Australian building material costs: how much prices have increased since 2020

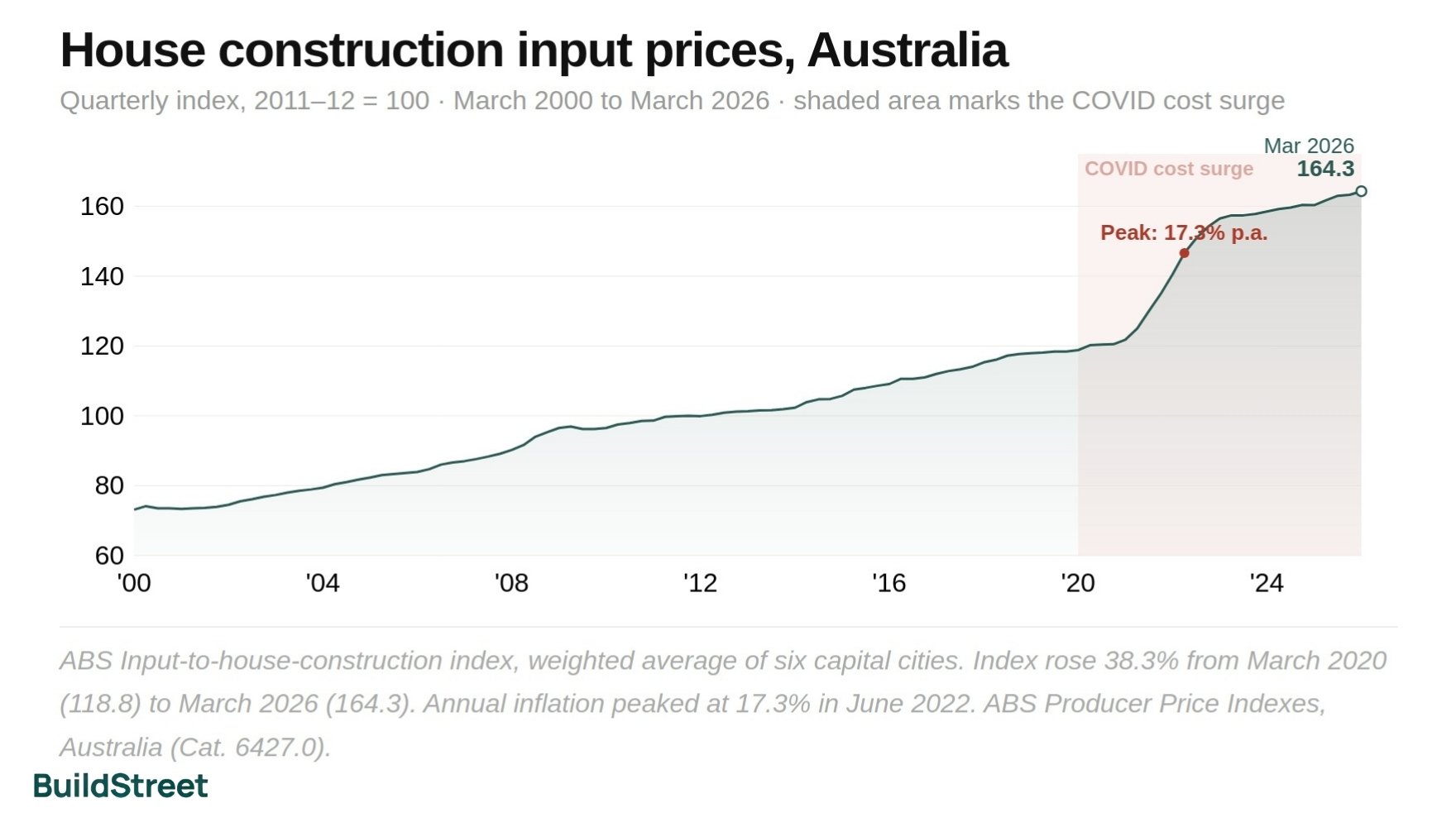

Building material costs in Australia are 38.3% higher than in early 2020, even though annual price growth has slowed sharply. ABS data shows annual inflation peaked at 17.3% in mid-2022 before easing to 2.5% in the March 2026 quarter. Prices have stabilised, but they have not returned to pre-pandemic levels, leaving builders, buyers and developers working from a much higher cost base.

Cumulative rise since March 2020

+38.3%

Input-to-house-construction index, Mar 2020 to Mar 2026 (ABS PPI)

Annual inflation rate

2.5%

Year-on-year change, March quarter 2026; peak was 17.3% in June 2022

Fastest-rising item this quarter

+14.5%

Copper pipes and fittings, March quarter 2026; electric cable +9.2%

SECTION 01 · INFLATION RATE

Are building material costs still rising in Australia?

Building material costs are still rising, but much more slowly than during the pandemic cost surge.

Building material input costs rose 2.5% over the year to March 2026, with a quarterly increase of 0.6% in the March quarter. That annual rate is well below the sustained double-digit growth of 2021 and 2022, and roughly in line with pre-pandemic norms.

The pace of change shifted quickly from its peak. Annual inflation hit 17.3% in June 2022, then declined steadily through 2023 and 2024, reaching a low of 1.1% in June 2024 and again in March 2025 before edging back up to 2.5% by March 2026.

The March 2025 quarter was the first quarterly decline since 2012, with input costs falling 0.1% as timber and steel prices eased. That pause was brief, with costs rising again in later quarters.

House construction input prices, Australia

Quarterly index (2011–12 = 100) and year-on-year percentage change, March 2000 to March 2026

Methodology: ABS "Input to house construction" index, weighted average of six capital cities. Annual % change calculated from quarterly index values. Source: ABS Producer Price Indexes, Australia, March 2026.

Recent quarterly data show steady but modest growth. After the −0.1% dip in March 2025, the index rose 0.9% in June, 0.8% in September, 0.2% in December, and 0.6% in March 2026. The annual rate for the twelve months to March 2026 was 2.5%, compared with 17.3% in the year to June 2022.

| Quarter | Index value | Quarterly change | Annual change |

|---|---|---|---|

| Dec 2024 | 160.4 | +0.5% | +1.6% |

| Mar 2025 | 160.3 | -0.1% | +1.1% |

| Jun 2025 | 161.7 | +0.9% | +1.6% |

| Sep 2025 | 163.0 | +0.8% | +2.1% |

| Dec 2025 | 163.3 | +0.2% | +1.8% |

| Mar 2026 | 164.3 | +0.6% | +2.5% |

Source: ABS Producer Price Indexes, Australia, March 2026. Index reference 2011–12 = 100.

How much have building material costs increased in Australia?

Building material input costs rose 38.3% between March 2020 and March 2026, increasing from an index value of 118.8 to 164.3. Most of the rise happened between 2021 and mid-2022. Since March 2023, the index has increased by only 5.0%, showing that cost growth has slowed sharply. Annual inflation was 2.5% in the March 2026 quarter, down from a peak of 17.3% in June 2022 and close to the pre-pandemic average.

SECTION 02 · SINCE 2020

How much have building material costs increased since 2020?

Building material input costs rose 38.3% between March 2020 and March 2026, from an index value of 118.8 to 164.3. Most of that increase was concentrated in a two-year window. Between March 2020 and June 2022 alone, costs climbed 23.4%. From June 2022 to March 2026, the index added a further 17.7 points, but spread across almost four years.

The 2022 calendar year recorded an annual average change of 15.7%, the highest in the 2000 to 2026 series. By 2024 and 2025, that rate had returned to 1.4% and 1.7% respectively, both below the pre-pandemic 10-year average of 2.1%.

The key qualification is that a lower inflation rate does not mean lower costs. Builders, buyers and project managers are working from a cost base that is roughly 38% above pre-pandemic levels, and that elevated baseline has not reversed.

| Year | Annual average index | Annual average change |

|---|---|---|

| 2016 | 110.3 | +2.7% |

| 2017 | 113.0 | +2.4% |

| 2018 | 116.6 | +3.1% |

| 2019 | 118.2 | +1.4% |

| 2020 | 120.0 | +1.5% |

| 2021 | 127.9 | +6.6% |

| 2022 | 148.0 | +15.7% |

| 2023 | 157.3 | +6.3% |

| 2024 | 159.4 | +1.4% |

| 2025 | 162.1 | +1.7% |

Methodology: Annual averages calculated from quarterly ABS index values. Source: ABS Producer Price Indexes, Australia, March 2026 and March 2021 releases.

SECTION 03 · MATERIALS BREAKDOWN

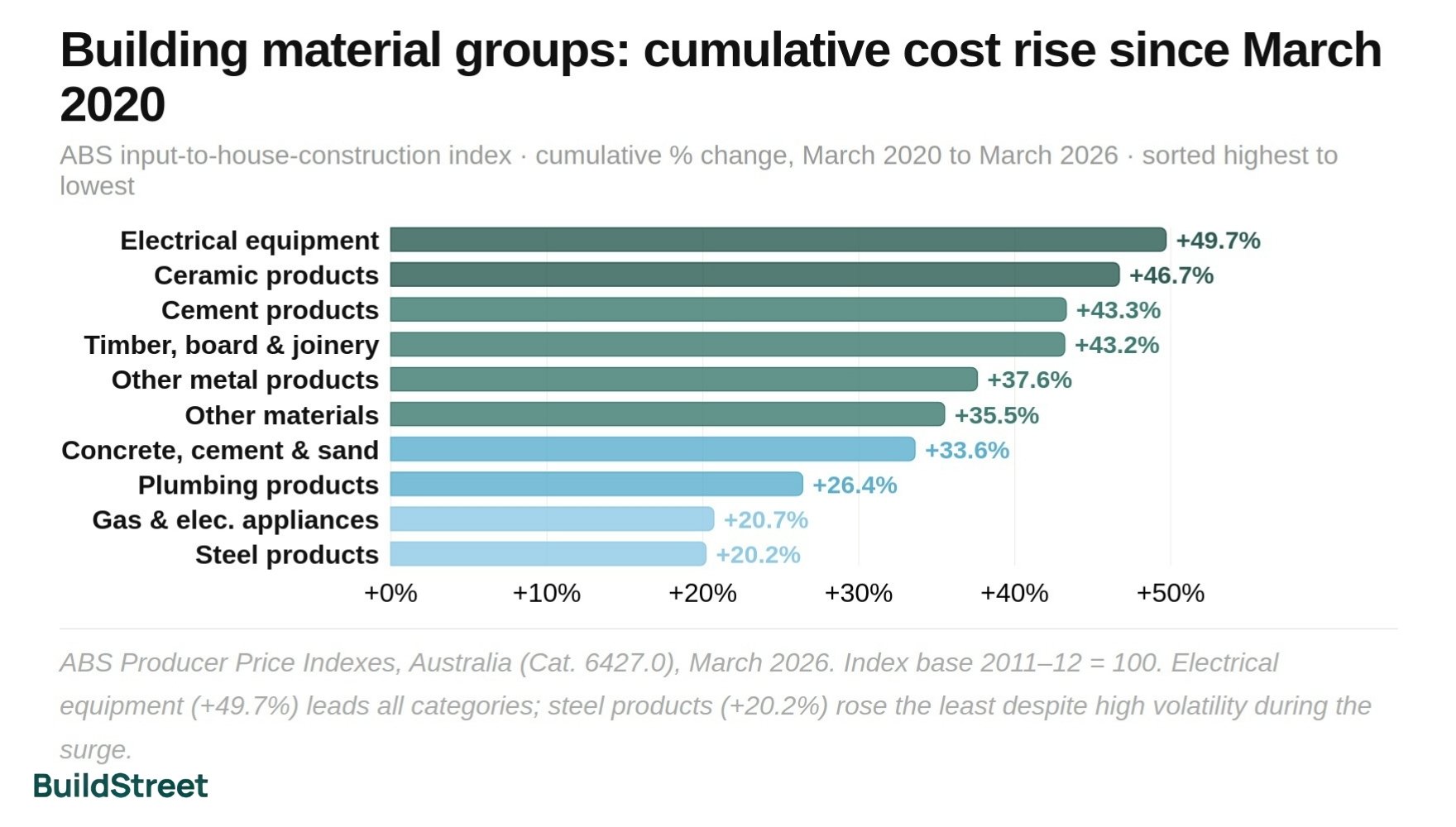

Which building materials have increased the most?

Copper pipes and fittings were the fastest-rising material in the March quarter 2026, up 14.5% for the quarter. Electric cable and conduit rose 9.2% over the same period.

The inflation profile has changed significantly since 2020. Timber and steel were the main pressure points in 2021 and 2022, but both have eased. Copper-linked products and concrete are now contributing more to ongoing cost pressure.

Building material input price changes by category

Quarterly change (March quarter 2026) vs full-year change (calendar year 2025) for key input groups

Electrical equipment

Methodology: Quarterly figures are ABS-reported percentage changes for selected input categories in the March quarter 2026. Full-year 2025 figures are from the NHSAC State of the Housing System 2026, drawing on ABS PPI data. Source: ABS Producer Price Indexes, Australia, March 2026; NHSAC State of the Housing System 2026.

Timber prices

Timber was one of the clearest pandemic-era pressure points. By the March quarter 2022, timber, board and joinery had risen 20.6% over the year, driven by supply shortages amplified by demand from the federal HomeBuilder programme and state construction grants. That pressure has since eased. In the March quarter 2026, the timber, board and joinery group fell 0.2% for the quarter, although it remained 2.8% higher than a year earlier.

Steel and rebar prices

Steel products shifted from a major inflation driver in 2021 and 2022 to a disinflationary force by 2023. Steel product prices fell 4.4% in the March quarter 2023 and were down 6.2% over the year by the March quarter 2025. They fell 4.6% over the full year 2025 and had largely stabilised by the March quarter 2026.

Concrete and cement costs

Concrete and cement have remained a steadier source of inflation. In the March quarter 2026, concrete, cement and sand rose 1.7% for the quarter and 2.8% over the year, driven by ready-mixed concrete price increases. Over the full year 2025, the same category rose 1.6%. Sustained infrastructure construction activity continues to support demand for concrete.

Copper, plumbing and electrical material costs

Copper-linked products are the standout cost driver in the March quarter 2026. Copper pipes and fittings rose 14.5% for the quarter, while electric cable and conduit rose 9.2%, both driven by higher copper prices. At the group level, electrical equipment rose 5.0% in the quarter, making it the largest single-group contributor. Other metal products rose 1.5% for the quarter.

Building material groups: change since March 2020

ABS input-to-house-construction index. Weighted average of six capital cities.

- Mar 2026

- Mar 2020

Electrical equipment

Methodology: Percentage change calculated from March 2020 to March 2026 index values. Index reference period 2011–12 = 100.0. Source: ABS Producer Price Indexes, Australia, March 2026.

SECTION 04 · DRIVERS

What caused Australia's building material cost surge?

Building material input costs rose 23.4% between March 2020 and June 2022, driven by a combination of demand and supply pressures that arrived simultaneously and reinforced each other. Multiple factors converged during that period, shifting the cost base to levels from which it has not retreated.

Demand-side stimulus

The federal HomeBuilder programme and state government grants created a surge in new residential construction at exactly the point when global supply chains were already under stress. More dwellings were being ordered and started than the industry could efficiently deliver.

Supply chain disruption and freight costs

Global shipping delays and high international freight costs increased the cost of imported materials, particularly timber. Shipping delays and freight costs were cited directly in commentary from 2022 as contributors to quarterly input price growth.

Timber shortages

Shortages of structural timber, combined with higher global demand and pandemic-era sawmill disruptions, pushed timber prices up sharply. Timber shortages were identified as a specific contributor in multiple quarterly releases from 2021 to 2022.

Energy costs and metals inflation

Rising energy prices raised production costs for energy-intensive materials, including steel, aluminium and concrete. ABS commentary from 2023 identified high energy and transport costs as ongoing contributors to input price growth, even after the initial surge had eased.

Trade shortages and build delays

Labour shortages meant builders could not schedule work efficiently. Housing Australia's State of the Nation's Housing 2022–23 reported that around 28,000 dwellings were delayed. Builders also made cost allowances of up to 40% for unexpected delays, compared with a more typical 20%. Those delay costs flowed through to final prices.

SECTION 05 · CITIES AND STATES

States and cities with the highest building cost pressure

Building cost pressure varies by location and by measure. City-level input prices show changes in material costs, while state-level output prices show what builders charge for new house construction. Adelaide recorded the highest annual input cost increase of any capital city in the year to March 2026, at 3.7%. Brisbane followed at 3.0%.

At state level, Tasmania and Western Australia recorded the strongest builder-side price growth. House construction output prices rose 8.8% in Tasmania and 6.3% in Western Australia.

Input prices show what builders pay for materials in each city. Output prices show what builders charge for new house construction, including labour, margins and other costs. The two measures can diverge, particularly in states with tight labour markets or strong demand.

Input prices by capital city

Among the six sampled capital cities, Adelaide recorded the highest annual input cost increase in the year to March 2026 at 3.7%, followed by Brisbane at 3.0%. Sydney and Melbourne were level at 2.6%. Perth posted the lowest annual increase at 1.2%, notable given its strong construction activity. Quarterly, Hobart recorded the highest city gain at 2.3% in the March quarter 2026.

On a cumulative basis since March 2020, the differences narrow: Brisbane's input costs have risen 40.5% and Sydney's 34.7%, with the other cities clustered between 39% and 40%.

Annual change in input prices by city, selected quarters

Year-on-year percentage change, ABS input-to-house-construction index.

- Mar 2026

- Dec 2025

- Sep 2025

Adelaide

Methodology: Year-on-year percentage change published by ABS for the input-to-house-construction index by capital city. Index reference 2011–12 = 100. Source: ABS Producer Price Indexes, Australia, March 2026.

Output prices by state

Builder-side price pressure is strongest in Tasmania and Western Australia. Tasmania's house construction output prices rose 8.8% in the year to March 2026, the highest of any state, while WA posted 6.3%, both attributed to sustained demand. The national average annual change for house construction output was 4.1%, roughly double the input-price inflation rate.

On a cumulative basis, the difference since March 2020 is more pronounced. Western Australia's house construction output prices have risen 97.7%, almost doubling over six years. Tasmania recorded the next-largest increase at 60.6%, followed by South Australia at 59.0% and Queensland at 57.7%. Victoria recorded the smallest cumulative rise at 33.3%.

Annual change in house construction output prices by state

Year-on-year percentage change, ABS 3011 House construction output index.

- Mar 2026

- Dec 2025

- Sep 2025

TAS

Methodology: Annual change calculated from index values for same quarter in prior year. Subdivision 3011 covers house construction only. NT data should be interpreted with caution given smaller sample size. Source: ABS Producer Price Indexes, Australia, March 2026.

Western Australia's house construction output prices have risen 97.7% since March 2020. That is by far the largest cumulative increase of any state, reflecting sustained demand and the geographic and logistical factors that can amplify material and freight costs in WA.

| State | Output index (Mar 2026) | Annual change | Cumulative since Mar 2020 |

|---|---|---|---|

| Tasmania | 192.2 | +8.8% | +60.6% |

| Western Australia | 214.1 | +6.3% | +97.7% |

| South Australia | 173.8 | +4.1% | +59.0% |

| Australia (national) | 179.0 | +4.1% | +47.4% |

| Queensland | 193.2 | +3.9% | +57.7% |

| Victoria | 163.5 | +3.7% | +33.3% |

| ACT | 163.6 | +3.5% | +49.1% |

| New South Wales | 189.3 | +3.4% | +38.5% |

| Northern Territory | 130.8 | +2.8% | +18.3% |

Source: ABS Producer Price Indexes, Australia, March 2026. ABS subdivision 3011 House construction. Annual change calculated from March 2025 and March 2026 index values. Cumulative change from March 2020 to March 2026. Index reference 2011–12 = 100.

SECTION 06 · NEW HOME BUILDING

How do material costs affect new home prices?

New dwelling prices charged to owner-occupiers rose 4.5% over the year to March 2026. That outpaced the input-only inflation rate of 2.5%. House construction output prices rose 4.1% over the same period.

The gap reflects the additional weight of labour costs, builder margins and financing conditions, which sit on top of materials in the final price. Builders faced continued pressure in securing bricklayers, carpenters and concreters during the March quarter, alongside shortages of bricks, pavers and sand. That combination of labour and material tightness feeds through directly to prices charged to owner-occupiers contracting to build a new home.

On a cumulative basis, the output-of-building-construction index rose from 116.0 in March 2020 to 161.1 in March 2026, a gain of 38.9%. This closely tracked the increase in input costs over the same period. Even where individual materials, such as steel, have fallen recently, overall residential construction prices remain far above 2020 levels.

New dwellings CPI (Mar 2026)

+4.5%

Year-on-year; prices charged to owner-occupiers

Building construction output (Mar 2026)

+4.2%

Year-on-year; PPI output measure

House construction output (Mar 2026)

+4.1%

Year-on-year; PPI series 3011

Output index since Mar 2020

+38.9%

Cumulative rise in builder output prices (116.0 to 161.1)

Source: ABS Producer Price Indexes, Australia, March 2026; ABS Consumer Price Index, Australia, March 2026.

SECTION 07 · HOUSING TARGET

Why construction costs matter for the 1.2 million homes target

Construction costs matter for the National Housing Accord because they affect whether approved homes can move through to commencement and completion.

Since the Accord began in July 2024, building approvals and commencements have both risen by about 17%. More than 219,000 homes were completed over the first five quarters of the Accord. However, the NHSAC estimates that roughly 980,000 homes will be delivered over the full five-year period, below the 1.2 million target.

The NHSAC's annual housing assessment modelled two construction cost shock scenarios linked to geopolitical instability. A 6% peak increase in construction costs could reduce completions by 10,000 homes by mid-2029. A 10% peak increase could reduce completions by 33,000 homes. At the time of the NHSAC's March 2026 Quarterly Report, real construction costs were 0.9% lower than when the Accord began. However, the annual assessment remains more cautious about the outlook.

ABS pipeline data shows the current gap between approvals and completions. In March 2026, total dwelling approvals were 17,300 seasonally adjusted, up 13.1% from a year earlier. In the December quarter 2025, commencements rose to 53,567, but completions were 43,536, down 3.9% over the year. There were 236,858 dwellings under construction at the end of that quarter.

Why the gap between approvals and completions matters

Approvals count homes that have permission to be built. Commencements count homes where construction has started. Completions count homes that are finished and ready to occupy. A large under-construction stock of 236,858 dwellings means many approved and started homes are not yet adding to the housing supply. Material costs, labour availability and financing conditions all affect how quickly those homes are completed.

SECTION 08 · OUTLOOK

What building cost trends mean in 2026

Builder-side prices are rising at 4.1% to 4.5% annually, roughly double the materials-only rate. This is because labour costs, trades availability and builder margins also feed into the final price of a new home. The cost base set during 2022 has not reversed. In 2026, construction quotes typically reflect costs that are around 38% to 40% above 2020 levels.

Three conclusions follow from the data.

Material cost inflation has slowed. A repeat of the 2021 and 2022 materials shock is not the base case. Current pressure is narrower, led mainly by copper-linked products and concrete rather than the broad-based timber, steel and energy surge seen in 2021 and 2022.

Builder-side prices are still rising faster than material inputs. Output prices are up 4.1% to 4.5% annually, compared with 2.5% for inputs. Monthly CPI data also shows that prices charged to owner-occupiers for new homes continue to increase.

The higher cost base remains in place. Construction quotes in 2026 are likely to reflect costs that are roughly 38% to 40% above 2020 levels, even though the rate of further increase has slowed.

Lower risk

Annual input inflation (2.5%) is near its pre-pandemic average. Timber and steel are not adding significant pressure. Material-only cost escalation is unlikely to reproduce the 2022 shock absent a major external event.

Ongoing pressure

Copper-linked costs are rising sharply and feeding through to electrical and plumbing components. Concrete remains elevated. Labour costs and trades availability continue to push output prices above the input-price benchmark.

Key risk

The NHSAC has modelled scenarios in which a 6–10% construction cost shock (from geopolitical disruption or commodity price moves) could cut housing completions by 10,000 to 33,000 through to mid-2029, adding pressure to an already constrained supply pipeline.

Monthly CPI data on new dwellings provide a useful near-term indicator. New dwelling prices rose 3.5% over the year in January 2026, 3.7% in February and 4.5% in March. The rise in March 2026 suggests builder pricing has not settled, even as the materials-only measure remains comparatively contained.

For the construction sector, the main pricing risk in 2026 is no longer broad-based materials inflation. It is volatility in specific categories, particularly in copper-linked plumbing and electrical products, combined with ongoing labour and subcontractor cost pressure. Quotes should allow for targeted escalation in those categories rather than assuming all materials are rising at a uniform rate.

General information only

This article draws on publicly available data from the ABS, NHSAC, Housing Australia and Treasury. It is intended as a reference and data summary and does not constitute financial or construction advice. Where percentage changes are calculated from index values, the methodology is described in the accompanying footnotes. Data reflects the most recently published releases available as of the page's last updated date and may subsequently be revised by the source.

ABS Producer Price Indexes, Australia, March quarter 2026

ABS Producer Price Indexes, Australia, March quarter 2025

ABS Producer Price Indexes, Australia, March quarter 2024

ABS Producer Price Indexes, Australia, March quarter 2023

ABS Producer Price Indexes, Australia, March quarter 2022

ABS Producer Price Indexes, Australia, March quarter 2021

ABS Consumer Price Index, Australia, March quarter 2026

ABS Building Approvals, Australia, March 2026

NHSAC State of the Housing System 2026

Housing Australia State of the Nation's Housing 2022–23

Treasury National Housing Accord

Cumulative and annual percentage change calculations are derived from the ABS quarterly index series and are not separately published in the source releases.

Chart Snapshots