What the post-2020 cost surge means for homebuilding in Australia

House construction prices in Australia surged 40.8% between September 2020 and June 2024, according to ABS producer price data for house construction. That increase has permanently reset the cost baseline. In 2026, new dwelling prices continued to rise, with the annual CPI rate reaching 3.7% by February.

The double-digit increases of 2021 and 2022 have since eased, but they've stacked onto a cost base that was already at a historic high. Prices are unlikely to return to 2019 levels. For anyone building now, the real question is knowing which pressures have genuinely eased, which ones are here to stay, and where the next shocks are likely to come from.

House construction PPI surge (Sep 20 – Jun 24)

+40.8%

Fastest residential escalation on ABS record

Current annual rate (Feb 2026)

+3.7%

16-month high · ABS CPI housing component

Construction insolvencies (FY to Feb 2026)

1,894

Sector ranked #1 for insolvencies 3 yrs running

Why construction costs surged after 2020

The HomeBuilder stimulus launched in 2020 at exactly the wrong moment. It pushed a flood of consumer spending into the residential sector just as global supply chains were breaking down. Structural timber doubled in price within months. Steel followed. Freight rates hit records. Builders who had signed fixed-price contracts before the surge watched their margins disappear entirely. Construction became the top sector for corporate insolvencies, a position it hasn't given up since 2022.

Copper prices are rising and adding pressure

With timber finally settling down, the next major input shock for the construction industry is copper. Prices passed US$13,000 per tonne in early 2026, a 16.5% rise year-on-year. This isn't a temporary supply chain problem. It's structural demand driven by global electrification, renewable energy grids and AI data centres. Industry forecasters are expecting at least two more price rises in electrical cabling before the end of 2026.

Section 01 · The Cost Reset

Why have construction costs in Australia risen so sharply after 2020?

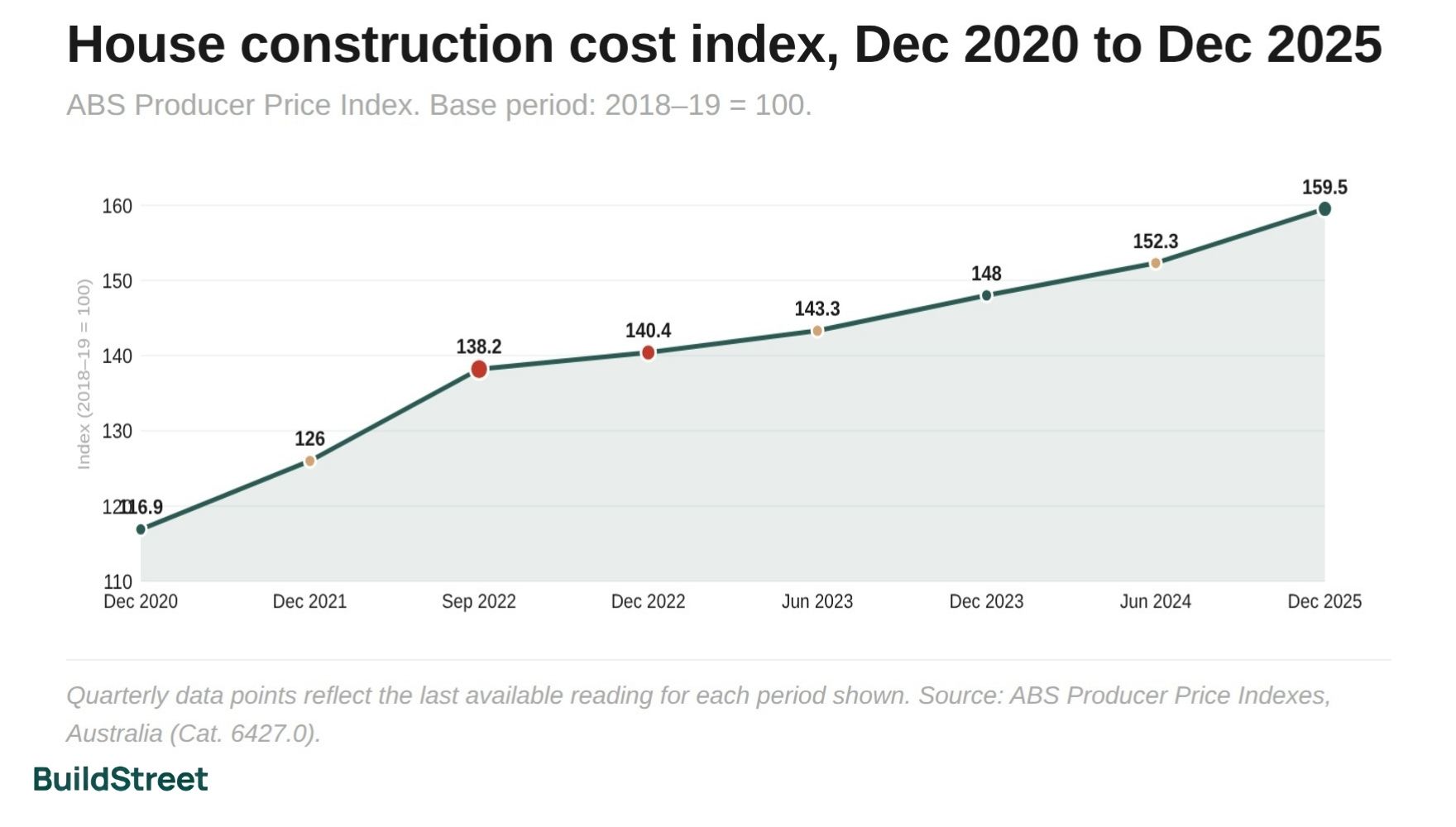

Australia's homebuilding cost base did not just rise after 2020. It reset. What had been a relatively steady pattern of price growth gave way to a sharp and sustained escalation, driven by stimulus-fuelled demand, supply chain disruption, labour shortages and higher risk pricing across the sector. The ABS Producer Price Index for house construction tracks the prices building businesses receive for their work, capturing not only materials but also labour, contractor margins and risk pricing. Between 2006 and 2019, the index rose at a relatively steady pace of about 3.4% a year. From 2020, that stability broke down. Three consecutive quarters of double-digit growth between mid-2021 and late 2022 pushed costs higher at an extraordinary pace. By December 2025, the index had reached 159.5, a 36.5% increase from 116.9 in December 2020.

ABS PPI for House Construction, index level: Dec 2020 to Dec 2025

Index base period: 2018–19 = 100. Quarterly data points reflect the last available reading for each period shown.

Methodology: Index base 2018–19 = 100. The most recent PPI reading available is December 2025 at 159.5. Separately, the ABS CPI housing component for February 2026 shows an annual rate of +3.7%, the fastest pace in 16 months, though this is a different measure to the PPI and is not plotted above. Source: ABS Producer Price Indexes, Australia (Cat. 6427.0); ABS Consumer Price Index, Australia (February 2026).

Pandemic onset. Temporary deflation fears gave way to massive fiscal stimulus. The HomeBuilder program launched, flooding demand into the sector.

Early supply shock. Global shipping constraints and initial material shortages started pushing input costs well above pre-pandemic norms.

Hyper-escalation. Timber and steel prices hit records. Labour mobility collapsed as trades were locked into backlogs across multiple states simultaneously.

Persistent inflation. Despite some supply chain easing, elevated costs entrenched themselves across the industry. Builder insolvencies began accelerating.

Disinflation phase. The growth rate began slowing, but was still compounding onto a base that had already surged more than 20% in two years.

Stabilisation. Builders absorbed costs through renegotiation. Domestic labour shortages replaced material price shocks as the primary pressure.

Secondary rebound. Public infrastructure projects began competing heavily with residential builders for concrete, steel and skilled labour.

Post-peak plateau. Growth slowed, but from a cost base that is now 36.5% above where it was in late 2020. The new normal is structurally more expensive.

Index base 2018–19 = 100. The most recent PPI reading available is December 2025 at 159.5. Separately, the ABS CPI housing component for February 2026 shows an annual rate of +3.7%, the fastest pace in 16 months, though this is a different measure to the PPI and is not plotted above. Source: ABS Producer Price Indexes, Australia (Cat. 6427.0); ABS Consumer Price Index, Australia (February 2026).

Section 02 · Sector Spend

The construction spend surge behind slower housing delivery

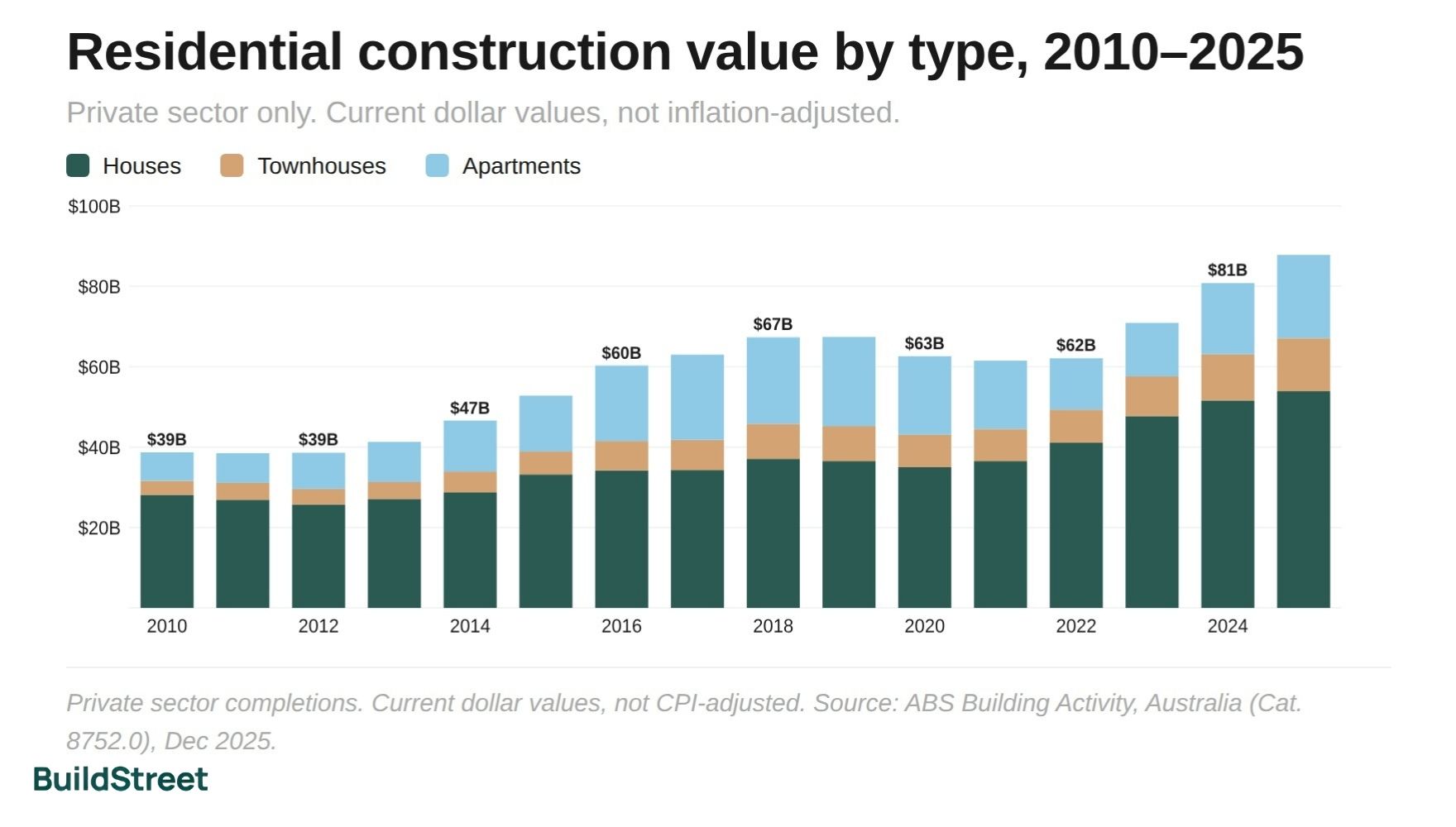

Australia spent more on residential construction in 2025 than at any point in recent years, but the increase says more about cost inflation than a building boom. The total nominal value of new residential construction completed reached $87.8 billion, up 40.2% from $62.6 billion in 2020. While that points to strong growth on paper, the underlying mix shows how much of the increase has come from higher costs rather than more homes being delivered. House construction remained the dominant segment at $53.9 billion, up 54% from 2020, despite detached housing completions shifting only marginally over the period. That makes the $18.9 billion increase overwhelmingly a cost story. Townhouses posted the fastest growth by dollar value, rising 62% since 2020. Apartments, however, remain in a different cycle. Spending has recovered from the 2021–22 trough, but it is still below the 2017 peak, with a depleted development pipeline continuing to suppress volumes.

Total value of new residential construction completed, 2010–2025 ($B)

Private sector only. Current dollar values, not inflation-adjusted.

Methodology: Values are not inflation-adjusted — a portion of every year-on-year increase reflects higher prices rather than more homes being built. Apartment values peaked nationally in 2017 at $21.2B and have not yet recovered to that level. Source: ABS Building Activity, Australia (Cat. 8752.0).

Section 03 · National Averages

What it actually costs to build: national averages over time

The nominal dollar value of construction tells one story, and the average cost of building an individual home tells another. Since 2020–21, the national average cost to build a new house has risen from $338,051 to $474,939 in 2024–25. Townhouses and apartments have followed a similar pattern. Crucially, average floor areas have not fallen enough to offset those cost increases. The average new house is slightly larger than it was in 2020–21, meaning Australians are paying more per square metre for roughly the same amount of space.

Average cost to build a new dwelling, national: 2014–15 to 2024–25

Per-dwelling average at completion. Excludes land, stamp duty and transaction costs.

Methodology: Apartment average is derived from NSW, VIC and QLD only, as other states and territories do not have sufficient completions volume for the ABS to publish reliable figures. Source: ABS Building Activity, Australia (Cat. 8752.0); ABS Characteristics of New Residential Dwellings.

House · National

$474,939

Townhouse · National

$435,089

Apartment · NSW/VIC/QLD

$567,947

Cost per m² is derived by dividing average build cost by average floor area for each financial year. Apartment floor area includes common areas and hallways divided across all dwellings in a building, which tends to inflate the per-m² figure relative to houses and townhouses. Source: ABS Building Activity, Australia (Cat. 8752.0); ABS Characteristics of New Residential Dwellings.

Section 04 · City Outlook

Not all cities are equal: Brisbane overheats while Sydney gets a brief breather

Construction cost pressures are no longer moving in lockstep across Australia. A clear two-speed market is emerging, with Brisbane and parts of Queensland accelerating sharply while Sydney and Melbourne experience a more moderate pace of escalation. Tender Price Index data, which captures what contractors actually charge for a job, including margins and risk premiums as well as material costs, points to a widening gap between the major east coast markets. At the heart of that divergence is infrastructure demand. In Queensland, large-scale projects are drawing trades and materials away from residential work, intensifying cost pressures in the housing sector.

Brisbane

2032 Olympics prep, $3.8B stadium and statewide energy rollout absorbing all available trades capacity.

Gold Coast

Olympics pipeline rapidly consuming skilled tradespeople across South East Queensland.

Townsville

Sustained defence and infrastructure demand creating extreme capacity constraint with no relief in sight.

Perth

Nation-leading population growth and Australia's most active detached housing market keeping pressure steady.

Adelaide

Major healthcare and defence projects entering peak construction, draining residential labour supply.

Darwin

Limited Tier 1 contractor competition and sustained federal defence infrastructure spending.

Canberra

Hospital and security precinct early works pulling trades away from the residential sector.

Melbourne

High baseline with builder insolvencies reducing some demand, but thinning competition at the same time.

Sydney

Temporary subcontractor availability improvement; affordability ceiling dampening new build demand.

TPI measures contractor pricing including margin and risk loading, making it a more forward-looking indicator than materials price indices alone. Forecasts reflect committed infrastructure pipelines and should be read as indicative ranges. Source: RLB Australia Market Intelligence Update Q1 2026; Altus Group, Australian Construction Price Outlook Q4 2025.

Sydney's relative slowdown is not a sign of a healthier market. Construction prices have climbed to a point where they're now suppressing demand, with builders holding quotes down just to win work. The current improvement in subcontractor availability is likely temporary. Once the major high-density pipelines and the Western Harbour Tunnel move into their active construction phases later in 2026, that breathing room will close quickly.

Section 05 · What's Eased

The good news: what's gotten cheaper since the 2022 peak

Not every cost input has kept rising. Several of the most acute pressures from 2021 and 2022 have genuinely eased, giving builders and buyers some real, if partial, relief:

- Global shipping and logistics. The worst of the disruption (container shortages, port backlogs and erratic international freight) has largely passed. Shipping costs have come back to normal, which removes one of the most unpredictable variables from builder cost estimates.

- Diesel prices. After hitting record highs and pushing up the cost of moving materials across Australia's long distances, diesel has fallen back to pre-pandemic levels. That feeds through into more stable logistics costs for building supplies.

- Structural timber. Timber, which forms the core of most Australian residential builds, is in a period of price stability in 2026. Domestic stockpiles are high, and competitively priced imported timber has eased pressure on framing quotes considerably.

Section 06 · Lingering Pressures

Why some construction costs are still climbing

The easing in timber and logistics has been partly offset by a different set of pressures, many of them structural rather than cyclical and unlikely to reverse quickly.

🔶

Copper price

US$13,000/t

+16.5% year-on-year. Electrical wiring, plumbing and HVAC all affected. At least two further cabling price rises expected in 2026.

👷

Labour wage target

+4% p.a.

Minimum union target across 2026 enterprise agreements. Trade shortages mean these targets are largely achievable across all states.

⚠️

Construction insolvencies

25%+ share

Of all 11,000 FY24 insolvencies. Up 34% year-on-year. Surviving builders price in sharply higher risk margins when competitors collapse.

Copper is especially disruptive because it tends to hit late in the build, when projects have the least flexibility to absorb additional costs. Because it sits at the centre of global electrification, renewable energy expansion and AI data centre construction, the pressure on copper prices appears structural rather than temporary. Labour conditions are similarly tight. With state governments simultaneously pushing ahead with hospitals, highways and housing, the conditions for wage pressure to ease are still not in place.

Section 07 · Cost of Money

How interest rates have changed the cost of building since 2020

Rising construction costs aren't the only burden on borrowers. The past five years have also brought the sharpest monetary policy tightening in over a decade, and for anyone borrowing to build, the monthly cost of carrying the debt has surged separately from what it costs to construct the home.

April 2020 · Pandemic baseline

April 2026 · Current

Monthly repayment estimates use principal and interest on a 25-year term. Actual repayments will vary by lender and loan structure. Source: RBA Statement on Monetary Policy, February 2026.

Higher construction costs and higher interest rates are compounding each other. A buyer who needed to borrow $730,000 in 2020 is now, in many cases, borrowing considerably more because the build itself costs more, while also servicing that larger debt at a rate roughly 300 basis points higher. The monthly gap isn't just $1,400. It's $1,400 on a loan that is itself significantly bigger than it would have been six years ago.

Section 08 · Adapting

Building smarter in 2026: modular construction and smaller homes are reducing cost pressures

Faced with unpredictable labour availability, material cost spikes, long delays and expensive finance, the Australian market is adapting. Two approaches are gaining real traction among cost-conscious buyers and developers.

Smaller, high-performance footprints. The old ambition of maximising floor area is giving way to the economics of 2026. Fewer square metres means fewer expensive trades, less material and a smaller exposure to cost blowouts. Passive house systems, which once added 15–20% to build cost, now typically add around 5–10% as local expertise and supply chains have caught up. That makes the trade-off between footprint and performance much easier to justify.

Modular and prefabricated construction. The Australian prefab market has grown by over 20% annually in recent years. Modules are built in climate-controlled factories while on-site preparation happens in parallel, cutting total timelines by 30-60%. The main benefit is cost certainty, arguably the single most valuable thing in a market where variation risk has become the norm.

Modular / Prefabricated

High cost certainty (fixed-price standard)

Minimal weather delays (built indoors)

30–60% faster than traditional

Welded steel chassis, often termite-proof

Low site impact (crane install, low waste)

~$380,000 fixed (150 m² 3BR example)

Traditional site-built

Low (prime cost and provisional sum exposure)

Frequent stoppages common

12–24 months typical

Timber or block frame, standard

Extended noise, waste and disruption

$400,000–$450,000+ variable

Cost estimates are indicative ranges and will vary significantly by location, specification and contractor. Source: S2A Modular, Modular vs Traditional Construction in 2026.

For buyers going ahead with a traditional build, industry professionals consistently recommend holding a 10–15% cash contingency buffer, kept liquid rather than borrowed, to cover the variation shocks that remain common in a structurally inflated market. With national costs forecast to rise a further 4.0–7.5% through 2026, depending on the city, every quarter of delay has a real dollar cost attached to it.

General information only

This article is based on publicly available ABS data and third-party forecasts. It is general information only and does not constitute financial or investment advice. If you are making decisions about saving for a property purchase, consider speaking with a licensed financial adviser.

ABS Producer Price Indexes, Australia, March 2026 (Cat. 6427.0)

ABS Building Activity, Australia, Dec 2025 (Cat. 8752.0)

ABS Insights into Output of Building Construction Prices

ABS Characteristics of New Residential Dwellings: 15-Year Summary

Altus Group, Australian Construction Price Outlook Q4 2025

RLB Australia Market Intelligence Update Q1 2026

CIE / HIA, Taxation's Major Impact on Housing (2025)

RBA Statement on Monetary Policy, February 2026

Scale Suite, Australian Business Insolvency by Industry 2026

S2A Modular, Modular vs Traditional Construction in 2026

Chart Snapshots