First home buyer support in Australia in 2026: grants, guarantees and concessions by state

More than one in three first home buyers nationally used the federal deposit guarantee scheme in 2024–25, up from one in ten in 2020–21, the scheme's first full year of operation. Seasonally adjusted first home buyer loan commitments reached 31,590 in the December 2025 quarter, before easing to 30,241 in the March 2026 quarter. The derived average first home buyer loan size reached $614,048 by March 2026.

State cash grants range from no cash grant in the ACT to $50,000 in the Northern Territory. Queensland continues to offer a $30,000 grant for eligible new-home transactions, while Tasmania's $30,000 grant is set to reduce from 1 July 2026, subject to legislation. South Australia has removed the property value cap from its cash grant and its new-home stamp duty exemption.

FHBs backed by federal scheme, 2024–25

1 in 3

Up from 1 in 10 in 2020–21

Derived average FHB loan size, March 2026

$614,048

Up 1.1% on Dec 2025 quarter

Home Guarantee Scheme places taken up, 2024–25

46,022

92% of 50,000 available places, including Family Home Guarantee places

Highest cash grant in Australia (NT, contract deadline Sep 2027)

$50,000

Application deadline Sep 2028

Section 01 · Support overview

What first home buyer support is available in 2026?

State grants range from $10,000 to $50,000, depending on the state, territory and property type. The federal deposit guarantee scheme supported more than one in three first home buyers nationally in 2024–25. Together, five main programme types make up the core forms of government assistance available to first home buyers in 2026.

Federal programmes mainly relate to deposits, loan size and shared equity. State and territory cash grants and duty concessions reduce purchase costs for eligible buyers. Some programmes may be available for the same purchase, but eligibility depends on each scheme's rules, including contract date, settlement date, property type, property value and owner-occupier requirements.

| Type of support | What it does | Who administers it |

|---|---|---|

| Deposit guarantee | The government guarantees part of the loan so eligible buyers can purchase with a 2–5% deposit without paying Lenders Mortgage Insurance | Housing Australia (federal) |

| Shared equity | The government co-owns up to 40% of a new home, or 30% of an established home, reducing the loan the buyer needs to take out | Housing Australia (federal) |

| First Home Super Saver Scheme | Buyers can make voluntary super contributions and later withdraw them (with a tax advantage) toward a home deposit | Australian Taxation Office (federal) |

| First Home Owner Grant | A one-off cash payment from the state or territory government, generally for new homes only, subject to property value caps | State and territory revenue offices |

| Stamp duty concession | A full or partial exemption from transfer duty on eligible first home purchases, with thresholds and qualifying property types set by each state or territory | State and territory revenue offices |

First home buyer grants and stamp duty concessions by state

The Northern Territory's $50,000 HomeGrown Territory Grant is the largest cash payment available in Australia. South Australia offers the broadest stamp duty relief, with no value cap on new home purchases since June 2024. The ACT has not offered a cash grant since 2019, instead providing an income-tested duty concession that can apply across new homes, established homes and vacant land. Queensland continues to offer a $30,000 grant for eligible new homes, while Tasmania's $30,000 grant is scheduled to reduce from 1 July 2026, subject to legislation.

| State/territory | Cash grant | Stamp duty support | Main 2026 note |

|---|---|---|---|

| New South Wales | $10,000 | Full exemption to $800,000 (new or existing homes) | Grant limited to new homes; value cap $600,000 (completed) or $750,000 (house-and-land) |

| Victoria | $10,000 | Full exemption to $600,000 | Temporary off-the-plan concession extended to 21 April 2027, pending legislation |

| Queensland | $30,000 for eligible new homes | Full first home concession to $700,000 | The $30,000 grant continues for eligible contracts signed from 1 July 2026 onward |

| Western Australia | $10,000 | Full exemption to $600,000 (from 7 May 2026) | Grant cap raised to $800,000 south of 26th parallel from 7 May 2026; full duty threshold also raised |

| South Australia | $15,000 | Full exemption, no value cap (new homes from 6 June 2024) | No property value cap on the grant or duty exemption; both apply to new homes only |

| Tasmania | $30,000 (to 30 Jun 2026); $20,000 from 1 Jul 2026* | 100% exemption for established homes to $750,000 (to 30 June 2026) | Time-limited established-home concession ends 30 June 2026 under current legislation |

| Australian Capital Territory | No cash grant | From 1 Jul 2026: no stamp duty for ACT first home buyers. To 30 Jun 2026: 2025–26 HBCS thresholds apply | No FHOG since 2019; HBCS covers new, established, and vacant land |

| Northern Territory | $50,000 (contract deadline 30 Sep 2027) | No broad first-home-buyer stamp duty concession; support mainly via the HomeGrown Territory Grant | Grant applies to eligible new homes incl. off-the-plan, owner-builders and new transportable homes (app deadline 30 Sep 2028) |

Amounts and deadlines reflect state revenue office information current at June 2026. Time-limited schemes depend on contract, application, or settlement dates. Scheme rules and deadlines are subject to change.

Section 02 · Federal schemes

Federal first home buyer schemes

One in three first home buyers nationally used the federal deposit guarantee scheme in 2024–25, up from one in ten in 2020–21, the scheme's first full year of operation. Since January 2020, the scheme has supported more than 230,000 Australians into home ownership. Help to Buy, the federal shared equity scheme, opened to applications in December 2025.

The three main federal first home buyer programmes in 2026

The Australian Government 5% Deposit Scheme lets eligible buyers purchase with a 5% deposit and no Lenders Mortgage Insurance. The Help to Buy Scheme has the government contribute up to 40% of the purchase price, reducing the loan the buyer needs to take out. The First Home Super Saver Scheme allows eligible buyers to withdraw eligible voluntary super contributions and associated earnings for a home deposit.

Australian Government 5% Deposit Scheme

The scheme was renamed from the Home Guarantee Scheme on 1 October 2025. The renamed scheme removed income caps, waitlists and annual place limits, while higher property price caps also took effect.

Through Housing Australia, the government guarantees part of the loan so eligible buyers can purchase with as little as a 5% deposit, without paying Lenders Mortgage Insurance. Single parents or legal guardians with at least one dependent can use the scheme with a 2% deposit and do not need to be first home buyers. Participants must live in the property as owner-occupiers.

In 2024–25, scheme take-up was near capacity across all three programmes:

- 34,948 of 35,000 First Home Guarantee places were taken up

- 9,986 of 10,000 Regional First Home Buyer Guarantee places were taken up

- Victoria accounted for 37% of all guarantees, above its 26% population share

Including the Family Home Guarantee, total take-up across all three guarantee streams was 46,022, representing 92% of the 50,000 available places. Since launch in January 2020, more than 230,000 Australians have bought through the scheme. Over 34,000 of those households have since exited by paying off the loan or refinancing, with an average discharge time of 29 months.

| State/territory | Capital city & regional centres | Other areas |

|---|---|---|

| New South Wales | $1,500,000 | $800,000 |

| Victoria | $950,000 | $650,000 |

| Queensland | $1,000,000 | $700,000 |

| Western Australia | $850,000 | $600,000 |

| South Australia | $900,000 | $500,000 |

| Tasmania | $700,000 | $550,000 |

| Australian Capital Territory | $1,000,000 | — |

| Northern Territory | $600,000 (Darwin: $750,000 from Jul 2026) | $600,000 |

Regional centres are: NSW (Illawarra, Newcastle and Lake Macquarie), VIC (Geelong), QLD (Gold Coast and Sunshine Coast). Both the purchase price and the lender's assessed value must be at or below the applicable cap. For separate land and construction contracts, the combined cost must stay within the cap.

Help to Buy Scheme

Help to Buy opened to applications on 5 December 2025. The government contributes up to 40% of the purchase price for new homes, or up to 30% for established homes. Buyers need a minimum 2% deposit and are not charged interest or rent on the government's share. When the property is sold, the government's share is repaid based on the market value at that time.

Annual taxable income must be no more than $100,000 for individual applicants, or $160,000 for joint applicants or single parents. These thresholds are indexed on 1 July each year. Participants cannot own any other residential property in Australia or overseas. Single parents who hold a share in a jointly owned property may be eligible in some circumstances.

The scheme has 10,000 places available each year and is designed to support up to 40,000 households over four years. Bank Australia and the Commonwealth Bank of Australia were the initial participating lenders, with more lenders joining during 2026.

Help to Buy uses the same price caps as the 5% Deposit Scheme in all states and territories except New South Wales, where the Help to Buy capital city cap is $1,300,000 compared with $1,500,000 under the deposit scheme.

First Home Super Saver Scheme

The FHSS lets buyers use the lower tax rates inside superannuation to save for a home deposit. Voluntary contributions of up to $15,000 per financial year can be made, with a lifetime cap of $50,000 across all years.

When released, eligible amounts include all after-tax contributions and 85% of before-tax contributions, plus associated deemed earnings. The scheme can generally be used alongside the 5% Deposit Scheme and state grants, subject to each programme's rules.

| Scheme | Support type | Min deposit | Income cap | Administrator |

|---|---|---|---|---|

| 5% Deposit Scheme | Government loan guarantee; avoids Lenders Mortgage Insurance | 5% / 2% | None (from Oct 2025) | Housing Australia |

| Help to Buy | Shared equity: up to 40% equity (new homes), 30% (established) | 2% | $100,000 individual; $160,000 joint | Housing Australia |

| First Home Super Saver | Deposit saving via concessional superannuation tax rate | N/A | None | ATO |

The 5% Deposit Scheme minimum deposit is 5% for most first home buyers and 2% for single parents or legal guardians with dependants. Help to Buy income caps are indexed on 1 July each year. The FHSS lifetime contribution cap is $50,000.

Section 03 · State and territory grants

First home owner grants by state and territory

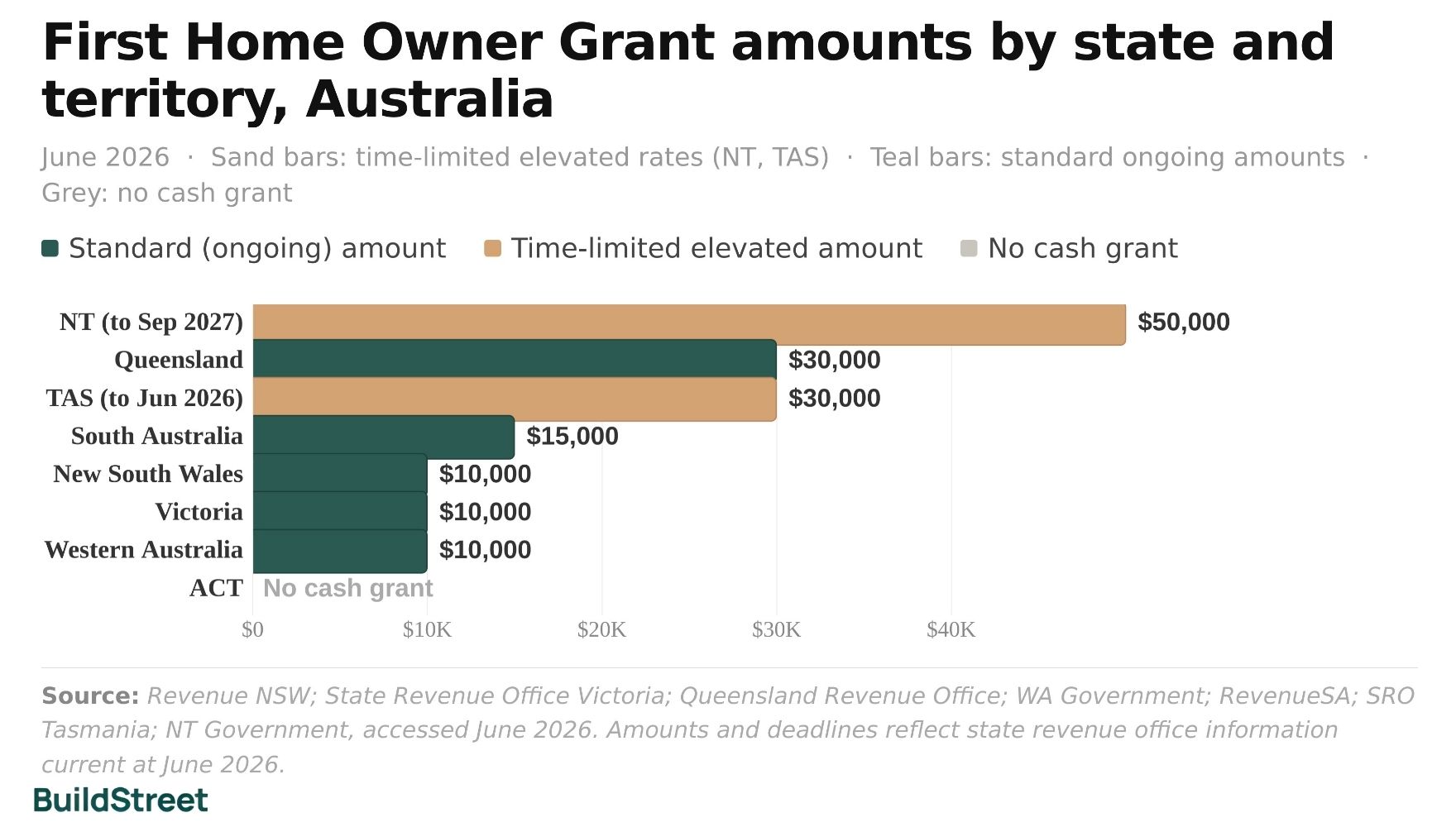

Cash grants range from $10,000 in NSW, Victoria and WA to $50,000 in the Northern Territory. Queensland continues to offer a $30,000 grant for eligible new homes, while Tasmania's $30,000 grant is scheduled to reduce from 1 July 2026, subject to legislation. All current grants apply to new homes only.

Grant amounts at a glance

Amounts range from $10,000 in NSW, Victoria and WA to $50,000 in the NT, where the contract or build-start deadline is 30 September 2027. Queensland continues to offer $30,000 for eligible new homes. Tasmania's $30,000 grant is scheduled to reduce to $20,000 from 1 July 2026, subject to legislation. SA provides $15,000 with no property value cap for eligible new homes from 6 June 2024. The ACT has no cash grant.

Grants are almost exclusively for new homes

Apart from an NT established-home grant that ended in September 2025, no state or territory currently offers a cash grant for purchasing existing housing stock. The largest grant amounts are limited to new homes.

- Northern Territory ($50,000): Eligible applicants must sign a contract or start owner-builder construction by 30 September 2027. Applications are accepted until 30 September 2028.

- Queensland ($30,000): Applies to eligible new-home transactions and continues for eligible contracts signed from 1 July 2026 onward.

- Tasmania ($30,000, time-limited): Set to reduce to $20,000 from 1 July 2026, pending passage of legislation. The $20,000 rate comprises a $10,000 base plus a $10,000 additional payment.

- South Australia ($15,000, uncapped): No property value cap for contracts from 6 June 2024.

- Western Australia ($10,000): Grant cap raised from $750,000 to $800,000 south of the 26th parallel from 7 May 2026.

- NSW and Victoria ($10,000): Apply to new homes with specific property value limits.

- ACT: No cash grant. The territory replaced it with a duty concession scheme in 2019.

First Home Owner Grant amounts by state and territory, Australia, June 2026

Sand bars: time-limited elevated rates (NT, TAS). Teal bars: standard ongoing amounts. Grey: no cash grant.

Source: Revenue NSW; State Revenue Office Victoria; Queensland Revenue Office; WA Government; RevenueSA; SRO Tasmania; NT Government, accessed June 2026.

| State/territory | Current amount | Property type | Value cap | Change |

|---|---|---|---|---|

| New South Wales | $10,000 | New and substantially renovated | $600,000 (completed); $750,000 (H&L) | No change scheduled |

| Victoria | $10,000 | New, never previously sold or occupied | Up to $750,000 dutiable value | No change scheduled |

| Queensland | $30,000 | New homes only | Under $750,000 | Continues for contracts signed from 1 Jul 2026 onward |

| Western Australia | $10,000 | New homes | $800,000 south of 26th parallel (from 7 May 2026); $1,000,000 north | Cap increased 7 May 2026 |

| South Australia | $15,000 | New homes, off-the-plan, substantially renovated | No cap (contracts from 6 Jun 2024) | No change scheduled |

| Tasmania | $30,000 (time-limited) | New homes | No stated value cap | Reduces to $20,000 from 1 Jul 2026, subject to legislation |

| Australian Capital Territory | No grant | — | — | FHOG discontinued 1 July 2019 |

| Northern Territory | $50,000 (time-limited) | New homes, off-the-plan, new transportable | No stated cap | Contract/build-start deadline 30 Sep 2027; app deadline 30 Sep 2028 |

For SA: knock-down rebuild projects are not eligible for contracts entered into on or after 13 February 2025. The NT $10,000 established-home grant (for contracts to 30 September 2025) has expired. Grant eligibility depends on residency, citizenship, and prior-ownership conditions set by each state and territory revenue authority.

Section 04 · Stamp duty concessions

Stamp duty concessions for first home buyers by state

First home buyer stamp duty concessions vary widely by state and territory. NSW provides a full exemption up to $800,000 for new and established homes, while Victoria and Western Australia provide full exemptions up to $600,000. South Australia has no value cap for eligible new homes, and Queensland has no value cap for eligible first home buyers purchasing a brand-new home from 1 May 2025. Two of Tasmania's time-limited duty concessions expire on 30 June 2026.

How stamp duty concessions work

Transfer duty (commonly called stamp duty) is a state and territory tax paid when buying a property. Most states give first home buyers a full exemption up to a set price threshold, with a partial reduction above it. South Australia offers a full exemption for new homes with no value cap. In the ACT, 2025–26 HBCS thresholds apply to 30 June 2026. From 1 July 2026, stamp duty is scheduled to be abolished for ACT first home buyers. NT relief is limited to house-and-land packages only.

Tasmania duty concessions end 30 June 2026

Tasmania's full duty exemption for first home buyers purchasing established homes with a dutiable value up to $750,000 applies to transfers that complete by 30 June 2026. Its 50% concession for eligible off-the-plan apartments or units also closes on 30 June 2026.

Each state and territory runs its own concession framework. The main differences are which property types qualify, at what price threshold the full exemption applies, and whether current settings are ongoing or temporary.

South Australia provides a full stamp duty exemption with no value cap on eligible new homes. For contracts from 6 June 2024, first home buyers pay no stamp duty on new homes, off-the-plan apartments, or vacant land for new construction. No relief applies to established homes.

The ACT provides no duty up to $1,020,000 across all property types through its Home Buyer Concession Scheme, subject to income testing. The income threshold is $250,000 for buyers with no dependants, rising by $4,600 per dependent child. The maximum concession is $35,238. These ACT thresholds apply to 2025–26 settings before the 1 July 2026 change.

Western Australia announced in May 2026 that eligible newly built or established homes valued up to $600,000 would pay no duty, with a concessional rate above that to $800,000. RevenueWA has noted some of these changes remain subject to the Parliamentary process and system updates.

| State/territory | Full exemption (new homes) | Full exemption (established) | Concession range | Key notes |

|---|---|---|---|---|

| New South Wales | Up to $800,000 | Up to $800,000 | Over $800,000 and less than $1,000,000 | Vacant land: full to $350,000; concession over $350,000–$450,000 |

| Victoria | Up to $600,000 dutiable value | Up to $600,000 | $600,001–$750,000 | Vacant land dutiable value excludes build cost. Temp off-the-plan concession extended to 21 Apr 2027. |

| Queensland | Full concession for eligible brand-new homes (no value cap) | Full concession to $700,000 | $700,001–$799,999 (sliding scale) | Brand-new and established homes treated under different concession settings |

| Western Australia | Up to $600,000 (from 7 May 2026) | Up to $600,000 (from 7 May 2026) | $600,001–$800,000 | Vacant land: full to $450,000; concession to $550,000. Changes from 7 May 2026. |

| South Australia | No cap (contracts from 6 June 2024) | No relief | N/A | New homes, off-the-plan, vacant land for new build only |

| Tasmania | Standard new-home framework (continues post Jul 2026) | 100% to $750,000 (to 30 Jun 2026); does not continue 1 Jul 2026 | 50% on off-the-plan to $750,000 (to 30 Jun 2026) | Two time-limited concessions expire 30 June 2026 under current legislation |

| Australian Capital Territory | To 30 Jun 2026: no duty to $1.02m. From 1 Jul 2026: no stamp duty. | To 30 Jun 2026: no duty to $1.02m. From 1 Jul 2026: no stamp duty. | To 30 Jun 2026: $1.02m–$1.455m sliding scale. From 1 Jul 2026: n/a. | To 30 Jun 2026: income-tested HBCS applies. From 1 Jul 2026: applies to ACT FHBs. |

| Northern Territory | House-and-land packages only (contracts 1 Jul 2022–30 Jun 2027) | No broad relief | — | NT cash grant is the primary support vehicle |

Thresholds reflect current legislation and announced changes as at June 2026. Stamp duty settings can change with state budgets. ACT figures are 2025–26 Home Buyer Concession Scheme thresholds; the income threshold is updated annually.

Section 05 · Price caps compared

First home buyer property price caps by state

NSW is the only state where the caps for the two federal schemes differ: the 5% Deposit Scheme capital city cap of $1,500,000 sits $200,000 above the Help to Buy cap of $1,300,000. In the other states and territories, the listed state-level price caps are the same across the two schemes.

The NSW difference reflects how the two schemes are set up. Help to Buy has income caps of $100,000 for individual applicants and $160,000 for joint applicants or single parents. The 5% Deposit Scheme has no income cap, although applicants still need to meet lender assessment and scheme eligibility rules.

From 1 July 2026, the Northern Territory will have two separate price caps under the 5% Deposit Scheme: $750,000 for Darwin and $600,000 for the rest of the territory.

Property price caps by state: 5% Deposit Scheme and Help to Buy

Capital city and major regional centre caps only. Rest-of-state caps are shown in the table below.

Source: Housing Australia, 5% Deposit Scheme and Help to Buy property price caps, firsthomebuyers.gov.au, accessed June 2026.

| State/territory | 5% Deposit: capital/regional | 5% Deposit: other areas | Help to Buy: capital/regional | Help to Buy: other areas |

|---|---|---|---|---|

| New South Wales | $1,500,000 | $800,000 | $1,300,000 | $800,000 |

| Victoria | $950,000 | $650,000 | $950,000 | $650,000 |

| Queensland | $1,000,000 | $700,000 | $1,000,000 | $700,000 |

| Western Australia | $850,000 | $600,000 | $850,000 | $600,000 |

| South Australia | $900,000 | $500,000 | $900,000 | $500,000 |

| Tasmania | $700,000 | $550,000 | $700,000 | $550,000 |

| Australian Capital Territory | $1,000,000 | — | $1,000,000 | — |

| Northern Territory | $600,000 | $600,000 | $600,000 | $600,000 |

From 1 July 2026, Darwin will have its own cap of $750,000 under the 5% Deposit Scheme. Regional centre definitions for Help to Buy may differ from those used for the 5% Deposit Scheme in some postcodes.

Section 06 · Common eligibility

Common eligibility rules for first home buyer support

Eligibility rules vary by programme, state and territory. Most schemes include conditions relating to age, citizenship or residency, previous property ownership, property value, property type and owner-occupier use. Some schemes also apply different rules depending on whether the buyer is purchasing alone, with a partner, with another joint applicant or as a single parent.

| Eligibility requirement | What it generally means |

|---|---|

| First home buyer status | The applicant, and in some cases their spouse or partner, must generally meet the scheme's first home buyer or previous-ownership rules. Some federal settings recognise buyers who have not owned property in Australia for a set period. |

| Age | Most programmes require applicants to be at least 18 at the time of application. |

| Citizenship or residency | At least one applicant must generally be an Australian citizen or permanent resident. Some schemes include specific visa or residency categories. |

| Owner-occupier requirement | The buyer must live in the property as their main home for a minimum period after settlement, typically six to twelve months. |

| Property value cap | The purchase price (and the lender's assessed value) must be within the applicable limit. Caps differ by programme, state, and location. |

| Property type | New homes, established homes, off-the-plan apartments, vacant land, and house-and-land packages are treated differently by each programme. Most state cash grants and some duty concessions apply to new homes only. |

| Contract or application date | Eligibility often depends on when the purchase contract is signed, when an application is lodged, or when settlement occurs. |

The requirements above describe how most programmes work in general. Exact definitions, thresholds, and exclusions are set by each scheme's administering authority. Current eligibility criteria are available from the official government source for each programme.

Section 07 · Lending data

First home buyer lending in 2025–26

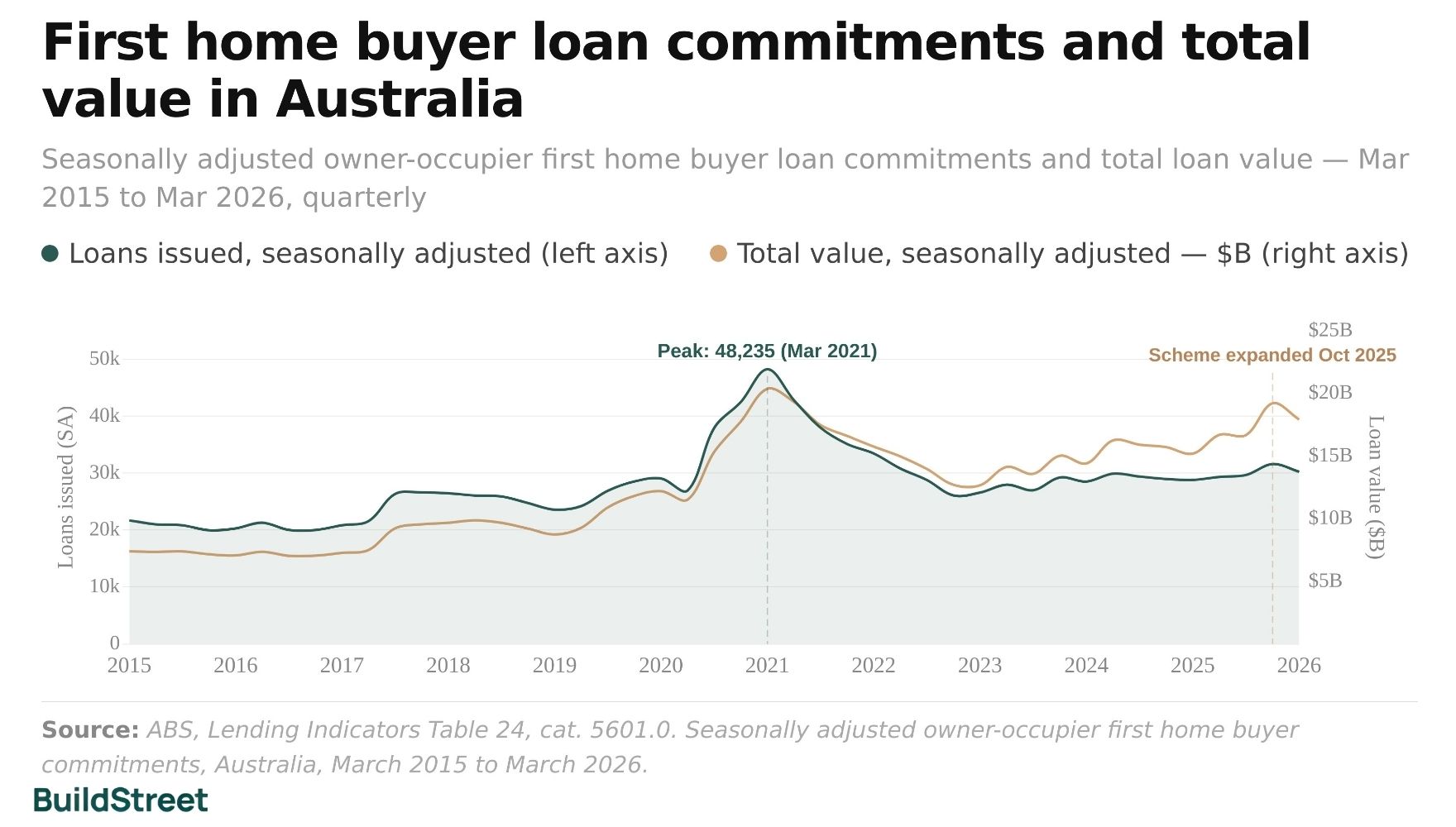

First home buyer lending rose through late 2025 before easing in early 2026. In the owner-occupier first home buyer series, loan commitments reached 31,590 in the December 2025 quarter, the highest quarterly total since early 2022, before falling 4.3% to 30,241 in the March 2026 quarter. The derived average first home buyer loan size reached $614,048 in March 2026, based on ABS loan value and loan count data.

First home buyer loan commitments averaged around 23,000 per quarter from 2015 to 2019, before peaking at 48,235 in the March 2021 quarter. They then fell through 2022 and 2023, before stabilising through 2024–25 and rising for three consecutive quarters to December 2025.

Total first home buyer loan value reached $19.2 billion in the December 2025 quarter, up 15.2% on the September quarter. The December quarter followed the October 2025 expansion of the federal deposit guarantee scheme, which removed income caps and annual place limits.

First home buyer loan commitments and total value in Australia, Mar 2015 to Mar 2026

Seasonally adjusted owner-occupier first home buyer loan commitments and total loan value, quarterly.

Source: ABS, Lending Indicators Table 24, cat. 5601.0. Seasonally adjusted owner-occupier first home buyer commitments, Australia, March 2015 to March 2026.

Quarterly first home buyer lending data, June 2024 to March 2026

| Quarter | Loans issued (SA) | Q/Q | Total value (SA) | Q/Q | Derived avg loan size | Q/Q |

|---|---|---|---|---|---|---|

| Jun 2024 | 29,912 | — | $16.2B | — | $532,177 | — |

| Sep 2024 | 29,395 | −1.7% | $15.9B | −2.1% | $536,510 | +0.8% |

| Dec 2024 | 28,966 | −1.5% | $15.7B | −1.2% | $543,356 | +1.3% |

| Mar 2025 | 28,805 | −0.6% | $15.2B | −3.3% | $542,720 | −0.1% |

| Jun 2025 | 29,335 | +1.8% | $16.7B | +9.8% | $554,732 | +2.2% |

| Sep 2025 | 29,675 | +1.2% | $16.7B | −0.1% | $560,249 | +1.0% |

| Dec 2025 | 31,590 | +6.5% | $19.2B | +15.2% | $607,624 | +8.5% |

| Mar 2026 | 30,241 | −4.3% | $17.9B | −6.7% | $614,048 | +1.1% |

SA = seasonally adjusted. Q/Q = quarter-on-quarter change. Loans issued means owner-occupier first home buyer new loan commitments for dwellings, excluding refinancing. Derived average loan size is calculated from ABS first home buyer loan value divided by first home buyer loan count and is not a separately published ABS statistic.

The March 2026 quarter pulled back from the December 2025 peak. Loans fell 4.3% to 30,241, and total value dropped from $19.2 billion to $17.9 billion. The decline was not specific to first home buyers. Across all borrower types, new loan commitments fell 6.2% in the same quarter.

Year-on-year, first home buyer volumes in March 2026 were 5.0% higher than March 2025, with total value up 17.9%. Derived average loan sizes rose in every quarter across the period. By March 2026, the derived average first home buyer loan reached $614,048, up 1.1% on December 2025.

State and territory results for owner-occupier first home buyer loan commitments in the March 2026 quarter showed:

- Queensland: down 5.8%

- Victoria: down 4.5%

- NSW: down 4.1%

- ACT: the only state or territory to record growth, up 6.5%

Section 08 · Historical context

How first home buyer support has changed in Australia

First home buyer support now includes state cash grants, stamp duty concessions, federal deposit guarantees and federal shared equity support. The First Home Owner Grant remains a state and territory payment, but the federal deposit guarantee scheme has become a larger part of first home buyer support since its launch in January 2020.

The First Home Owner Grant was introduced nationally in July 2000, mainly to offset the GST impact on new home purchases. The model is still based on a one-off payment, but grant amounts, property types and value caps now vary significantly by state and territory.

The federal deposit guarantee scheme changed the structure of first home buyer support. Rather than reducing the purchase price directly, it targets the deposit requirement, allowing eligible buyers to purchase with a deposit as low as 5% without Lenders Mortgage Insurance. The scheme was renamed the Australian Government 5% Deposit Scheme on 1 October 2025, removing income caps, waitlists and annual place limits, while higher property price caps also took effect.

Help to Buy opened to applications in December 2025. It differs from the deposit scheme because the government contributes an equity share in the property, rather than only guaranteeing part of the loan.

Federal deposit scheme growth since launch

Jan 2020

Scheme launched as Home Guarantee Scheme

1 in 10

FHBs supported in 2020–21, first full year of operation

1 in 3

FHBs supported in 2024–25

230,000+

Australians supported since inception to June 2025

Tasmania's grant history shows the degree to which state-level settings can shift. Since 2013, the Tasmanian FHOG has been set at seven different levels, ranging from $10,000 to $30,000.

Tasmania First Home Owner Grant amounts by contract date, 2013 to 2026

July 2026 rate of $20,000 is subject to passage of legislation, comprising a $10,000 base plus a $10,000 additional payment.

Source: State Revenue Office Tasmania, First Home Owner Grant eligibility and historical amounts, accessed June 2026.

In 2026, the largest state and territory cash grants are restricted to new homes. South Australia's full stamp duty exemption applies to eligible new homes, off-the-plan apartments and vacant land for a new build. Queensland's $30,000 grant applies to eligible new homes, and Tasmania's $30,000 grant applies to eligible new homes until 30 June 2026. The Northern Territory's $50,000 HomeGrown Territory Grant applies to eligible first home buyers building or buying a new home, including eligible new transportable homes.

The NSW Shared Equity Home Buyer Helper pilot is no longer accepting applications. The federal Help to Buy Scheme is the main shared equity pathway covered in this article for NSW first home buyers in 2026.

General information only. This article describes government first home buyer support programmes based on official published sources. It does not assess eligibility for any individual, compare individual options or recommend a scheme. Scheme rules, deadlines, thresholds and participating lenders can change. Current criteria are available from the official government source for each programme.

References

- ABS – Lending Indicators, March Quarter 2026, Table 24, cat. 5601.0

- Housing Australia – Home Guarantee Scheme Trends and Insights Report 2024–25

- firsthomebuyers.gov.au – Australian Government 5% Deposit Scheme

- firsthomebuyers.gov.au – 5% Deposit Scheme property price caps

- firsthomebuyers.gov.au – Help to Buy Scheme

- firsthomebuyers.gov.au – Help to Buy Scheme property price caps

- ATO – First Home Super Saver Scheme

- Revenue NSW – First Home Owner (New Homes) Grant

- Revenue NSW – First Home Buyers Assistance Scheme

- State Revenue Office Victoria – First home buyer duty exemption or concession

- Queensland Revenue Office – First Home Owner Grant

- WA Government – First Home Owner Grant

- RevenueSA – First Home Owner Grant

- SRO Tasmania – First Home Owner Grant

- ACT Revenue Office – Home Buyer Concession Scheme

- NT Government – HomeGrown Territory Grant

Chart Snapshots