Community housing in Australia: growth and new supply

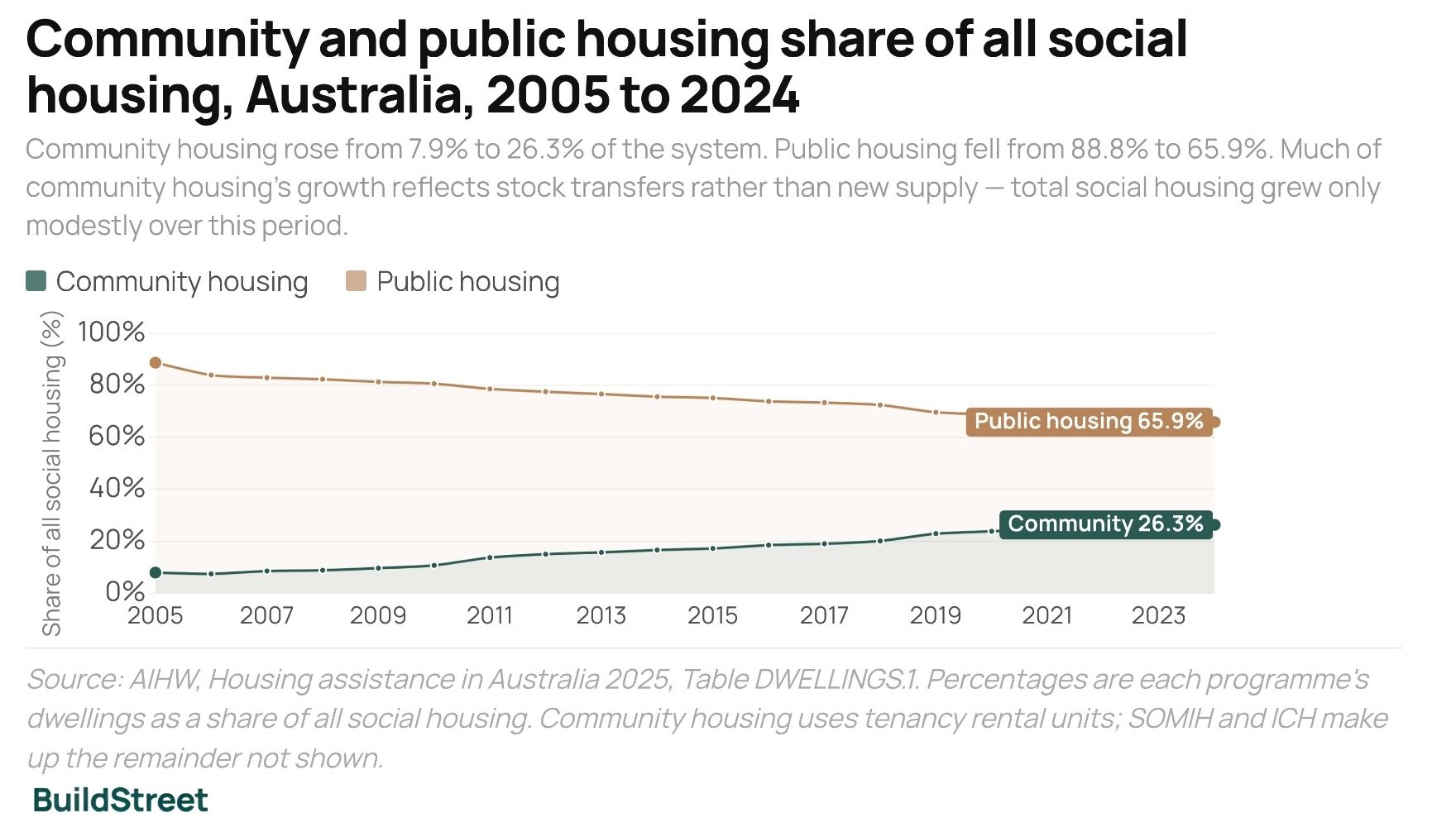

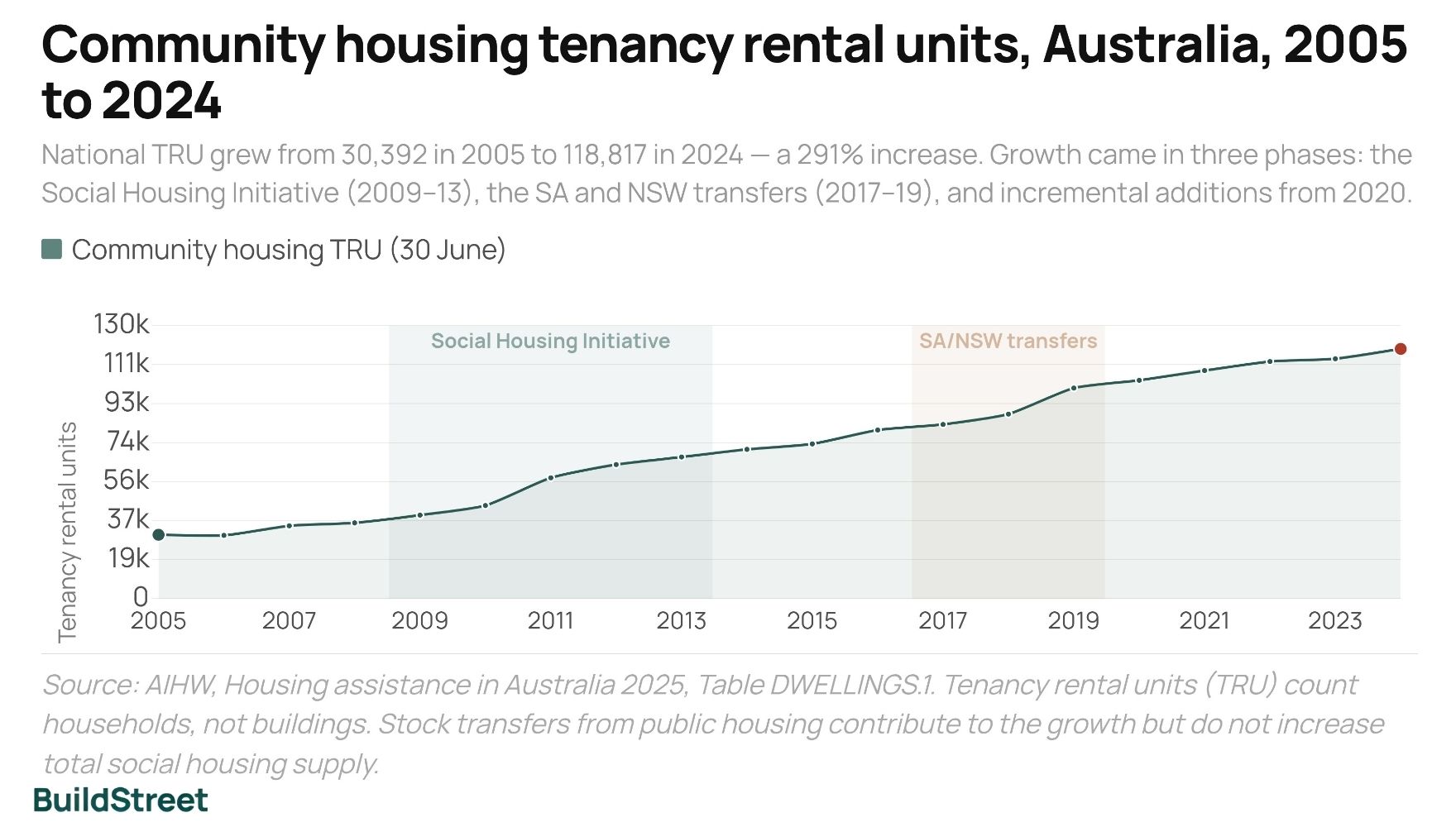

Community housing providers managed 118,817 tenancy rental units at 30 June 2024, up from 30,392 in 2005. Over the same period, community housing's share of Australia's social housing system rose from 7.9% to 26.3%, while public housing's share fell from 88.8% to 65.9%.

This growth came from three main sources: public housing stock transfers to community providers, new construction funded through government grants and private finance, and a funding model that allows eligible community housing tenants to receive Commonwealth Rent Assistance. The $10 billion Housing Australia Future Fund, launched in 2023, is now the largest national programme supporting new social and affordable housing supply through community housing providers.

Community housing TRU, June 2024

118,817

Up from 30,392 in 2005

Growth since 2005

+291%

From 30,392 to 118,817 in 19 years

Share of social housing, 2024

26.3%

Up from 7.9% in 2005

Reporting providers, 2024

531

Community housing organisations

What is the difference between community housing and public housing?

Community housing is managed by not-for-profit providers rather than state and territory governments. The main practical difference is that eligible community housing tenants can receive Commonwealth Rent Assistance, while public housing tenants generally cannot. Both programmes charge below-market rents and serve people who cannot afford private rental.

What caused community housing to grow in Australia?

The sector grew from 7.9% to 26.3% of Australia's social housing system between 2005 and 2024. Most of this growth came from public housing stock transfers, especially in South Australia in 2017–18 and New South Wales in 2018–19. New construction and government programmes using not-for-profit community housing providers also added to the sector over this period.

Section 01 · Definition

What is community housing in Australia?

Community housing accounted for 26.3% of all social housing in Australia at June 2024, up from 7.9% in 2005. It is managed by not-for-profit community housing providers and sits within the wider social housing system alongside public housing, state-owned and managed Indigenous housing, and Indigenous community housing.

Community housing is rental housing managed by not-for-profit community housing providers (CHPs) for people who cannot afford private market rents. Three features distinguish it from public housing:

- Commonwealth Rent Assistance eligibility: Community housing tenants can receive CRA because they rent from a non-government provider. Public housing tenants generally cannot.

- Non-government ownership and management: Community housing properties may be owned, leased or managed by a community housing provider, rather than managed directly by a state or territory government.

- Private finance access: Larger community housing providers can borrow against their property portfolios and raise private funds alongside government grants.

| Programme | Who manages it | Key characteristics |

|---|---|---|

| Public housing | State and territory governments | Direct government management; largest programme; tenants not eligible for CRA |

| Community housing | Not-for-profit CHPs | Non-government providers; tenants may receive CRA; can leverage private finance |

| SOMIH | State authorities (Indigenous-specific) | State-owned and managed Indigenous housing; concentrated in Qld and NT |

| Indigenous community housing | Indigenous community organisations | Funded and unfunded providers; significant data limitations apply |

Section 02 · Current stock

How many community housing homes are there in Australia?

Australia had 118,817 community housing tenancy rental units at 30 June 2024, with 107,637 households in active tenancies — an occupancy rate of 90.6%. The sector grew from 30,392 TRU in 2005 and is now the second-largest component of Australia's social housing system after public housing.

Community housing at a glance, 30 June 2024

The most recent ROGS count was 118,425 TRU at June 2025, slightly below the 2024 AIHW figure. This change should be read cautiously because the figures come from different reporting releases and may reflect reporting or classification differences.

Section 03 · Growth trend

Community housing growth in Australia since 2005

Community housing grew by 291% between 2005 and 2024, from 30,392 to 118,817 tenancy rental units. The increase was not steady. Growth was concentrated in two major periods: the Social Housing Initiative from 2009 to 2013, and stock transfer programmes in South Australia and New South Wales from 2017 to 2019.

Growth in community housing TRU, 2005 to 2024

From 30,392 in 2005 to 118,817 in 2024. Over the same period, public housing stock fell by 45,617 dwellings, while community housing's share of social housing rose from 7.9% to 26.3%.

Community housing TRU, Australia, 2005 to 2024

Stock grew in three phases: the Social Housing Initiative (2009–2013), SA and NSW transfers (2017–2019), and incremental additions from 2020.

Source: AIHW, Housing assistance in Australia, Table DWELLINGS.1 (2025 release).

Early organic growth. Community housing rose from 30,392 to 39,770 TRU through small-scale construction and programme expansion, before major policy interventions reshaped the sector.

Social Housing Initiative. The largest single-year jump occurred in 2010–11, when community housing grew by 13,178 TRU. The Commonwealth programme funded new social housing construction, with a portion delivered through community housing providers.

Consolidation. Moderate growth through incremental transfers and smaller state programmes, rising from 67,385 to 82,902 TRU.

SA and NSW stock transfers. South Australia transferred 3,820 public housing and 225 SOMIH dwellings to CHPs in 2017–18. NSW transferred approximately 10,700 public housing properties in 2018–19, the largest single transfer event in the sector's history.

Incremental growth. Smaller transfers, new construction and programme additions supported growth averaging approximately 3,700 TRU per year.

≡Full annual data table, 2005 to 202520 annual figures + 2025 ROGS

| Year (30 June) | Community housing TRU | Year-on-year change | Share of social housing |

|---|---|---|---|

| 2005 | 30,392 | n/a | 7.9% |

| 2006 | 30,103 | −289 | 7.4% |

| 2007 | 34,672 | +4,569 | 8.5% |

| 2008 | 36,079 | +1,407 | 8.8% |

| 2009 | 39,770 | +3,691 | 9.6% |

| 2010 | 44,328 | +4,558 | 10.7% |

| 2011 | 57,506 | +13,178 | 13.7% |

| 2012 | 63,797 | +6,291 | 15% |

| 2013 | 67,385 | +3,588 | 15.7% |

| 2014 | 71,036 | +3,651 | 16.6% |

| 2015 | 73,620 | +2,584 | 17.2% |

| 2016 | 80,226 | +6,606 | 18.5% |

| 2017 | 82,902 | +2,676 | 19% |

| 2018 | 87,819 | +4,917 | 20.1% |

| 2019 | 100,205 | +12,386 | 22.9% |

| 2020 | 103,895 | +3,690 | 23.8% |

| 2021 | 108,519 | +4,624 | 24.7% |

| 2022 | 112,843 | +4,324 | 25.5% |

| 2023 | 114,150 | +1,307 | 25.6% |

| 2024 | 118,817 | +4,667 | 26.3% |

| 2025 (ROGS) | 118,425 | −392 | n/a |

Section 04 · State breakdown

Which state has the most community housing?

New South Wales had 52,439 community housing tenancy rental units at June 2025, accounting for about 44% of national community housing stock. Growth varied widely between jurisdictions from 2016 to 2025, ranging from 2.7% in Western Australia to 142.9% in the Northern Territory.

NSW leads Australia for community housing stock

New South Wales held 52,439 TRU at 30 June 2025, ahead of Victoria (19,625) and Queensland (13,158). Tasmania's community housing (10,430 TRU) now exceeds its public housing stock (5,051 dwellings), the largest community-to-public ratio of any jurisdiction.

Community housing TRU by state, at 30 June 2025

NSW holds 44% of national stock; Tasmania's community housing now exceeds its entire public housing count.

NSW

Source: Productivity Commission, ROGS 2026, Table 18A.3; AIHW Table DWELLINGS.2 (2025 release).

South Australia and Queensland had similar-sized community housing sectors at June 2025, with 13,010 TRU in South Australia and 13,158 TRU in Queensland. Western Australia added 202 TRU between 2016 and 2025, an increase of 2.7% — the smallest absolute increase of any state over the period.

Tasmania's community housing system is now more than double its public housing stock, with 10,430 community housing TRU compared with 5,051 public housing dwellings at June 2025. This follows the transfer of approximately 2,000 public housing dwellings to community housing provider management in 2021–22.

| State / territory | TRU (June 2025) | TRU (June 2016) | Change | % change |

|---|---|---|---|---|

| NSW | 52,439 | 32,266 | +20,173 | +62.5% |

| VIC | 19,625 | 14,236 | +5,389 | +37.9% |

| QLD | 13,158 | 11,679 | +1,479 | +12.7% |

| SA | 13,010 | 7,472 | +5,538 | +74.1% |

| TAS | 10,430 | 6,076 | +4,354 | +71.7% |

| WA | 7,611 | 7,409 | +202 | +2.7% |

| ACT | 1,246 | 715 | +531 | +74.3% |

| NT | 906 | 373 | +533 | +142.9% |

| Australia total | 118,425 | 80,226 | +38,199 | +47.6% |

NSW TRU was 54,412 at June 2024 in the AIHW data and 52,439 at June 2025 in the ROGS data. Source: Productivity Commission, ROGS 2026, Table 18A.3.

≡Community housing TRU by state, 2016 to 2025Annual data, 10 years

| Year | NSW | VIC | QLD | WA | SA | TAS | ACT | NT | Total |

|---|---|---|---|---|---|---|---|---|---|

| 2016 | 32,266 | 14,236 | 11,679 | 7,409 | 7,472 | 6,076 | 715 | 373 | 80,226 |

| 2017 | 34,398 | 14,278 | 11,512 | 7,847 | 7,484 | 6,115 | 883 | 385 | 82,902 |

| 2018 | 35,345 | 14,486 | 11,116 | 8,062 | 11,561 | 5,980 | 895 | 374 | 87,819 |

| 2019 | 46,557 | 15,081 | 10,941 | 7,968 | 11,622 | 6,698 | 907 | 431 | 100,205 |

| 2020 | 49,509 | 14,857 | 11,054 | 8,005 | 12,151 | 6,919 | 936 | 464 | 103,895 |

| 2021 | 53,233 | 14,996 | 11,439 | 7,997 | 12,387 | 7,019 | 970 | 478 | 108,519 |

| 2022 | 54,292 | 16,159 | 11,524 | 7,718 | 12,430 | 9,267 | 958 | 495 | 112,843 |

| 2023 | 53,913 | 16,363 | 11,665 | 7,978 | 12,333 | 9,715 | 1,695 | 488 | 114,150 |

| 2024 | 54,412 | 18,191 | 12,548 | 8,012 | 13,048 | 10,139 | 1,736 | 731 | 118,817 |

| 2025 | 52,439 | 19,625 | 13,158 | 7,611 | 13,010 | 10,430 | 1,246 | 906 | 118,425 |

Section 05 · Sector structure

Fewer community housing providers are managing more homes

The number of reporting community housing organisations fell by 25% between 2016 and 2024, from 704 to 531. Over the same period, total community housing stock grew by 48%. Average portfolio size also increased, from approximately 114 dwellings per reporting provider in 2016 to approximately 224 in 2024.

Community housing providers manage 200 or more dwellings

In 2024, 89 reporting organisations managed 200 or more dwellings — 16.8% of all reporting organisations. By contrast, 305 providers managed fewer than 20 dwellings each, representing 57.4% of all reporting organisations.

Community housing providers by portfolio size, Australia, 2024

305 of 531 providers manage fewer than 20 dwellings; 89 manage 200 or more and hold most development and delivery capacity.

Source: AIHW, Housing assistance in Australia, Table DWELLINGS.11 (2025 release).

| Provider size | Number | Share | Capacity context |

|---|---|---|---|

| Less than 20 | 305 | 57.4% | Small specialist or local providers; limited development capacity |

| 20 to 99 | 104 | 19.6% | Mid-scale providers; focused on one community or programme type |

| 100 to 199 | 33 | 6.2% | Regional or niche providers with developing capacity |

| 200 or more | 89 | 16.8% | Large CHPs; hold most development and HAFF/NHAF delivery capacity |

| Total | 531 | 100% |

Number of community housing organisations, Australia, 2014 to 2024

Provider numbers peaked at 715 in 2014, fell to 492 by 2020, and rose to 531 by 2024.

Source: AIHW, Housing assistance in Australia, Table DWELLINGS.11 (2025 release).

Section 06 · Policy rationale

Why governments use community housing providers

Government net recurrent expenditure on community housing was $5,024 per household in 2024–25, compared with $15,510 per public housing household. This difference reflects the way each programme is funded and should not be read as a direct comparison of service costs.

01

Commonwealth Rent Assistance access

Community housing tenants can receive Commonwealth Rent Assistance, while public housing tenants generally cannot. In 2024, around 89,600 households in community housing were receiving CRA. This payment forms part of the rent paid to the provider, but it is not recorded as state or territory housing expenditure.

02

Private and institutional finance

Larger community housing providers can borrow against their property portfolios and raise funds through private markets. This can help fund additional housing projects alongside government grants, concessional finance, land contributions and other public support.

03

Ownership, management and maintenance responsibilities

Maintaining public housing is an ongoing cost for state and territory governments. Where homes are transferred to community housing providers, some ownership, management or maintenance responsibilities may also move to the provider, depending on the terms of the transfer.

Government spending figures are not a like-for-like cost comparison

Government recurrent spending per public housing household was $15,510 in 2024–25. This covers management, maintenance and tenancy services, but excludes capital construction. The equivalent figure for community housing was $5,024 — direct grants and subsidies to providers, excluding CRA paid to tenants and private financing carried by providers.

Public housing

$15,510

net recurrent per household, 2024–25

Community housing

$5,024

net recurrent per household, 2024–25

Section 07 · Tenants

Who lives in community housing in Australia?

At 30 June 2024, 92.1% of Australia's 107,637 community housing households were on low incomes, and 78.8% had a government payment as their main income source. Compared with public housing tenants, community housing tenants were more likely to be under 35 and less likely to have a disability.

Classified as low income

92.1%

vs 96.0% in public housing

Main income: govt payment

78.8%

vs 85.8% in public housing

Main income: employment

11.5%

vs 6.6% in public housing

With a disability

29.0%

vs 42.3% in public housing

| Characteristic (main tenant, 2024) | Community housing | Public housing |

|---|---|---|

| Household composition | ||

| Single adult households | 62.5% | 58.1% |

| Sole parent with dependent children | 10.7% | 13.0% |

| Age of main tenant | ||

| Aged 55 years or over | 49.8% | 59.1% |

| Aged 65 years or over | 29.8% | 36.4% |

| Under 35 years | 15.2% | 10.1% |

| Income and disadvantage | ||

| Classified as low income | 92.1% | 96.0% |

| Main income: government payment | 78.8% | 85.8% |

| Main income: employment | 11.5% | 6.6% |

| With a disability | 29.0% | 42.3% |

| Indigenous status | 10.7% | 14.2% |

| Female main tenant | 60.4% | 63.0% |

Dwelling suitability in community housing

In 2024, 3.6% of community housing households with suitability data were in overcrowded dwellings, compared with 4.6% of public housing households. Community housing also had a higher share of households in suitable or adequate dwellings, at 83.3% compared with 78.3% in public housing.

| Dwelling suitability (2024) | Community housing | Public housing |

|---|---|---|

| Overcrowded | 3.6% | 4.6% |

| Underutilised | 10.6% | 16.5% |

| Suitable or adequate | 83.3% | 78.3% |

| Unknown or not stated | 2.6% | 0.6% |

Section 08 · Expenditure

How much do governments spend on community housing?

State and territory governments spent $1.33 billion on community housing in 2024–25. This included $540.8 million in net recurrent expenditure and $790.3 million in capital expenditure. Capital spending was concentrated in Queensland and Victoria, which together accounted for $788.9 million of the $790.3 million national capital total.

State & territory government expenditure on community housing, 2024–25

$540.8 million net recurrent expenditure and $790.3 million capital expenditure. Public housing expenditure was $7.95 billion in the same year.

| State / territory | Net recurrent ($m) | Capital ($m) | Total ($m) |

|---|---|---|---|

| New South Wales | 101.3 | 0.1 | 101.4 |

| Victoria | 189.4 | 287.1 | 476.5 |

| Queensland | 103.9 | 501.8 | 605.7 |

| Western Australia | 12.6 | n/a | 12.6 |

| South Australia | 50.2 | 0 | 50.2 |

| Tasmania | 72.1 | 1.3 | 73.4 |

| ACT | 11.3 | 0 | 11.3 |

| Northern Territory | n/a | n/a | n/a |

| Australia total | 540.8 | 790.3 | 1,331.1 |

n/a means not reported to ROGS for 2024–25. WA and NT did not report community housing capital expenditure. Source: Productivity Commission, ROGS 2026, Table 18A.1.

CRA recipients in housing organisations, 2024

89,600

Approx. households receiving CRA in housing organisations

Rental stress: housing org CRA recipients

12.8%

In rental stress (rent above 30% of income)

Rental stress: private rental CRA recipients

50.5%

vs 12.8% in housing organisations

The lower rental stress rate for CRA recipients in housing organisations is likely influenced by rent-setting rules. Community housing rents are generally set as a share of household income rather than full market rent.

Section 09 · New supply pipeline

HAFF and NHAF new supply pipeline

As at November 2025, 18,650 homes had been contracted under the Housing Australia Future Fund and National Housing Accord Facility. Of these, 9,501 were under construction and approximately 1,432 had been completed.

HAFF and NHAF delivery pipeline, November 2025

Community housing providers are central to delivery. Round 3, targeting the remaining 21,350 homes, opened in January 2026.

Target (5 years)

40,000

20k social + 20k affordable

Contracted

18,650

279 projects; Rounds 1 & 2

Under construction

9,501

Among contracted projects

Completed

~1,432

Finished and tenantable

Scenario only: not all contracted homes will be classified as community housing TRU.

Social housing and affordable housing are counted differently

Social housing under HAFF and NHAF is priced at 25 to 30% of household income and reserved for people with the greatest need. Affordable housing through the same programmes is priced at around 80% of local market rent. Only social housing is counted in the national social housing data series.

Social housing rent

25–30%

of household income

Affordable housing rent

80%

approx. of local market rent

Section 10 · Limits and context

What are the limits of community housing growth?

UNSW City Futures research estimates that around 640,000 Australian households were without adequate housing in 2021, with projections rising to nearly 940,000 by 2041. The 40,000-home HAFF/NHAF target is large, but it remains small relative to these estimates of unmet housing need.

01 · Scale of need

The HAFF target addresses a fraction of estimated housing need

Based on UNSW City Futures / CHIA estimates, housing need is projected to reach nearly 940,000 households by 2041. The 40,000-home HAFF/NHAF target remains small relative to estimates of unmet housing need, but the two figures are not directly comparable because the target includes both social and affordable housing.

02 · Construction capacity

Delivery capacity is concentrated among large providers

Most development capability sits with the 89 largest providers. Smaller and mid-tier CHPs often lack the in-house expertise to manage large construction projects. Large housing projects can be affected by construction costs, financing conditions and delivery timelines.

03 · Private financing exposure

Private debt introduces interest rate and project risk

The ability to use private finance is also a source of risk. CHPs borrowing to fund construction are exposed to interest rate changes and construction cost overruns in ways that state housing authorities are not.

04 · Social vs affordable distinction

Half the HAFF pipeline may not appear in social housing statistics

Half of the 40,000 HAFF/NHAF target homes are affordable housing, charged at around 80% of market rent rather than as a share of household income. These are not counted in the social housing data series.

05 · Public subsidy remains essential

The CHP model reduces but does not remove government funding requirements

CRA, capital grants, concessional finance, planning concessions, and land contributions all play a role in making community housing viable. Below-market rents require ongoing subsidy, regardless of who manages the properties.

Section 11 · Frequently asked questions

Common questions about community housing in Australia

Australia had 118,817 community housing tenancy rental units (TRU) at 30 June 2024, of which 107,637 were occupied. The most recent figure (June 2025) is 118,425 TRU. TRU counts households, not buildings: one house split into two tenancies counts as two TRU but one dwelling.

General information only

This article draws on publicly available data from the Australian Institute of Health and Welfare and the Productivity Commission. It is general information only and does not constitute financial, investment, or housing advice. Figures are from official government data releases and may be updated in future. Housing need estimates come from UNSW City Futures and CHIA research, which uses different methods from official government counts.

Australian Institute of Health and Welfare, Housing assistance in Australia 2025 (AIHW HOU 342): supplementary data tables DWELLINGS.1, DWELLINGS.2, DWELLINGS.11, HOUSEHOLDS.1, HOUSEHOLDS.4, SUITABILITY.1, CRA.8.

Productivity Commission, Report on Government Services 2026, Part G Section 18 Housing: Tables 18A.1, 18A.3.

Housing Australia, HAFF and NHAF Rounds 1 and 2 contract update, November 2025.

UNSW City Futures / CHIA, Housing need national snapshot.

Chart Snapshots