are still 64% below the 2013 peak of 2,294, a year that reflected major Commonwealth investment in remote and urban housing.

Houses make up the clear majority of what gets built. In FY2024–25, 76.7% of new residential dwelling approvals were for detached houses, with 533 houses out of 695 dwellings in the ABS dwelling-type breakdown. Townhouses and semi-detached dwellings accounted for 19.3%, while apartments accounted for 4.0%.

Higher-density activity was concentrated in two areas: Darwin City suburb, with 24 apartment and medium-density approval applications, and the Palmerston townhouse corridors of Bakewell and Durack–Marlow Lagoon, with 22 combined. Litchfield recorded no non-house approval applications in FY2024–25.

Approved residential values totalled $381.8 million for FY2024–25. April 2026 alone recorded $50.0 million, the highest monthly figure since March 2021, and coincided with 110 total dwelling approvals, the strongest monthly count in over five years.

NT new residential approvals by dwelling type, FY2024–25

Source: ABS Building Approvals (cat. 8731.0), Table 28, NT new residential dwellings by type. FY2024–25, original series.

NT dwelling approvals by type, 2000 to 2025

Houses have consistently made up most NT dwelling approvals. Other residential dwellings reached up to 60% during the 2010 to 2014 boom, but the decline after 2017 was mainly driven by fewer house approvals.

Note: Dwelling-type breakdown derived from ABS Table 18, using total dwelling approvals minus house approvals. Source: ABS Building Approvals (cat. 8731.0), Table 18, NT, original series.

SECTION 02 · HOUSING TARGETS

NT housing targets: how far behind is the Territory?

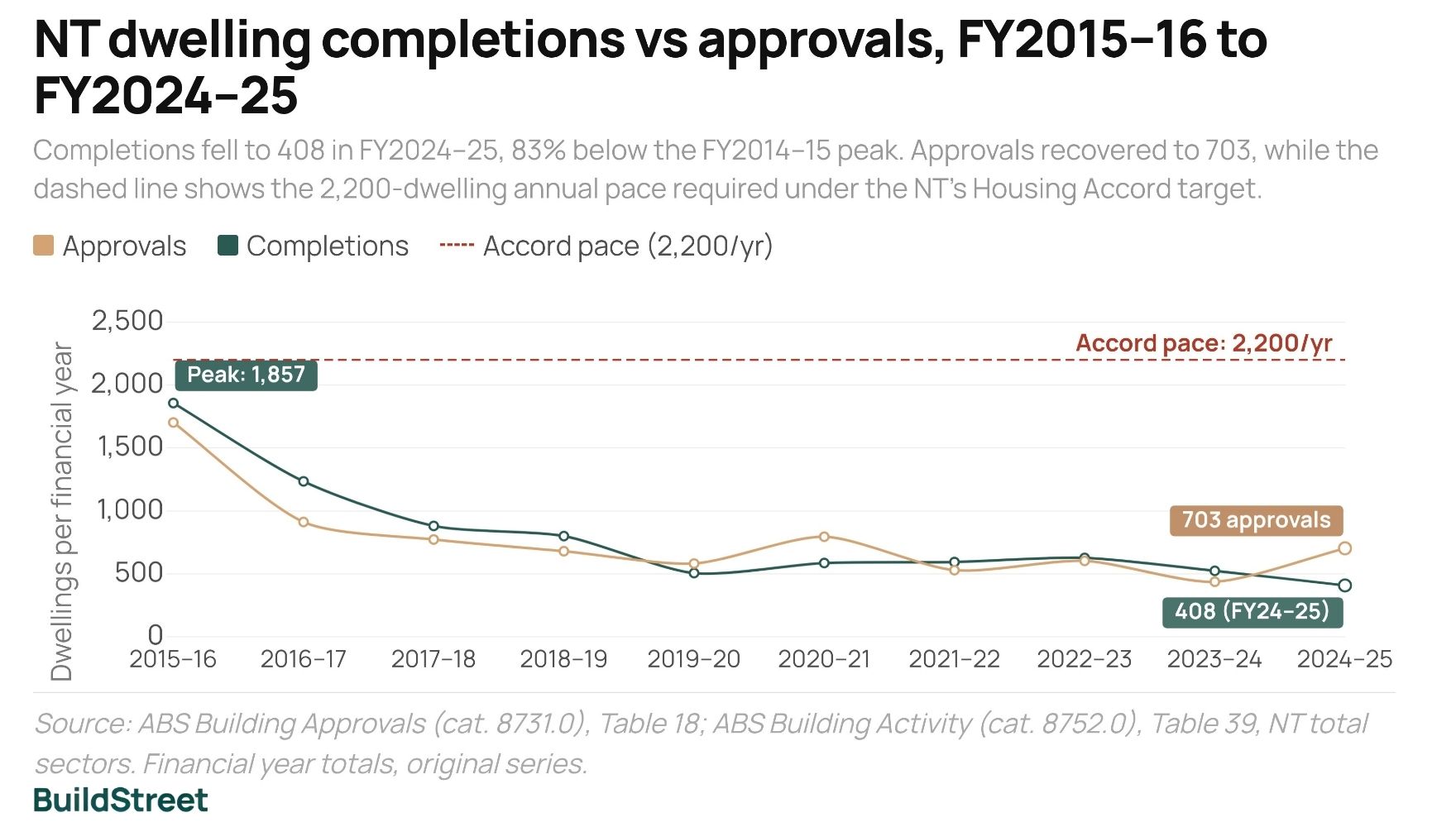

The NT completed 408 dwellings in FY2024–25, equal to roughly 19% of the 2,200 homes per year required to meet its National Housing Accord share of 11,000 homes by June 2029. NT dwelling approvals reached 703 in FY2024–25, but approvals do not always convert to completions within the same period.

On the current NHSAC outlook, the NT is expected to deliver around 4,000 homes across the five Accord years, equal to about 34% of its target. It is not projected to meet its share before 2034, which is the latest estimated completion date of any state or territory in the outlook.

The Territory's small housing market makes annual figures more volatile than in larger states. In a small market, large public housing projects can have a noticeable effect on annual approval totals. The 2025 approvals recovery included a larger public sector component than most recent years.

NT Housing Accord progress

Cumulative progress against the target of 11,000 homes by June 2029, based on NHSAC early 2026 outlook.

Accord startJun 2029

Accord deadline

Jul 2024 – Dec 2025

Jul 2024 – Dec 2025

Expected target completion: after 2034

NHSAC estimates the NT will deliver around 4,000 homes across the five Accord years, approximately 34% of its 11,000-home target. The Territory built about 3,000 homes in the five years prior to the Accord. Even at improved rates, the NT is not expected to meet its share before 2034, the slowest projected outcome of any state or territory.

Notes: NT Accord target of 11,000 homes is based on NHSAC's population-share allocation. Completions cover July 2024 to December 2025 (ABS Building Activity Table 39). Source: NHSAC State of the Housing System, Early 2026 Outlook; ABS Building Activity (cat. 8752.0); ABS Building Approvals (cat. 8731.0).

SECTION 03 · APPROVALS VS COMPLETIONS

The gap between NT approvals and completions

NT dwelling completions fell from 1,857 in FY2015–16 to 408 in FY2024–25, a drop of 78% over nine years. Over the same period, annual dwelling approvals also declined, although they recovered from 437 in FY2023–24 to 703 in FY2024–25. That left a one-year gap of 295 dwellings between approvals and completions in FY2024–25.

The gap partly reflects the time between approval and completion. Labour availability, supply chains and the remoteness of some NT projects can affect delivery timelines. This means annual approvals and completions do not always move together, even when both measures refer to the same housing market.

Recent approval figures show an increase in the pipeline. Approvals over the 18 months to December 2025 reached approximately 1,134, and FY2025–26 recorded 669 approvals in its first ten months, from July 2025 to April 2026. If that pace continued across the full financial year, FY2025–26 approvals would exceed 800 for the first time since FY2020–21.

NT completions trend

2,385

completed in FY2014–15 (peak in records from FY2014–15 to FY2024–25)

408

completed in FY2024–25 (the lowest in the same period)

−83%

decline in dwelling completions from the FY2014–15 peak to FY2024–25

View full NT housing activity table (FY2014–15 to FY2024–25)

| Financial year | Approvals | Approved value | Commencements | Houses comp. | Other res. comp. | Other work | Total comp. |

|---|---|---|---|---|---|---|---|

| 2014–15 ★ Peak | 1,814 | $557.3m | 2,003 | 882 | 1,482 | 20 | 2,385 |

| 2015–16 | 1,703 | $539.3m | 1,539 | 936 | 852 | 70 | 1,857 |

| 2016–17 | 912 | $307.8m | 1,074 | 760 | 456 | 20 | 1,235 |

| 2017–18 | 773 | $264.3m | 864 | 710 | 154 | 17 | 881 |

| 2018–19 | 680 | $243.9m | 650 | 542 | 242 | 16 | 800 |

| 2019–20 | 582 | $210.9m | 524 | 393 | 95 | 19 | 506 |

| 2020–21 | 795 | $304.2m | 909 | 454 | 108 | 21 | 586 |

| 2021–22 | 529 | $194.7m | 496 | 490 | 88 | 16 | 594 |

| 2022–23 | 603 | $271.9m | 604 | 432 | 126 | 68 | 627 |

| 2023–24 | 437 | $218.5m | 437 | 454 | 63 | 7 | 524 |

| 2024–25 | 703 | $381.8m | 459 | 357 | 50 | 1 | 408 |

Notes: Approvals are total dwelling approvals for each financial year. Total completions include other building work. Sources: ABS Building Approvals; ABS Building Activity.

NT dwelling completions vs approvals, FY2015–16 to FY2024–25

Completions fell to 408 in FY2024–25, 83% below the FY2014–15 peak. Approvals recovered to 703, while the dashed line shows the 2,200-dwelling annual pace required under the NT's Housing Accord target.

Source: ABS Building Approvals (cat. 8731.0), Table 18, NT total sectors. ABS Building Activity (cat. 8752.0), Table 39, NT total sectors. Financial year totals, original series.

NT approved residential building value, January 2024 to April 2026

Approved residential building values increased from mid-2024. April 2026 recorded $50.0 million, the highest monthly value in the period, alongside 110 total dwelling approvals.

Source: ABS Building Approvals (cat. 8731.0), Table 28, NT total residential building value, original series. Values in $'000.

SECTION 04 · WHERE HOUSING IS BEING BUILT

Where is new housing being built in Darwin?

Greater Darwin accounted for 70% of all NT residential building approval applications in FY2024–25. Construction activity is concentrated in two areas: Palmerston's southern growth corridor and a handful of outer Darwin suburbs undergoing subdivision or medium-density infill.

Palmerston recorded 183 approvals, representing 49% of the Greater Darwin total. Palmerston South alone drove 153 of those (41% of all Greater Darwin approvals), with an approved residential value of $71.6 million, the highest of any Darwin suburb. The suburb added 344 residents in 2024–25, among the strongest growth figures in the city.

In the Darwin Suburbs SA3, Berrimah dominated with 63 approvals, or 67% of that SA3's total of 94. Most were detached houses linked to the Berrimah Farm residential development, with Lyons the next most active suburb at 14.

Litchfield recorded 56 approvals, all detached houses, spread across Humpty Doo (18), Howard Springs (15), Virginia (14) and Weddell (9). Darwin City SA3 had the fewest approvals at 41 but the highest medium-density share: 28 of 41 (68%) were apartments or townhouses, with Darwin City suburb accounting for 24 of those.

Outside Greater Darwin, 160 approvals were recorded across five remote regions: Barkly (40), Katherine (39), Daly–Tiwi–West Arnhem (36), Alice Springs (33) and East Arnhem (12). Public sector housing programmes account for a large share of approval activity in these areas.

Residential building approvals by suburb, Greater Darwin, FY2024–25

Palmerston South accounted for 41% of Greater Darwin approvals. The top five suburbs accounted for 70%. Solid bars show houses; faded bars show townhouses and apartments.

Palmerston

Darwin Suburbs

Darwin City

Litchfield

Darwin City

Darwin Suburbs

Litchfield

Litchfield

Darwin Suburbs

Palmerston

Palmerston

Litchfield

Palmerston

Note: Counts residential building approval applications (not dwelling units). Each application may contain one or more dwellings. Suburbs with fewer than 3 approvals are grouped into their SA3 "other" category. Source: ABS Building Approvals, Australia (cat. 8731.0), 87310DO026_202507, NT SA2 data cube, FY2024–25 (July 2024 to June 2025).

NT population distribution and growth, 2024–25

Source: ABS Regional Population 2024–25 (cat. 3218.0), Table 7, NT SA2 level data. Greater Darwin figure sums Darwin City, Darwin Suburbs, Litchfield, and Palmerston SA3 areas.

Dwelling type varies significantly by area

Litchfield recorded zero non-house approvals across all four of its suburbs. Darwin Suburbs SA3 was 91% houses, with Berrimah (63 approvals, 57 of them houses) and Lyons (14 houses) driving the numbers. Palmerston was 82% houses, with non-house approvals concentrated in Bakewell (12 townhouse projects) and Durack–Marlow Lagoon (10). Darwin City SA3 was the exception: 68% of its 41 approvals were apartment or medium-density projects, almost all in Darwin City suburb (24) and Larrakeyah (4).

Dwelling type mix by SA3 area, Greater Darwin, FY2024–25

Darwin City was the only SA3 where apartments, townhouses and semi-detached approvals outnumbered houses. In every other area, houses made up at least 80% of approvals. Numbers above bars = SA3 total.

Source: ABS Building Approvals, Australia (cat. 8731.0), 87310DO026_202507, NT SA2 data cube, FY2024–25 (July 2024 to June 2025). Counts residential building approval applications; each application may contain one or more dwellings.

SECTION 05 · REMOTE HOUSING

Remote housing: why supply works differently outside Darwin

The public sector accounted for 30% of NT house approvals in 2024, rising to 33% in 2025, the highest sustained share since the 2008 to 2010 stimulus period. A significant share of the NT population lives outside Greater Darwin and Alice Springs. In those areas, new housing activity is more likely to involve public sector housing than private sector construction. This has a direct effect on NT housing data. Large federal or territory housing programmes can increase approval totals sharply in individual months. In December 2008, the NT recorded 436 new residential dwelling approvals in a single month, with 390 from the public sector and 46 from the private sector.

Remote housing faces structural constraints that do not apply in the same way in urban Darwin. Land tenure in remote communities is often held under the Aboriginal Land Rights Act or subject to long-term government leasing, which can limit conventional market financing. Distance from Darwin, limited local trades capacity and high logistics costs can extend construction timelines compared with similar projects in larger urban markets.

Residential approvals outside Greater Darwin, FY2024–25

The 160 residential building approvals recorded outside Greater Darwin in FY2024–25 were spread across five regions. Barkly recorded 40 approvals, including a high share of non-house projects, with 12 of 40 approvals in Tennant Creek. Katherine followed with 39 approvals, mostly in Katherine township, where 32 house approvals were recorded. West Arnhem was the most active single remote NT area, with 25 approvals, while East Arnhem recorded 12.

| Region (SA3) | Key areas | Houses | Other res. | Total | Res. value |

|---|---|---|---|---|---|

| Katherine | Katherine township (32), Gulf (4), Victoria River (3) | 37 | 2 | 39 | $19.0m |

| Barkly | Tennant Creek (27), Barkly region (13) | 28 | 12 | 40 | $24.1m |

| Daly – Tiwi – West Arnhem | West Arnhem (25), Daly (8), Alligator (3) | 24 | 12 | 36 | $24.7m |

| Alice Springs | Alice Springs city (27), remote SA2s (6) | 27 | 6 | 33 | $31.0m |

| East Arnhem | Nhulunbuy (12) | 8 | 4 | 12 | $11.2m |

| Rest of NT total | 124 | 36 | 160 | $109.9m |

Note: Counts residential building approval applications. "Other residential" includes apartments, townhouses, and semi-detached dwellings. Source: ABS Building Approvals (cat. 8731.0), NT SA2 data cube, FY2024–25.

SECTION 06 · GREENFIELD, INFILL AND INFRASTRUCTURE

Greenfield growth accounts for most Greater Darwin approvals

Outer growth areas accounted for 73% of all Greater Darwin residential approvals in FY2024–25, with 272 of 374 approvals. Palmerston South and the four main Litchfield suburbs, Humpty Doo, Howard Springs, Virginia and Weddell, together accounted for 209 approvals, or 56% of the Greater Darwin total. Berrimah also contributed to outer-area activity, with subdivision-style development on former rural land. Palmerston South recorded $71.6 million in approved residential value, the highest of any Darwin suburb, and added 344 residents in 2024–25.

Medium-density approvals, including apartments, townhouses and semi-detached dwellings, made up 23% of Greater Darwin residential approvals in FY2024–25. Darwin City SA3 recorded 41 total approvals, while the combined established middle-ring suburbs of Karama, Malak–Marrara, Nightcliff, Coconut Grove and Jingili recorded one house approval between them. Although Darwin has flat land and relatively large residential lots, the approval data shows limited medium-density activity outside Darwin City.

Infrastructure is a factor in growth corridor expansion. The Palmerston ring road and associated transport works have supported development in the satellite city, while water, sewerage and power networks in outer areas need to expand alongside population growth.

SECTION 07 · STATE COMPARISON

NT housing supply compared with other states and territories

The NT delivered 111 completed dwellings per 1,000 new residents in FY2024–25, the lowest ratio of any mainland state. By comparison, Western Australia recorded 343, Victoria 455 and NSW 424 over the same period. In raw volume, NT completions of 408 sit alongside WA's 22,736 and Victoria's 55,909. This reflects the Territory’s small population base and lower completion levels after a decade of decline.

That ratio needs qualification. A large share of NT population growth came from overseas migration concentrated in Darwin, while net internal migration was negative, meaning more residents left for other states than arrived from them. This means the completions-per-new-resident ratio should be read alongside migration patterns, not as a standalone measure of housing pressure.

Note: Accord target and estimated supply figures are from NHSAC Table 4.1, Early 2026 Outlook. Completions per 1,000 new residents is a Build Street calculation using ABS Building Activity and ABS Regional Population data. Sources: NHSAC State of the Housing System, Early 2026 Outlook; ABS Regional Population 2024–25; ABS Building Activity.

SECTION 08 · DEMAND DRIVERS

What is driving new housing demand in the NT?

NT population grew by 3,672 in 2024–25, but the composition of that growth is important. Net overseas migration added 3,753 people, natural increase contributed 2,024, and net internal migration subtracted 2,105 residents. This mix means NT housing demand cannot be read from the headline population growth figure alone.

Overseas migration was the largest contributor to NT population growth

Net overseas migration of 3,753 was the largest single contributor to NT population growth in 2024–25, more than offsetting the internal migration loss. Because most private sector construction is concentrated in Greater Darwin, overseas migration can affect housing demand differently from natural increase or internal migration.

Net internal migration remained negative

The NT lost a net 2,105 residents to other states in 2024–25. The pattern varied across Greater Darwin. Karama lost 167 residents through internal migration, Malak–Marrara lost 111, and Coconut Grove lost 111. Palmerston South gained 111 residents, and Berrimah gained 479, both areas with newer or expanding housing stock.

Employment sectors support Darwin housing demand

The 59% rise in approvals from 2024 to 2025 coincided with several factors, including deferred construction activity, renewed public sector housing programmes and higher approved residential values. The data does not isolate how much each factor contributed to the increase. Darwin’s demand base is supported by Defence, federal government employment, the oil and gas sector, and NT government employment. These sectors form part of the city’s employment base, but the approval data does not show their direct effect on housing demand.

Overseas migration 2024–25

+3,753

Largest contributor to NT population growth.

Net internal migration 2024–25

−2,105

More residents left the NT for other states than arrived from them.

Natural increase 2024–25

+2,024

Births minus deaths.

Greater Darwin population

≈159,300

About 60% of total NT population; the primary market for private sector construction.

CY2025 approvals recovery

+59%

Dwelling approvals rose from 518 (2024) to 823 (2025); strongest annual total since 2016.

Public sector housing share 2025

33%

Highest share outside the 2008 to 2010 stimulus period.

Source: ABS Regional Population 2024–25 (cat. 3218.0); ABS Building Approvals (cat. 8731.0), Table 18, NT Private and Public Sector, original series.

General information only

This article draws on publicly available data from the Australian Bureau of Statistics. Building approval and completion figures use the original, unadjusted series and are subject to revision. Financial year completion totals are derived from quarterly ABS Building Activity data and may differ from later ABS releases. Unless stated otherwise, figures refer to the Northern Territory as a whole. This article is general information only and does not constitute financial, investment or planning advice.

Building Approvals, Australia, April 2026 | Australian Bureau of Statistics: Building Approvals, Australia (cat. 8731.0), Table 18, Table 28, and NT SA2 data cubes.

Building Activity, Australia, December 2025 | Australian Bureau of Statistics: (cat. 8752.0), Table 39.

Regional population, 2024-25 financial year | Australian Bureau of Statistics: Regional Population, Australia, 2024–25 (cat. 3218.0), Tables 7 and 8

National Housing Supply and Affordability Council, State of the Housing System 2026

Chart Snapshots