Why builder insolvencies increased after 2020

Construction company failures rose from 1,284 in FY2021-22 to 3,596 in FY2024-25, a 180% increase in three years. Construction remained the single largest industry for insolvency appointments and accounted for 24% of all appointments in the first eight months of 2025-26.

The surge was not a simple post-pandemic catch-up. It was the result of a chain reaction: a demand boom, a materials cost shock, fixed-price contracts that locked in prices before costs rose, and a cash-flow squeeze that took years to force companies into formal administration.

Construction insolvencies FY2024-25

3,596

Up from 1,284 in FY2021-22, a rise of 180%

Residential building construction

819

Up from 319 in FY2021-22, a rise of 157%

Share of all 2025-26 appointments

24%

Construction ranked number-one industry three years running

The chain reaction that drove failures

HomeBuilder stimulus and ultra-low interest rates increased demand for residential builders in 2020, just as global supply chains began to break down. Timber prices rose sharply, followed by steel. Builders locked into fixed-price contracts then faced higher input costs without the ability to fully pass them on. Margins narrowed, cash buffers weakened, and the financial pressure built before many companies entered formal insolvency.

Why insolvencies kept rising

Material cost pressures began easing from 2023, but builder insolvencies continued to rise. Labour costs remained elevated, the ATO resumed stronger enforcement of deferred tax debts from January 2024, and finance costs increased as the RBA raised interest rates. As larger builders adjusted or exited earlier, financial stress increasingly shifted toward subcontractors and property developers.

Construction insolvencies rose faster than industry growth

The clearest way to understand the post-2020 increase in insolvencies is to compare company failures with the size of the industry itself. The ABS counted 462,939 actively trading construction businesses at 30 June 2025, up just 2.2% year-on-year. Over the same period, Australian Securities and Investments Commission (ASIC) first-time external administrations in construction rose far more quickly, meaning failures significantly outpaced industry growth.

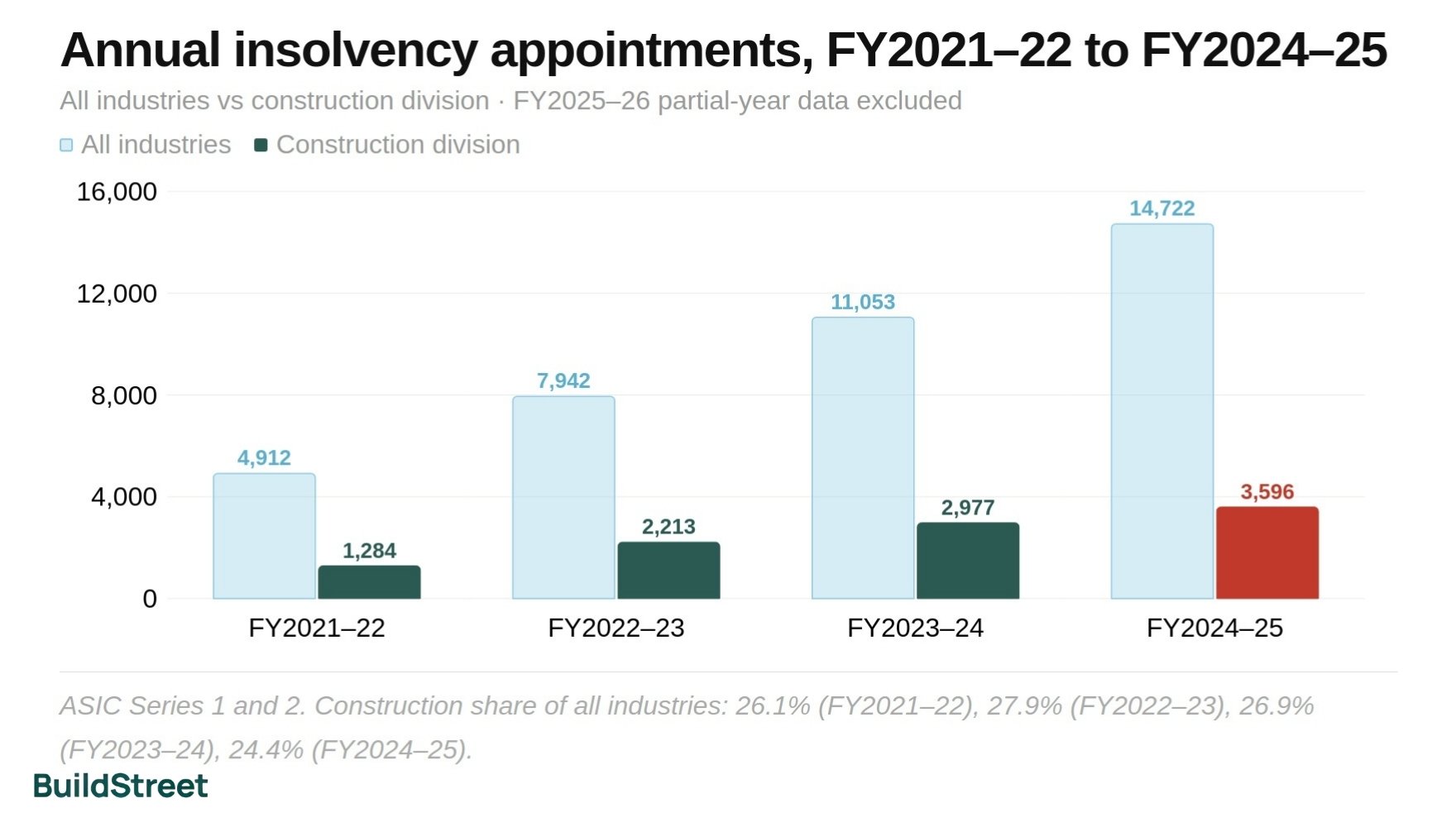

Across all industries, administrations increased from 4,912 in FY2021–22 to 14,722 in FY2024–25. ASIC reported the overall share of companies entering administration reached 0.41% in FY2024–25, up from 0.33% the year before. Construction accounted for much of that increase, representing 24% of all appointments in the first eight months of FY2025–26.

Between FY2021–22 and FY2024–25, construction services insolvencies rose 197%, residential building construction insolvencies increased 157%, and insolvencies across the full construction division rose 180%. The increase extended well beyond large builders and moved through the broader subcontracting chain.

Industry shrinkage was tiny by comparison

Increase in construction company failures between FY2021-22 and FY2024-25, from 1,284 to 3,596. Over the same period, the number of actively trading construction businesses grew by just 2.2%.

Annual insolvency appointments by sector, FY2021-22 to FY2024-25

Toggle between views. FY2025-26 partial-year data is excluded from trend comparisons.

- All industries

- Construction division

Source: ASIC Series 1 and 2. Construction share of all industries: 26.1% in FY2021-22, 27.9% in FY2022-23, 26.9% in FY2023-24, 24.4% in FY2024-25.

Annual insolvency data by sector

| Period | All industries | Construction division | Residential building | Const. services |

|---|---|---|---|---|

| FY2021-22 | 4,912 | 1,284 | 319 | 848 |

| FY2022-23 | 7,942 | 2,213 | 567 | 1,409 |

| FY2023-24 | 11,053 | 2,977 | 712 | 2,010 |

| FY2024-25 | 14,722 | 3,596 | 819 | 2,521 |

| FY2025-26 (Jul–Apr) | 11,526 | 2,824 | 593 | 1,998 |

Source: ASIC Series 1 and 2. Construction services includes subcontract trades. FY2025-26 is year-to-date to April 2026 only and should not be compared directly with full-year totals.

Monthly insolvencies in early 2026

| Month | All industries | Construction | Residential building |

|---|---|---|---|

| January 2026 | 634 | 152 | 29 |

| February 2026 | 1,260 | 307 | 55 |

| March 2026 (prov.) | 1,306 | 319 | 65 |

Source: ASIC Series 1 and 2, published 11 May 2026. March 2026 figures are provisional.

Between FY2021-22 and FY2024-25, construction services failures rose 197%, residential building construction rose 157%, and the full construction division rose 180%. The insolvency wave moved through the entire subcontracting chain, not just large builders.

Construction division

+180%

1,284 to 3,596 appointments

FY2021-22 to FY2024-25

Construction services

+197%

848 to 2,521 appointments

Subcontract trades, fastest-rising sub-sector

Residential building

+157%

319 to 819 appointments

House builders, FY2021-22 to FY2024-25

HomeBuilder and low interest rates drove a demand boom

The rise in insolvencies followed an earlier increase in residential construction demand. The federal government introduced the HomeBuilder grant during the pandemic, while interest rates were at historic lows and more households were seeking detached homes. Together, these factors helped drive a sharp increase in new house approvals, which peaked in March 2021.

That surge quickly filled builders' order books. Build queues lengthened, labour demand tightened, and builders became exposed when costs rose on projects already priced.

Demand softened through 2022 as government incentives wound down, interest rates rose, affordability weakened, and build times lengthened.

How HomeBuilder concentrated risk

The HomeBuilder grant was $25,000 for eligible new builds. Approximately 120,000 applications were received. That pipeline of funded projects entered the construction queue at roughly the same time, meaning a cost shock arriving after contract signing would affect a very large number of projects simultaneously with no ability to reprice.

The rate-hiking context

The RBA lifted the cash rate by 425 basis points between May 2022 and November 2023, from 0.10% to 4.35%. For builders and developers carrying debt during construction, this represented a sharp increase in holding costs at the same time as material costs were already elevated. Both pressures operated on the same balance sheet simultaneously.

Fixed-price contracts and how rising costs became losses

The most important structural pressure in residential construction was the use of fixed-price contracts. Builders usually agree to a price up front, and that price cannot easily be renegotiated if costs rise during construction.

In normal conditions, this is manageable. But when material costs rose sharply from early 2021, thousands of projects were already underway at earlier prices. Longer build times also increased the gap between progress payments, reducing cash flow while costs continued to build.

What did the RBA data show?

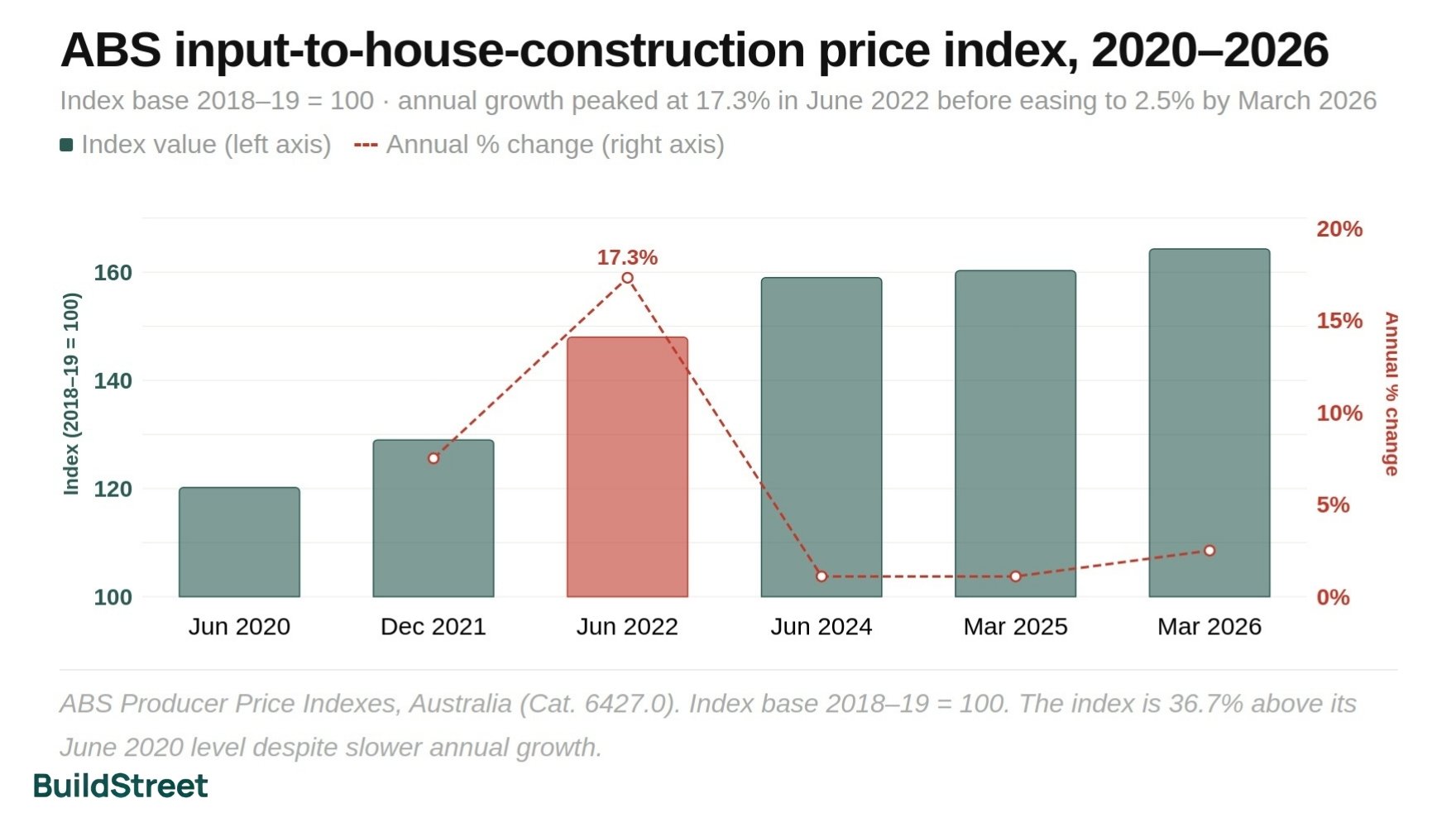

The RBA's October 2022 Financial Stability Review showed that building material costs had increased by more than 20% since the start of 2021. Detached-home build times had stretched to around 12 weeks above normal, and more than 25% of the largest 200 builders recorded an operating loss in the year to March 2022, up from just over 15% the year before.ABS input-to-house-construction price index, June 2020 to March 2026

Index base 2018-19 = 100. Annual growth peaked at 17.3% in June 2022 before easing to 2.5% by March 2026.

- Index value

- Annual % change

Source: ABS Producer Price Indexes, Australia (Cat. 6427.0). Index base 2018-19 = 100.

Key events in the cost-and-insolvency cycle

June 2020

Pandemic onset. HomeBuilder launched. Input price index at 120.2. Ultra-low interest rates and stimulus grants flood residential builders with demand just as global supply chains begin breaking down.

Late 2021

Early supply shock, running at 7 to 8% p.a. Global shipping constraints and material shortages push input costs sharply above pre-pandemic norms. Timber prices doubled within months. Steel followed.

June 2022

Annual growth peaks at 17.3% p.a. Timber and steel hit records simultaneously. Labour locked into multi-state backlogs. Builders on fixed-price contracts absorb losses with no recourse. Index reaches approximately 148.

May 2022 onwards

RBA begins rate-hiking cycle. Cash rate rises 425 basis points to 4.35%. Finance costs for builders and developers surge in parallel with materials pressure.

FY2022-23

Insolvencies reach 2,213, up 72% on the prior year. Even as the rate of cost growth decelerates, formal collapses accelerate. Businesses that became effectively insolvent in 2021-22 are now entering administration.

January 2024

ATO enforcement resumes. Debt referrals to external collectors begin. Total collectable ATO debt grew 5.2% in FY2023-24. Businesses that deferred PAYG, superannuation and GST obligations face a new and immediate catalyst for formal administration.

March 2026

Index: 164.3, up 2.5% p.a. Input growth has slowed, but the index is 36.7% above its June 2020 level. The new cost baseline is permanently higher. Early 2026 monthly insolvency figures are running below equivalent months in 2025.

Sources: ABS PPI (Cat. 6427.0); ASIC Series 1 and 2; RBA Financial Stability Review, October 2022.

How cash-flow pressure pushed builders into insolvency

Cost increases on fixed-price contracts do not usually appear as insolvencies straight away. They tend to appear first as cash-flow pressure. A builder losing money on a project still has to keep the site running, pay subcontractors, meet payroll and service debt. Losses can build while the company continues trading.

The RBA's 2022 review found that builders typically had liquidity buffers of less than three months of turnover. This was roughly 25% lower than comparably sized businesses in other industries. Around 40% of the median builder's liabilities were short-term unsecured trade credit, which was approximately double the share recorded by other businesses.

By FY2024–25, non-payment of PAYG withholding, superannuation guarantee, and GST appeared as an indicator in 83.2% of construction reports alleging insolvent trading. The share of construction insolvency reports where a company was assessed as having become insolvent more than two years before formal appointment also rose from 33.1% in FY2020–21 to 55.1% in FY2024–25.

Insolvent trading indicator

83.2%

Share of FY2024-25 construction insolvent trading reports citing non-payment of PAYG withholding, super or GST

Hidden insolvency lag

55.1%

Share of FY2024-25 reports where the company was assessed as insolvent more than two years before formal appointment

Change since FY2020-21

+22 pp

Rise in the “insolvent 2+ years before formal appointment” share, from 33.1% in FY2020-21 to 55.1% in FY2024-25

Why did insolvencies keep rising after cost pressures eased?

Many construction businesses had been under financial pressure for years before entering formal administration. In many cases, insolvency statistics lagged the actual distress by 18 months to three years, which helps explain why appointments kept rising even after material cost inflation slowed.

Nominated causes of failure in construction insolvency reports

Multiple causes can be nominated per report. This is a report-based series, not a direct count of failed companies.

- Inadequate cash flow

- Poor strategic management

- Trading losses

Source: ASIC Series 3.2 construction-industry external administrator reports.

| Financial year | Total reports | Inadequate cash flow | Poor strategic mgmt | Trading losses |

|---|---|---|---|---|

| FY2020-21 | 953 | 556 | 499 | 431 |

| FY2021-22 | 919 | 483 | 371 | 422 |

| FY2022-23 | 1,541 | 850 | 663 | 772 |

| FY2023-24 | 1,952 | 1,055 | 967 | 856 |

| FY2024-25 | 2,361 | 1,330 | 1,241 | 1,124 |

In FY2024-25, 63% of construction reports were for firms with fewer than five full-time-equivalent employees. Source: ASIC Series 3.2.

Data note: ASIC Series 3.2 is drawn from initial external administrators' reports and is a separate series from the company-count insolvency data in the tables above. Multiple causes can be nominated per report, so column totals exceed the report count.

Why construction insolvencies remained elevated after material costs peaked

Construction insolvency appointments continued rising into FY2024–25 even after material inflation slowed. By then, financial pressure had broadened beyond material costs to include labour expenses, higher interest rates, weaker trading conditions and renewed tax enforcement activity.

This shows the pressure was no longer just about material costs. By then, several other factors were weighing on the sector, including the end of pandemic support, weaker trading conditions as the economy slowed, and the ATO restarting enforcement on unpaid tax debts. The pressure was felt most strongly by construction firms and property developers. At the same time, failures among larger residential builders were starting to ease.

-

ATO enforcement resumed in January 2024. After a pandemic-era pause, the ATO began referring outstanding debts to external collectors. Total collectable ATO debt grew 5.2% in FY2023-24 and a further 2.8% in FY2024-25. For construction businesses that had deferred PAYG withholding, superannuation and GST obligations through the crisis, this represented a new and immediate catalyst for formal administration on top of existing trading difficulties.

-

Labour costs remained elevated at 4.2% p.a. Building-construction output prices were still rising at 4.2% annually to March 2026, with labour cited as a key ongoing driver by the ABS. Unlike materials, which are globally traded and subject to international price signals, wages in a domestic trade-shortage environment are stickier and less responsive to reduced activity levels.

-

Finance costs rose approximately 300 basis points. The rate-hiking cycle from May 2022 lifted borrowing costs sharply for both builders and the developers who commission their work. Development projects financially viable at 2021 borrowing rates became unviable after rates rose. Lenders requiring pre-sales on apartment projects found buyers reluctant to commit, constraining supply and concentrating risk among mid-rise developers.

Small business restructuring became a pressure release

Not every distressed construction company went straight into liquidation. From 2021, ASIC's small business restructuring process gave eligible companies a way to restructure debts while remaining under director control.

FY2021-22

70

All-industry restructuring appointments

FY2022-23

448

Up 540% on the prior year

FY2023-24

1,425

All-industry appointments

H1 FY2024-25

1,515

First half of year alone

Of the restructuring plans sent to creditors, 87% were approved. Of the plans completed by 30 June 2024, 89.4% of companies remained registered. This means the post-2020 period should be read as both an insolvency cycle and a restructuring cycle, with sector-wide balance-sheet repair taking place alongside company failures.

Construction led the restructuring queue

Construction accounted for 27% of all small business restructuring appointments between July 2022 and December 2024, the largest share of any industry. This shows the post-2020 period was not only an insolvency cycle. It was also a restructuring cycle, with many construction firms trying to repair their balance sheets and stay afloat.

Construction insolvency vs estimated restructuring appointments, FY2021-22 to FY2024-25

Construction insolvency appointments from ASIC Series 1 and 2. Restructuring estimated by applying the 27% construction share to the all-industry total per ASIC Report 810.

- Construction insolvency appointments

- Est. construction restructuring appointments

Sources: ASIC Report 810; ASIC Series 1 and 2.

Restructuring appointments vs insolvency appointments

| Financial year | Construction insolvencies | Est. construction restructuring | Ratio restructuring : insolvency |

|---|---|---|---|

| FY2021-22 | 1,284 | 19 | 1:68 |

| FY2022-23 | 2,213 | 121 | 1:18 |

| FY2023-24 | 2,977 | 385 | 1:8 |

| FY2024-25 | 3,596 | 818 | 1:4 |

Sources: ASIC Report 810; ASIC Series 1 and 2. Restructuring figures are estimates; ratio rounded.

How builder insolvency affects new home projects

With 3,596 construction companies entering external administration in FY2024–25, and insolvency rates well above pre-pandemic levels, the risk of a builder failing mid-project has increased compared with five years ago.

Builder financial health

A builder's quote, plans and display homes show the type of work they offer. Their financial position is also relevant because it may affect whether the project can be completed as agreed. With construction insolvencies still well above 2021 levels, checks of the relevant state licensing register and recent trade references are commonly used to assess builder risk before contract signing.

Fixed-price contract risks

A fixed-price contract may limit some cost increases, but the final price can still change. Many contracts include variation clauses, prime-cost items and provisional sums. These can increase the amount paid if selections, site conditions or allowances change.

Deposit and payment protections

Most states limit upfront deposits and require protections for certain residential building contracts. Domestic building insurance can provide a backstop if a builder fails before completion, although eligibility rules, claim timeframes and coverage limits vary by state.

Builder workload and pipeline length

Builders under pressure were often managing large volumes of committed work in a difficult cost environment. Long queues and extended build times can increase project delivery risk, particularly where builders are carrying multiple projects at once.

About the data

The ASIC broad construction division includes builders, subcontractors and other construction firms. This article separately compiles the residential building construction group from ASIC's detailed Series 1 dataset, but cause-of-failure tables are only available at the broader construction industry level.

ASIC Series 3.2 is based on initial external administrators' and receivers' reports, not the company-count insolvency series. Multiple causes can be nominated in each report. Those tables are best read as evidence on the character of failures, not as a count of failed companies.

The cleanest builder-specific company-count series in the current ASIC detailed workbook runs from FY2021-22 onward. Rebuilding a fully consistent long-run residential-builder series would require additional extraction from older ASIC files.

General information only

This article is based on publicly available ASIC, ABS and RBA data. It is general information only and does not constitute financial or investment advice.

ASIC insolvency statistics, Series 1, 2 and 3.2

RBA Financial Stability Review, October 2022, Box C: Financial stress in residential construction

RBA Financial Stability Review, September 2024, Resilience of Australian Households and Businesses

ABS Producer Price Indexes, Australia (Cat. 6427.0), March quarter 2026

ASIC Report 810, Small Business Restructuring Review, June 2025

ABS Counts of Australian Businesses, Including Entries and Exits, June 2025

ABS Insights: Output of building construction prices

Chart Snapshots